aka “What I learned at the CFTC Roundtable”

This past week, Amir sat on a panel at the CFTC to discuss everything MAT. I sat in the audience and heckled. And took notes. I will share those with you below.

BACKGROUND

If you are an avid reader of our blogs, you’d know we’ve been tracking MAT since the inception of SEFs. “MAT” stands for “Made Available to Trade” and is the process of deeming what products must be traded on a SEF (Swap Execution Facility). It’s been full of controversy from first sight.

The G20 and Dodd-Frank demanded that exchanges be formed for OTC swaps. Historically, the bulk of swaps were traded over the phone and investors had very little price transparency beyond what their dealer told them a swap cost. SEF’s were to change all that – we were to have transparent marketplaces where barriers to entry would be reduced and price discovery could happen freely among all market participants.

While there have been many issues with the introduction of SEFs, complete with lovers and haters and winners and losers, it’s largely been a success, particularly given the pace with which the CFTC brought it to market.

While there have been many issues with the introduction of SEFs, complete with lovers and haters and winners and losers, it’s largely been a success, particularly given the pace with which the CFTC brought it to market.

One conceptual problem is defining what products need to be traded on SEFs. Swaps are not like bonds or futures where there is a finite list of products such that you could highlight the ones that need to be traded on the exchange. So in their rulemaking, the CFTC treated swaps much like exchange traded products, by allowing SEF’s to “list” swap products. Every product a SEF offered would be either “permitted” to be traded on a SEF, or “MAT” aka mandatory to trade on a SEF.

To become MAT, any SEF just needs to submit some paperwork (“self-certification”) to the CFTC expressing their assessment of why a product should be MAT. I believe there are 6 guideline criteria, and a SEF needs to justify their submission by at least 1 of the criteria. The criteria are things like liquidity, plentiful buyers and sellers, etc, etc.

Shortly after the October 2013 launch of SEFs, 5 different SEFs submitted MAT applications, and after much debate, some very liquid swaps in rates and credit derivatives were MAT’d. That list is here.

WHATS BROKEN

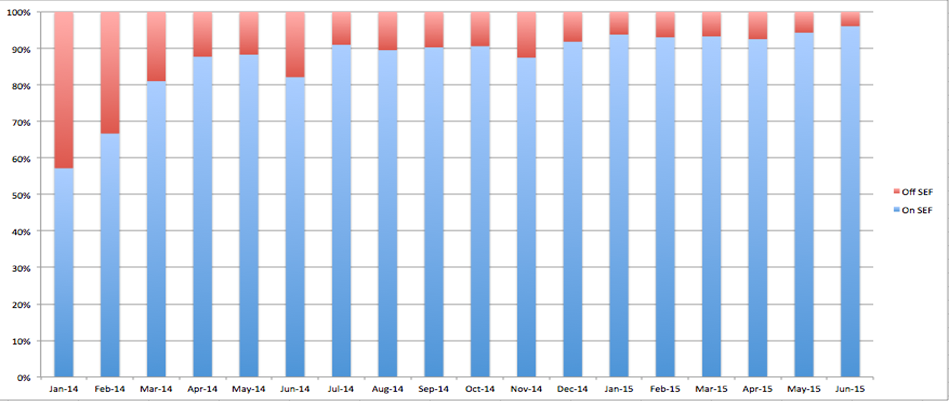

So after that flurry of 5 MAT applications, over a year has gone by with no more applications. MAT has stood still. We’ve been tracking SEF’s since inception and as a rule of thumb, since the MAT’s took effect in early 2014, the amount of trades registered on a SEF has hovered between 50 and 60 percent (for USD IRS). Most of those are MAT. Generally speaking, if the product isn’t MAT, it’s not trading on a SEF. And unless there is a user exception or it’s a block trade, everything MAT has traded on a SEF. So you can think of that 50-60 percent as roughly the portion of the market (in this case USD rate swaps) that are MAT.

As a benchmark, CDS index trades are roughly 90-95 percent on SEF.

And there are exceptions, for example there is no MAT products for all CFTC-governed commodities, FX and equity index swaps. Yet we do see activity in these products, particularly in FX NDF.

