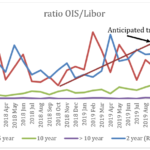

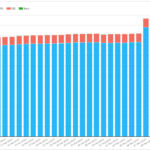

SOFR Market Developments

Last month I wrote about SONIA market developments and how trading is progressing ahead of 2022 when Libor is expected to end. In this blog I extend this analysis to the USD markets. Much like SONIA, SOFR has seen some growth over the past year, which is to be expected as USD Libor is also […]

G-SIB Mechanics and Definitions

There are 30 Global Systemically Important Banks (G-SIBs) in 2019. A bank must hold at least an extra 1% in Tier One capital as a result of qualifying as a G-SIB. We look at the calculations necessary to work out a bank’s G-SIB score and calculate the exact values for 2019. We estimate that HSBC […]

Mechanics and Definitions of ISDA IBOR fallbacks

If an ‘IBOR rate, e.g. USD LIBOR, ceases to publish, we now know the exact methodology that will be used in derivatives contracts to calculate a replacement rate. The calculation uses compounded in-arrears Risk Free Rates, which are decided at a currency level. A spread will be added to these compounded rates, which will be […]

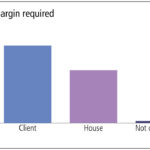

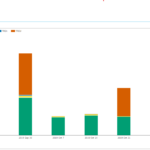

Swaps Data: Clearing Houses and one trillion dollars

My monthly Swaps Review looks at aggregate disclosures from over 50 clearing services, with details on: Initial margin by house and client Initial margin by product type Default resources, member and own capital Cash resources Stress Loss Margin calls Showing that in aggregate over $1 trillion is held by or available to clearing houses. Please click […]

Eurex Swaps and the DekaBank transfer

Last week Eurex put out a press release, DekaBank successfully switches swaps book to Eurex Clearing which was interesting enough to make me want to find out what else I could learn about the switch. The public details are that over 7,000 individual transactions were switched from LCH SwapClear to Eurex Clearing in a single […]

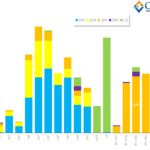

SONIA Term Rates – which is best?

Four providers have entered the race to provide term SONIA fixings. These terms fixings are intended to ease the uptake of SONIA and made the transition easier for end-user cash markets. The providers are LSEG, ICE, Refinitiv and Markit. We look at their proposals. Looking at the SDR data we find that 80% of SONIA […]

What we need to do to fix MIFID II Data

We attempt an analysis of available MIFID II transparency data. Analysis shows that 89% of notional in vanilla EUR IRS is reported with a four-week delay. We show that at least €800bn of transaction data for vanilla, cleared EUR IRS is missing each week. We estimate that as little as 5% of notional of off-venue […]

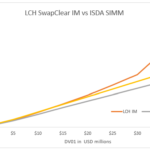

ISDA SIMM Concentration Thresholds for IR Risk

We last looked at ISDA SIMM Concentration Thresholds in January 2017, when ISDA SIMM version 1.2 introduced the concept. That blog detailed an Excel implementation of the concentration threshold calculation for interest rate delta risk and proved very popular. The methodology in SIMM v2.2 remains the same, just the thresholds themselves are changed. Today I […]