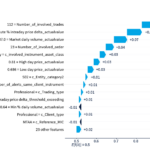

Improving transparency in ML models for market abuse detection

We recently covered an article on Using AI for Market Abuse Surveillance, a very interesting use of Machine Learning (ML) to improve the classification of alarms generated in market surveliance. One of the issues with ML is the lack of transparency, due to the “black-box” nature of the models. So you get an answer, but […]

Fast Valuation of Seasoned OIS Swaps

OIS swaps have coupons determined by compounded daily interest rates settled every few months. The valuation of future coupons is computationally similar to the valuation of a LIBOR payment, in that the valuation involves the ratio of two discount factors associated with the start and end of the accrual period. A problem can arise on […]

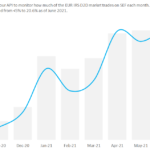

Using the Clarus API to monitor the latest Brexit impacts

After shouting “HopSchwiiz” in my adopted nation waaaaaay too much at the football last night, I needed a somewhat low-energy blog this morning. Step forward our easy-to-use API, which has recently been extended to include data from both CCPView and SEFView. Hopefully it’s not such a rollercoaster ride using the Clarus API 😛 Brexit Moves […]

Cloud Security – What you need to consider

In this article we look at cloud security. With all the hype around Cloud, it’s easy to make assumptions as to what it can do, but security is an area where making assumptions can prove very costly, both financially and reputationally. This blog will look at the cloud security model, security features offered by cloud […]

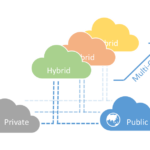

Types of Cloud – A Primer on the Choices and Challenges

Cloud is now ubiquitous, but not all clouds are the same. In this blog we will look at the different types of cloud – Private, Public, Hybrid and Multi-Cloud, and think about their suitability and use in financial organisations. Private Cloud Private clouds are facilities created for a single organisation: they may be provided as […]

Migrating to Cloud – An Insider’s Guide

In earlier blogs we have discovered the agility inherent in Cloud, but how do organisations manage to tap into this, with all their legacy systems? In this blog we will cover the strategy and issues involved in migrating a large systems estate. We will start by assuming foundational Cloud concerns for financial organisations such as […]

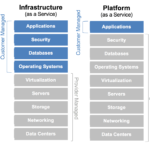

PaaS and SaaS – What you need to know

In my last blog I described the origins of Cloud and highlighted some of the benefits of Infrastructure as a Service (IaaS), but this does not reflect the real value of Cloud. To uncover this, we will explore the concepts of Platform as a Service (PaaS) and Software as a Service (SaaS). Platform as a […]

Infrastructure as a Service – the Bedrock of Cloud

In this blog I will explain the origins and key features of Infrastructure as a Service (IaaS), the core foundations of what we think of as Cloud. Cloud computing is an evolutionary consequence of a sequence of technology innovations, stretching from human based computing, across generations of hardware and networking, to the advent of virtualisation […]

Indices are the best way to calculate compound interest

To avoid complications with compound interest calculations, administrators of RFRs could publish a single Index each day. The equivalent term rate for any period could then be calculated by looking up the index level from the start date and the end date of each period. Interim rates do not need to be known. This allows […]

Test Data for the Cumulative Trivariate Normal Distribution

Using Java I implemented the double precision algorithm to compute the cumulative trivariate normal distribution found in A.Genz, Numerical computation of rectangular bivariate and trivariate normal and t probabilities”, Statistics and Computing, 14, (3), 2004. The cumulative trivariate normal is needed to price window barrier options, see G.F. Armstrong, Valuation formulae for window barrier options”, […]