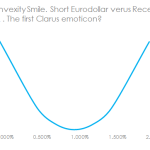

CME-LCH Basis: Convexity in Eurodollar Futures

Tod wrote about monetizing the CME-LCH basis last week by means of a straight 5 year swap. But is there a simpler way to go about it? We explain convexity trades, look at different pay-offs when funding costs are applied and then find evidence in the SDR data of convexity plays being put on with CME cleared […]