I suppose the thinking is generally that MAT-ing products improves transparency, liquidity and price discovery, so the questions would be:

- MAT applications have stopped. Why aren’t there any more?

- Only 50-60% of USD rates are trading on SEF, could that not be higher?

- Should the process be changed so that other bodies (eg CFTC) determine what is mandatory?

- Is there a risk that a SEF will just self-certify everything and there is no kill switch to stop it?

THE DISCUSSION

So here is what unfolded on the day. The CFTC agenda can be found here.

Panel 1 – MAT in other jurisdictions

The panel consisted of representatives from the US SEC, Japanese JFSA, and UK FCA. Roger Smith of the CFTC moderated.

What surprised me was that all three panelist basically said that their agency determines what is mandatory, and that the mandatory products were a subset of the clearing requirement. Edwin from the FCA noted that the UK rules seem to say something may be deemed mandatory by the FCA if:

- It is required for clearing

- It is available on a venue

- It meets a liquidity test

So if you require 5YR fixed/float swaps with certain criteria to be cleared, and a venue “lists” them, and you can deem them liquid, then they need to be traded on the exchange. It makes sense to me.

It was roughly then that I thought that Chairman Massad (who was in attendance) might just stand up, clap his hands and say “ok, let’s just do that then. Meeting adjourned”.

Alas that didn’t happen, and the meeting continued.

The process in these jurisdictions seems to be:

- Agency puts out a memo

- Public has a month to comment

- Goes into effect

Very efficient. Worth noting however that none of these agencies currently have mandatory trading yet (Japan will be in September) so it’s an academic discussion.

The other telling point was when Edwin (UK FCA) discussed the differences between OTF’s and MTF’s. The prior allows more bespoke transaction structuring / execution methods like phone-based broker workups. Commissioner Giancarlo made sure that this was repeated and clarified, as of course he is not a fan of the highly prescribed, cookie-cutter all-to-all SEF rules.

Panel 2 – Academia

CFTC Chief Economist Sayee Srinivasan chaired this panel, which included Amir, professors Darrell Duffie and John Hull, and Kevin McPartland.

Amir led off the second panel with a presentation showing some of our data, reinforcing the various degrees of performance we’ve seen in MAT’d products. He highlighted that:

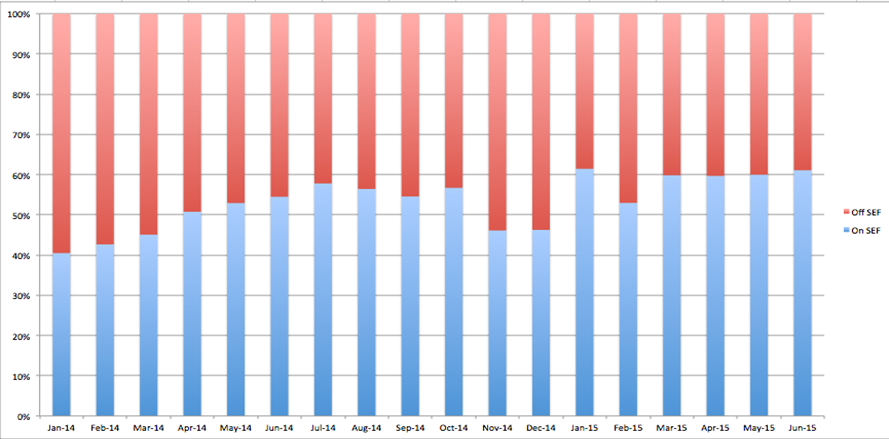

- CDS is already 90+ percent SEF-traded

- NDF is above 30% on SEF (a product for which there is no MAT)

- IRS hovers at 50-60%

- Adding other IRS tenors would budge that up ~5%

- Adding Fwd start would add another ~15%

- Remaining 20% is noise like compression, embedded options, truly bespoke, etc

Kevin referenced data from Greenwich Associates that seemed to corroborate what Amir presented, and had some valid references to electronic trading in other financial products which has followed similar trajectories, with the key thing being that the buyside will adopt electronic execution when it becomes the best way to execute.

