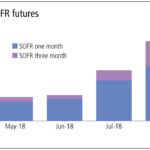

Swaps Data: The race to replace Libor

My monthly Swaps Review in Risk Magazine discusses Libor and looks at derivatives volumes in the Alternative Reference Rates that have been selected to replace it. I look in detail at SOFR Futures, SONIA and EONIA Swaps. Please click here for free access to the full article on Risk.net.

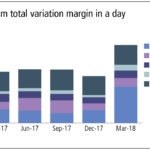

Swaps Data: OTC Margin Up, Futures Margin Down

My monthly Swaps Review in Risk Magazine looks at the most recent CPMI-IOSCO Quantitative Disclosures by Clearing Houses for Interest Rate Swaps, Credit Default Swaps and Futures and Options Showing strong year-on-year growth in each of these, except the last. I also look at the trend in client IM at LCH SwapClear and the maximum Variation margin call […]

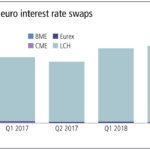

Swaps Data: The Big Get Bigger in Cleared Swaps

My monthly Swaps Review in Risk Magazine looks at global cleared volumes by CCP in 1H 2018 compared to 1H 2017 for: USD IR Swaps, EUR IR Swaps, JPY IR Swaps CDS Index and Single-name, USD and EUR Non-Deliverable Forwards Showing strong growth in all of these, except one. Please click here for free access […]

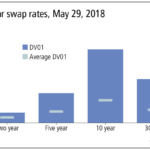

Swaps Data: Anatomy of a Wild Week in USD Swaps

My monthly Swaps Review in Risk Magazine looks at the recent market volatility resulting from Italian political events, which caused investors to move out of euros and into dollars and treasuries: 29th May, saw large falls in USD Swap Rates Swap volumes three times higher in major tenors How prices moved during the day Recovery […]

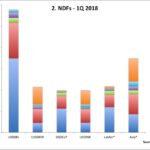

Swaps Data: The Allure of Liquidity

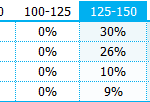

My monthly Swaps Review in Risk Magazine looks at execution venue market share in 1Q 2018 for: CDS Index NDFs by currency pair FX Options by currency pair Interest Rate Swaps by major currencies Bloomberg MTF for EUR IRS In simple terms, it shows that volume is either dominated by a single venue or split […]

Mar 2018 Swaps Review – SDR Data in 9 Charts

Continuing with our Swaps review series, let’s look at volumes in March 2018, focusing just on SDR Data. Summary: USD IRS volumes in 1Q 2018 are 11% higher than 1Q 2017 USD IRS On SEF Compression, a record month in Feb 2018 USD Swap Curve flattened by 12 bps over the month USD OIS volume exceeded the gross notional of USD IRS EUR, GBP, […]

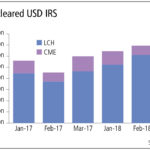

Swaps Data: A MiFID-shaped hole

My monthly Swaps Review in Risk Magazine looks at: Global volume in Cleared USD Swaps at LCH and CME US Swap Execution Facility volumes US Off SEF volumes MiFiD II so far failing to provide meaningful data USD OIS Swap volumes The challenge for SOFR Please click here for free access to the full article […]

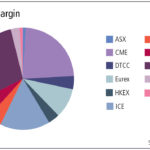

Swaps Data: Clearing’s $750 billion funding requirement

My monthly Swaps Review in Risk Magazine looks at the most recent CPMI-IOSCO CCP Quantitative Disclosures for the majority of CCPs to show that: Initial Margin required is > $500 billion The breakdown by CCP of this figure How IM is held, Gov Bonds, Cash, Other Variation Margin, daily average > $10 billion Default Resources […]

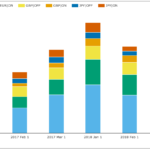

Swaps Data: the monopoly effect in clearing

My Monthly Swaps Data Review for Risk Magazine was published this week. This looks at 2017 CCP Volumes for: Interest Rate Swaps, in major and minor currencies Credit Derivatives, index and single-name Non-Deliverable Forwards It shows the dominance of one global CCP in each asset class and significant share by other CCPs in a specific […]

Clarus Daily Briefing

Our Clarus Daily Briefing is *FREE*. It provides a summary of price moves, volume trends and central bank expectations. Bringing you information about Swap markets straight to your inbox. Is your firm interested in sponsoring the Daily Briefing? If so, reach out to us. The FREE Clarus Daily Briefing Every morning, Clarus deliver our Daily […]