BREXIT: Moving Euro clearing conflicts with G20 Market Reforms

Moving clearing of EUR-denominated contracts to the Eurozone is a complicated proposition. Bifurcating cleared portfolios will make bilateral markets more attractive than cleared markets. This raises questions over existing clearing mandates. It also conflicts with the G20 OTC market reforms intended to reduce systemic risk through the promotion of clearing. Enforcing a location policy for a […]

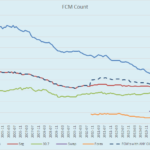

FCM Rankings & Concentration: Q1 2017

Clearing broker data is out for Q1 2017, so I wanted to run the numbers and see if anything has changed. Lets start with a view onto the number of registered FCMs. This shows 64 firms registered (down 1 from Q4 2016), and 55 firms with any Client Requirements (down 2). On the bright side, there […]

Swaps Data Review: ADV for OTC Derivatives

My Monthly Swaps Data Review for Risk Magazine was published today. This shows that Average Daily Volume (ADV), a widely used metric for Futures and Options contracts, can now be calculated at a the same granular level for OTC Derivatives. So just as CME Group publishes the ADV for the 10Y Treasury Note, it is […]

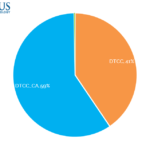

CAD Swaps – What Does the Data Show?

Amir took a look at CAD swaps when we first added the new Canadian DTCC data source at the beginning of this year. Now that we have more data and reporting has bedded down a bit, I thought it worthwhile to analyse the data to see if two sources are better than one. Canadian reporting […]

Microservices for Derivatives: What You Need to Know

It has been some months since I wrote about Microservices and the Amazon Cloud and as we have recently released a major new version, I wanted to elaborate further on the importance of this technology. Background Microservices are fine-grained services that can be used to rapidly assemble a more complex service, a system, or a user interface. Unlike libraries […]

マイクロ・サービス: ISDA SIMM センシティビティ・カリキュレーター

ClarusのAPIにはSIMMのセンシティビティを計算する関数があり、FpMLやCSVトレード・リスト・ファイルを含む多くのフォーマットが利用可能だ。

計算結果はISDA SIMM CRIFファイル・フォーマットに出力される

関数は一般的な言語、すなわちPython、R、C++、Julia、Java等の言語で実行可能だ

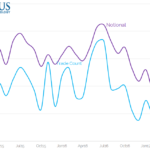

SONIA Reform – What is Going On?

There are two parallel branches to the SONIA reforms. One is to modify how the rate itself is being set. The other is to promote its’ use as the near Risk Free Rate for GBP derivative markets. We take a look at current SONIA markets. *Updated 18th May 2017 to correct the use of trimmed-mean (not median) […]

April 2017 Swaps Review

Continuing with our monthly Swaps review series, let’s look at volumes in April 2017. Summary: SDR USD IRS price-forming volume > $1.8 trillion gross notional SEF Compression activity in USD IRS > $250 billion USD OIS volume was > $2 trillion Both USD IRS and OIS are well down from recent highs EUR IRS and OIS volume is mostly Off SEF SEF USD, […]

CCP Disclosures 4Q 2016 – Trends in the Data

Central Counterparties recently published their latest CPMI-IOSCO Quantitative Disclosures and in this article I will highlight a few of the key trends, similar to my article on 3Q 2016 trends. Background Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk […]

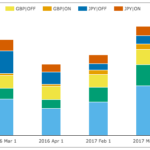

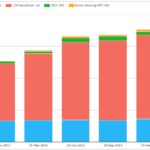

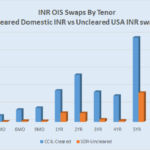

KRW and INR Swap Clearing

The CME have announced they are planning to clear Korean Won (KRW) and Indian Rupee (INR) interest rate swaps in the near future. I wanted to have a look at what these markets look like. So first things first, I grabbed all trades for non-G4 swaps on the US SDRs, year-to-date. Did this for both […]