I didn’t take great notes (in fact none) when the professors spoke, perhaps because no slides were used. I do recall Professor Duffie citing short dated physically settled FX as a massive risk that is not mitigated by CLS. I had not thought about that before, however that is a problem for a separate agency.

Professor Hull compared the liquidity in swaps to that of the housing market. The key suggestion being that the housing market works, and has brokers, phones and lesser transparency. As such, the CFTC should not be over-prescriptive in how you transact swaps. There’s some valid points somewhere in there, but probably not the best analogy.

They both however made one point that stuck in my head. They both discussed price transparency in a pre-and post-trade sense. Idea being that post-trade price transparency (ala SDR trade reporting) is good, but that pre-trade price transparency is better, ala an order book. It made we wonder if the CFTC (or many of the panelists) appreciate that order workups are taking place on some SEFs, granted only at the IDBs. Workups seem to be a very good solution for price transparency without the risk of getting clobbered (excuse the pun) in an order book.

Panel 3 – Industry Assessment

The last panel had representatives from liquidity providers, buyside firms and SEFs. Maybe it was just me, but by the time we got to this panel, I had thought it was a foregone conclusion that the CFTC would be taking over the MAT process and we just had to work out what that would look like.

I’ll bullet-point my takeaways from this:

Lots of debate on making the MAT process quantifiable. Such that the CFTC would define parameters (volume, OI, trades, etc) and then they could observe the data coming out of the market and have a little bell ring when some product hits all the criteria. The bell was not mentioned, that is my idea. But there was large support for having MAT driven more objectively from data.

Lots of debate on making the MAT process quantifiable. Such that the CFTC would define parameters (volume, OI, trades, etc) and then they could observe the data coming out of the market and have a little bell ring when some product hits all the criteria. The bell was not mentioned, that is my idea. But there was large support for having MAT driven more objectively from data.- Morgan Stanley suggested that a MAT product would require at least 2 SEFs trading it and at least 2 liquidity providers. Another panelist later said 5 and 5.

- Morgan Stanley pointed out that if MAT’ing was quantitatively driven, then there would be a need for an Un-MAT process (called “MUT”) when the data no longer supports it being MAT.

- Buyside representatives discussed technical hurdles involved for new MAT products. Not just for the buyside but for SEFs and liquidity providers. The Putnam representative gave an interesting case of the recent MBS-package relief rolling off and suddenly there was no combination of SEF and liquidity providers able to transact the packages (though I believe Tradeweb filled that need).

- Angela Patel of Putnam had another great comment about the “illusion of electronic trading”. I’d love to hear more, but the jist being that some of these trades that are perceived as electronically traded and STP’d still require phones, cutting and pasting and other manual intervention. She claimed her firm has a SWAT team for every new product they trade as it requires very thorough testing on the SEF and STP front.

- My favorite comment was that we need to treat packages as their own entity. Right now, we MAT a product and we end up in this frenzy trying to execute and process that product any time it trades in a package. Instead of the package exemptions, let’s make packages explicit in the MAT process.

- Stephen Berger of Citadel had a great comment – I believe he used the term “bogus fragmentation” – or perhaps that is just my bad note-taking. The idea being that liquidity in the swaps market is not as fragmented as we’ve all convinced ourselves it has become, and as such, this perception should not drive policy.

- Seemed to be some agreement that a hybrid solution is best – something like the CFTC taking ownership of the process but having an industry-chaired MAT committee to give sanity checks.

HERE IS MY PROPOSAL

Things are never as bad as they seem. The MAT process isn’t terribly broken and with some tweaking I think we’ll get there. I would generally recommend:

- CFTC own the process (get rid of “self certification”)

- Small MAT committee is formed with representatives from liquidity providers, buyside, SEFs, and a Clarus data junkie

- Establish quantitative, observable criteria (trades, price requests, missed orders, ability of liquidity providers to provide a price, and other “liquidity” measures) for a MAT product

- Implied in this is that package transactions are their own “product”

- Have quarterly reviews of measured data

- 3 month warning before MAT goes into effect

- A little Clarus “MAT” bell rings every time a new product is deemed MAT-able.

I’ll get started on the MAT bell.