December 2016 Swaps Review

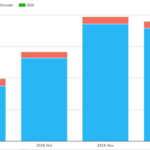

Continuing with our monthly Swaps review series, let’s look at volumes in December 2016. Summary: SDR On SEF USD IRS price-forming volume >$1.3 trillion gross notional 13% higher than a year earlier SEF Compression activity was >$350 billion in USD IRS The highest month on record and 66% higher than a year earlier USD OIS surprisingly has Off SEF volume up and On […]

Spreadovers

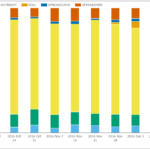

Clarus data now includes the implied Spread to the nearest on the run US Treasury bond for spot starting USD interest rate swaps. These so-called Spreadover trades make up over 10% of the USD derivatives market. Analysing price action and volume trends in these packages highlights important market insights, which can be explained by seasonal trends in bond […]