On June 30, Oracle issued $10 billion in bonds; the second largest corporate bond offering of 2014 after Apple’s $12 billion in April.

In this article I will look for Interest Rate Swap trades associated with this bond issue.

Bonds Issued

Lets start with the bonds themselves, which were issued in 7 tranches. (See Financial Review article).

- 3Y – $1 billion – Floating Libor 3M + 20bps

- 5.25Y – $750 million – Floating Libor 3M + 51 bps

- 5.25Y – $2.0billion – Fixed 2.3% (T+65)

- 7Y – $1.5 billion – Fixed 2.8% (T+70)

- 10Y – $2.0 billion – Fixed 3.4% (T+90)

- 20Y – $1.75 billion – Fixed 4.3% (T+95)

- 30Y – $1.0 billion – Fixed 4.5% (T+115)

Looking for the Swaps.

As Bond Issuers commonly execute interest rate swaps to change the fixed coupon into floating, we should first look for these trades. And as Oracle is a corporate hedging its bond, these swaps will be exempt from clearing and executed off SEF. They will also be large block trades.

Secondly we should look for the asset swaps done by the bond investors with the dealer, which allow the dealer to hedge its exposure to the issuer swap. These swaps will be cleared and probably off SEF as non-MAT dates.

Thirdly we should look for dealer hedges in the D2D market.

We would expect the first two of these swaps to have a maturity date that matches one of the bonds. As well as a fixed rate that matches the coupon of the bond, with a floating leg with a libor-spread to bring the value of the swap back to par. So we should be able to find these form all the swaps traded.

However the third type, the dealer hedges are likely to be standard MAT trades and so not distinguishable from others done at the same time.

Ignoring the first two floating bonds, lets start with number 3 in the above list i.e. 5.25Y at 2.3%.

5.25 Y or 2019 Bond

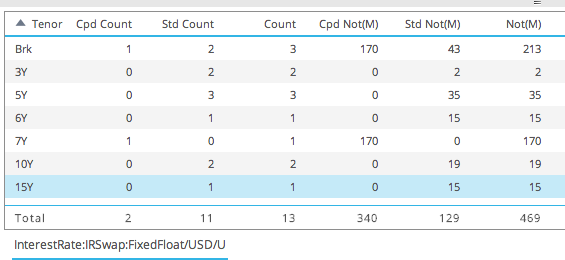

Using SDRView Professional we can select 30 June, USD IRS, Uncleared, the SubType “NStd” for non-standard (non-par swaps) and turn on the view option, “Separate Capped”.

Which shows that:

- There are two capped trades

- One in the Brk (broken) tenor row, where we would expect to find our 5Y3M trade

- One in the 7Y tenor row.

Lets drill-down on the single capped trade in the Brk column, which leads us to the following trade:

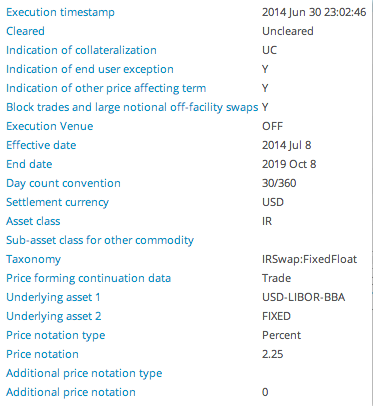

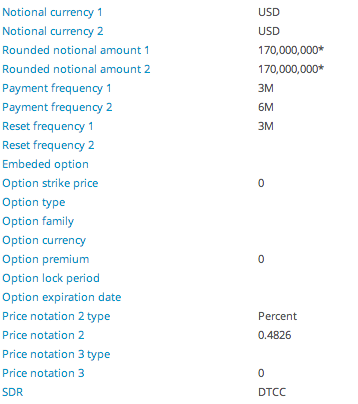

From which we can see that:

- Execution time as 23:02 LON or 6:02 NYC

- Execution Venue is Off

- End date is 2019 Oct 8, so exactly 5Y3M

- Fixed rate is 2.25% (not 2.3%, did BBG article get this correct as at 65bps over treasuries)

- Notional is rounded an capped at $170 million, the maximum shown for this tenor

- Price notation 2 shows a spread of 48.36 basis points on the Libor leg

- (Note 5Y Par rate on 30 Jun was 1.70)

So we can be pretty confident that this is the Swap executed by Oracle to swap its 5.25Y Bond coupon payments into floating.

