MIFID II Transparency will leave us in the dark

We run the SSTI and LIS thresholds over US SDR data. We anticipate that over 80% of EUR swaps will not be subject to pre-trade transparency. Post-trade transparency will not be much better. 75% of the risk traded will remain dark for up to four weeks. We are intrigued to see what the APAs will […]

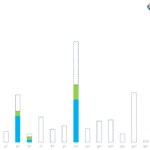

FRTB Non-Modellable Risk Factor Analysis

The FRTB Internal Model Approach requires risk factors to be checked for modellability Non-modellable risk factors are then subject to stressed capital add-ons Modellable and non-modellable is determined by applying a specific test Clarus has the Data and Analytics to perform such a test We make this available in our FRTB for Excel product Making […]