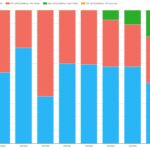

What’s new in CCP Disclosures – Q2 2025?

Clearing houses have published their latest CPMI-IOSCO Quantitative Disclosures for Q2 2025. Key takeaways Background Under the CPMI-IOSCO Public Quantitative Disclosures, central counterparties (CCPs) publish over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing, and more. CCPView has more than 8 years of these quarterly disclosures for 44 clearinghouses, each with multiple Clearing […]

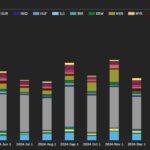

What’s new in JPY swaps in 2025?

Following our blog in April 2024, we further explore the volume expansions and market transitions in JPY IR derivatives. Key takeaways Cleared OTC interest rate derivatives (IRD) volumes As noted in our quarterly CCP IRD volumes blog, JPY IRD volumes exploded in 2024 and 2025. I wanted to look over a longer period to see […]

H1 2025 SDR-reported IR compression

Following our introductory blog, 2024 US SDR-Reported IR Compression, published in May 2025, we review today the same compression volumes for the first half of (H1) 2025. Key takeaways Background Note that SDRView is roughly half the total swaption compression volume, because trades are only reported to SDRs if they involve a US party. Nonetheless, […]

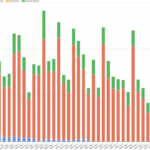

Volumes and most active names in credit derivatives – July 2025

Today we look at issuer names most actively traded in trades reported to US SEC Securities Based Swap Data Repositories (SBSDRs) in July 2025. The prior similar blog covered April 2025. Today’s iteration also includes a brief review of overall single-name CDS volumes. CDS on sovereigns We start with USD CDS on sovereign names. Table […]