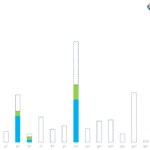

MIFID II Transparency will leave us in the dark

We run the SSTI and LIS thresholds over US SDR data. We anticipate that over 80% of EUR swaps will not be subject to pre-trade transparency. Post-trade transparency will not be much better. 75% of the risk traded will remain dark for up to four weeks. We are intrigued to see what the APAs will […]

FRTB Non-Modellable Risk Factor Analysis

The FRTB Internal Model Approach requires risk factors to be checked for modellability Non-modellable risk factors are then subject to stressed capital add-ons Modellable and non-modellable is determined by applying a specific test Clarus has the Data and Analytics to perform such a test We make this available in our FRTB for Excel product Making […]

APRA – Margining for non-centrally cleared derivatives

It is almost two years since I wrote about the Final US Rules on Margin for Non-Cleared Swaps. How time flies and since then we have seen implementation of this rule in the US and equivalent rules and regulations in many other jurisdictions. Today I will look at the Australian regulation recently made final by […]

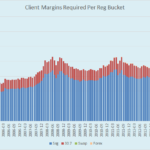

FCM Rankings & Concentration: Q2 2017

We have Q2 data for Clearing Brokers, showing any changes in the US clearing landscape. Let’s dig into the data, starting with our count of FCMs by various metrics: Showing 63 firms registered (down 1 from Q1 2017), and 56 firms with any Client Requirements. Other headline metric is total client required margins, which trended […]

Curve Trading in USD Swaps

Curve trades account for around 10% of volumes reported to US SDRs. We identify these package trades by matching timestamps and risk equivalence of the two legs. Benchmark curve switches trade every single day in decent size. We look at the USD Curve Trade market during 2017. Curve Trading Call them Curve Trades, Spreads or […]

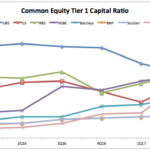

Capital and RWA for European Banks

Following on from my recent Capital Ratios and Risk Weighted Assets for Tier 1 US Banks article I wanted to look at the equivalent metrics from European Banks. Background One of the lessons learned from the Great Financial Crisis was that Banks were generally under capitalised commensurate to their risk exposure, leading to new Basel III regulations […]

MAC Swap Trading

Tod last took a look at MAC swaps in 2016. Has anything changed since? (Spoiler: not much!). But there is certainly some activity over at ERIS. What are MAC Swaps? A brief reminder that a MAC swap is a particular flavour of forward starting interest rate swap, starting on an IMM date (third Wednesday of […]

Our Response to the ESMA Trading Obligation Consultation

ESMA published their latest Consultation on Trading Obligation for Derivatives under MIFIR on 19th June 2017. As we stated back in June, we have concerns about the quality of the data used to determine the Trading Obligation. We have therefore offered to make all of our SDR data available to ESMA as part of our response to the […]

Array Formulas in Excel

We explain how to work with Array Formulas in Excel. Master the Three Finger Salute CTRL+SHIFT+ENTER. CTRL+/ is an amazingly effective shortcut. It is always easier to expand an array than shrink it. Consistent formatting provides an obvious visual cue when working with arrays. SIMM for Excel SIMM for Excel is an add-in that performs […]

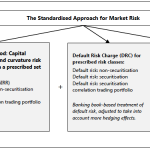

FRTB – Simplified Standardised Approach

The BCBS recently published a Consultative document on a ‘Simplified alternative to the standardised approach to market risk capital requirements” and in this article I will look at the detail of this. Standardised Approach (SA) BIS provides the following diagram to summarise the Standardised Approach. (For a re-cap of the SA see FRTB – What […]