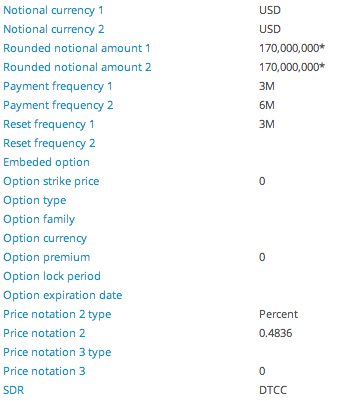

And what of the asset swaps with the bond investor?

Switching from Uncleared to Cleared, allows us to find this.

Which shows:

- Execution time as 22:14 LON or 5:14 NYC

- So 48 minutes prior to the client trade?

- Can we really trust execution timestamp for Off SEF trades?

- Probably not.

- Execution Venue is Off

- End date is 2019 Oct 8, so exactly 5Y3M

- Fixed rate is 2.25%

- Notional is rounded an capped at $170 million, the maximum shown for this tenor

- Price notation 2 shows a spread of 48.26 basis points on the Libor leg

So there you have it.

We have found the client trade and the investor trade..

We do not know how much of the $2 billion was swapped, presumably the full amount, perhaps less.

We do know that the client traded at 48.36 bps vs 48.26 bps for the investor.

So theoretically the dealer made 0.1 bps on the trade.

However given the difference between cleared and bi-lateral trades (credit charge), this looks a very tight price.

7Y Bond

Repeating the same for the 7Y Bond with fixed rate of 2.8%, we find the client trade with details:

- Execution time as 22:30 LON or 5:30 NYC

- Execution Venue is Off

- End date is 2021 Jul 8, so exactly 7Y

- Fixed rate is 2.8%

- Notional is rounded an capped at $170 million

- Price notation 2 shows a spread of 63.4 basis points on the Libor leg

However this time we find two cleared trades.

- Execution times of 22:40 LON and 0:02 LON

- Price notation 2 shows a spread of 62.95 basis points on the Libor leg

Presumably this is because the investor asset swaps were done in two separate trades.

In this case the dealer made 0.45 bps on the trade.

Which is a lot more than then 0.1 bps on the on the 5Y.

And perhaps a truer reflection of the price difference between cleared and bi-lateral trades.

10Y / 20Y / 30Y

Now you probably think you know what is coming; the same for 10Y, 20Y & 30Y.

If only life was that simple.

Unfortunately I cannot seem to find swaps with the same maturities and coupons as these bonds.

Which would lead me to believe that perhaps these were not swapped; as the issuer chose to remain paying fixed for the longer maturities, which would be entirely plausible.

Or they were or will be swapped after June 30. (Not found them on any of the subsequent days yet).

Or if they were swapped, a different swap strategy was used.

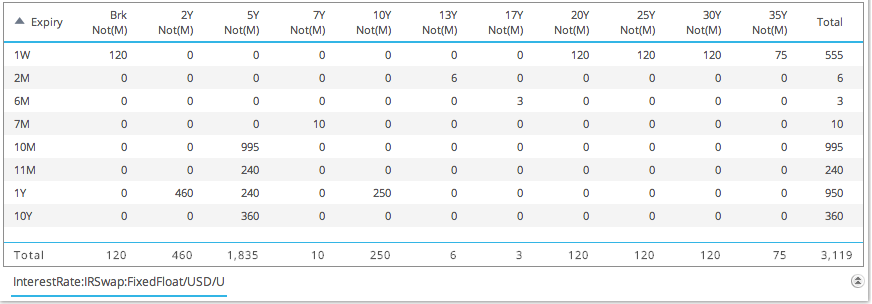

The only thing I can find that is plausible are some uncleared, forwards 1W into 20Y, 25Y, 30Y, 35Y, all block, which look unusual.

So definitely worth looking into.

But I am out of time for this blog.

D2D Hedges

We could look for cleared trades done around the same time.

However again I am out of time to look for these, so will leave that to those of you that are interested.

Summary

Oracle issued $10 billion of bonds on June 30, 2014.

These were in seven tranches.

For two of these (5Y3M and 7Y) we can find the associated client swaps in SDRView.

We can also find the asset swaps done with bond investors.

The price difference between the two is 0.1 bps and 0.45 bps.

Reflecting the difference in cleared vs bi-lateral pricing and profit

The 10Y, 20Y & 30Y do not appear to have been swapped.

Unless the forwards (in prior section) are the trades.

There is a lot that can be discovered in the data.