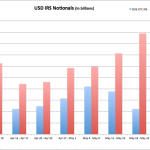

CME and LCH June 2015 Volumes

Following on from my blog LCH makes gains vs CME in USD IRS, I wanted to provide an update for June. Weekly Volumes Using CCPView lets look at weekly volumes of gross notional for just USD IRS for the past 8 weeks and compare CME IRS Volumes with LCH SwapClear Volumes (All and not just Client). Showing that: Jun […]

CCP Default Management Process and the SwapClear Fire Drill

There has been a lot written in the press about the increased importance of Central Counterparties (CCPs) and the cash and capital resources available in the event of member defaults. A CCPs Default Management Process (DMP) documents the steps to be taken in the event of a member default. These are designed to utilise the defaulting members margin to […]

Liquidity

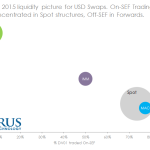

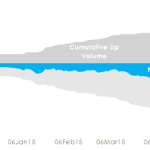

Clarus tools help our users monitor liquidity risk across Swaps markets. In this blog, we quantify how much risk has traded this year across a broad range of swap subtypes, and across venues. We show how our clients can use SDRView to stay on top of the risks they are running. Liquidity Concerns According to […]

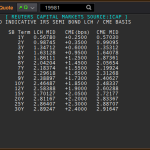

Pricing and Arbitraging the CME/LCH Basis

I’ve been pondering the appropriate spread between LCH and CME. It would seem to me that every firm should have their own true cost of putting on a swap at CME or LCH, based upon a multitude of factors not limited to how they are currently positioned. I thought it worthy to explore what these […]

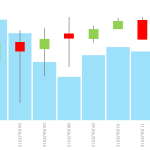

Technical Analysis in Swaps

Following on from last week’s look at the volatility in EUR swaps markets, I wanted to switch my attention to see the knock-on effect in USD swap markets. So let’s look at some of the Technical Analysis that is possible via our suite of SDRView tools. Is That an Outright or a Spread Sir? One […]

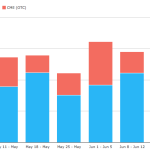

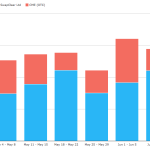

LCH Makes Gains vs CME in USD IRS (8-12 Jun 2015)

Following my blog on CME and LCH: What Happened on May 19 and Jun 12, I wanted to re-visit the data now that we have another week of published volumes. Weekly Volumes Using CCPView lets look at weekly volumes of gross notional for just USD IRS for the past 6 weeks and compare CME IRS Volumes with LCH […]

A New Flavor of Invoice Spreads?

If you’ve been following the package trade exemption, you’d know that Invoice spreads are one of the last package trades yet to be traded on-SEF. The swaps are due to be SEF-required (MAT’d) in November of this year. I wrote a blog last year about the issue here. While I am no further educated on just […]

CME and LCH: What Happened on May 19 and Jun 2?

Continuing with the theme of CME-LCH Basis which has been a phenomenally popular blog, I wanted to look at whether there has been an impact on volumes of Cleared USD Interest Rate Swaps at CME and LCH. Weekly Volumes Using CCPView we can extract weekly volumes of gross notional for just USD IRS for the […]

Volatility and Volumes in Europe

Since European Rates made all-time lows on 17th April, we have seen an unprecedented sell-off in European fixed income. SDRFix shows the moves from 17th April to the close on 5th June 2015: Showing: A huge steepening on the yield curve, with 30y rates 90bp higher (!), versus 2y higher by only 7.2bp. 5y are […]

The Issue with Anonymous Order Books in Swaps

The conversation seems to be heating up again about the topic of anonymous order books for the OTC swap market. The topic has been out there for well over a year, however really had not been in the press or acknowledged by the CFTC until SEFCON V in November 2014. It remains un-addressed. The CFTC […]