LIBOR OIS – March 2018 Update

Libor-OIS spreads have recently started to retreat from the wides hit in the middle of March. 1 year Libor-OIS spreads in USD reached as high as 45.25 basis points. They have since traded as low as 40.25bp. Notional volumes across all indices in March hit all time highs, 3 times the levels seen in 2017. […]

Swaps Data: A MiFID-shaped hole

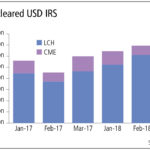

My monthly Swaps Review in Risk Magazine looks at: Global volume in Cleared USD Swaps at LCH and CME US Swap Execution Facility volumes US Off SEF volumes MiFiD II so far failing to provide meaningful data USD OIS Swap volumes The challenge for SOFR Please click here for free access to the full article […]