Clarus Top Blogs of 2019

For my last blog of the year, I will highlight our top blogs of the year. Top New Blogs in 2019 Starting with a ranking of the most popular new blogs that we published in 2019. Mechanics and Definitions of Carry in Swap markets €STR – What you need to know Ameribor – The $1.5bn […]

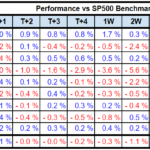

How do CNBC Stock Pickers Perform?

As year end is upon us, we sometimes like to perform some more lighthearted analysis. Many of you will know that the US financial markets are covered well by cable news network CNBC; and I’ve become a fan of the lunchtime “Halftime Report”. At the end of each episode, they typically solicit a handful of […]

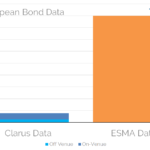

MIFID II Data for Bonds

Let’s take a look at the European bond market today. I wanted to repeat much of the analysis that I performed for MIFID II post-trade data concerning Interest Rate Swaps. However, I realised that we do not have enough of a complete data set due to a myriad of data access issues. For example, the […]

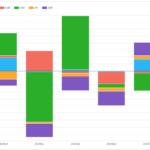

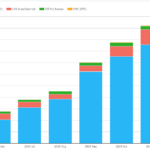

Futures and Swaps Volumes and OI in 2019

As we get close to year end, it is time to assess the trends in volumes that we have seen in 2019. Usually we do this by looking at the cleared volume in a period (month/quarter) compared to an earlier period, or the open interest (outstanding notional) at a point in time. Today I will […]

Four Trends in Swaps Data 2019

Welcome to a review of Clarus data for 2019. Cleared Rates markets are a $2.7trn-per-day market in 2019. On top of this, Compression accounts for a further $2trn of activity every day. Continued growth in clearing, electronification and compression coupled with a shortening of maturities have been identified by the BIS as key drivers for […]

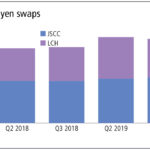

Swaps Data: Q3 2019 Clearing Volumes increase

My monthly Swaps Review looks at Q3 2019 volumes compared to 2018 and CCP market share for: Interest Rate Swaps in USD, EUR, JPY Credit Default Swaps Non-Deliverable Forwards FX Options Please click here for free access to the full article on Risk.net.

SOFR Futures and Swaps – November 2019

Last week we covered SOFR Market Developments covering the comparison of SOFR derivatives volumes vs Libor and FedFunds, which highlighted the massive growth that needs to happen for SOFR to surpass Libor as the primary interest rate reference index. Every firm active in Futures and Swaps should be tracking the uptake of SOFR trading and […]

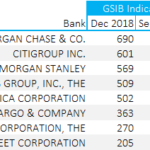

G-SIB Scores for US Banks

We detail the GSIB methodology for US banks, referred to as “Method 2” in the literature. We calculate the GSIB scores for 8 US banks as at December 2018 and September 2019. We find that the Method 2 scores are particularly penal for Morgan Stanley. It will be interesting to see how these scores change […]