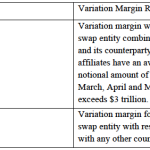

Final US Rules on Margin for Non-Cleared Swaps

On October 22, the United States published its Final Rules to establish the minimum margin requirements for swaps transacted by insured depository institutions, which are not cleared by a clearing house. The Joint Rules are the work of the Federal Deposit Insurance Corporation (FDIC), the Office of the Comptroller of the Currency (OCC), the Federal […]

What I Learned at SEFCON VI

The 6th annual SEF event took place on Monday. Always a good day to meet folks and hear what’s happening in SEF-land. As usual I’ll summarize the event for those who could not attend. For starters, ICAP pulled out of the WMBA so was generally not present. I noted only one ICAP representative in the […]

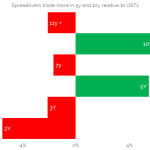

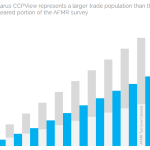

US Treasuries and Spreadovers – Market Comparisons

We compare Average Daily Volumes in US Treasury bonds to those in Spreadovers reported to the SDR Spreadovers account for about 2.5% of turnover of US Treasuries The maturity profiles of trading are broadly similar But Spreadovers have a greater concentration of trading in the 5y and 10y maturities. Half of all trades are not […]

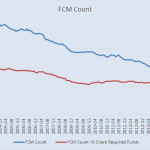

Update on The Health of FCMs

Six months ago I wrote a report that looked at the health of the FCM community. My general findings were that: The number of FCM’s was actively shrinking Only a small portion of FCM’s were handling Cleared Swaps The amount of client funds to support cleared swaps has doubled in the last year, concentrated largely […]

MiFID II and Best Execution for Derivatives

Following on from my recent article on MiFID II and the Trading Obligation for Derivatives, I wanted to look into another key section in the ESMA Final Report; namely the requirements for Best Execution. There are two specific requirements, one for Trading venues and another for Investment Firms. MiFID II Background The Final Report deals with Draft Regulatory […]

Our new Belfast office

We recently announced our expansion with a new office in Belfast. Key reasons for the choice of Belfast are; Well educated, English speaking STEM graduates, A very positive business environment, An existing financial technology cluster. Universities Belfast has two universities, Queens University of Belfast, dating back to the mid 1800s, and Ulster University a modern […]

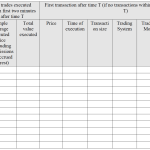

Why trade level reporting is the only reporting that makes sense

We look at the data sources available for AUD IRS markets…. …and try to reconcile some of the numbers We quickly find this is not as easy as it first appears…. …and conclude that publicly disseminated, trade-level reporting is the only way to add true transparency to OTC derivative markets. The great data reconciliation game […]

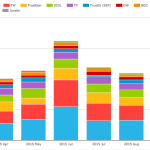

September 2015 Review – More of the Same

Continuing with our monthly review series, let’s take a look at US Interest Rate Swap volumes in Sep 2015. First the highlights: On SEF USD IRS Sep 2015 volume was >$1.2 trillion, Up from August and similar to July SEF Market Share remains the same as YTD Bloomberg in front with 30%, Tradeweb 23%, IDBs in mid-teens […]

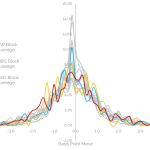

Performance of Block Trades on RFQ Platforms

The nature of swaps trading (RFQ to 1 participant for example) means that there can be a motivation to trade large-sized tickets in an old-school fashion – bilaterally. Therefore, unlike more mature electronic markets, these orders are not sliced’n’diced. This means that not only the performance of these large trades can be monitored in public data…. […]

Identifying Customer Block Trades in the SDR Data

Following up on our previous blog, What’s the story behind Tradeweb block trading? Regulations mean that different market participants will transact trades of block size in different ways This allows us to identify whether a block trade is transacted across a D2D venue, Tradeweb or Bloomberg We therefore have increased transparency as to whether these […]