Last month I wrote about SONIA market developments and how trading is progressing ahead of 2022 when Libor is expected to end. In this blog I extend this analysis to the USD markets. Much like SONIA, SOFR has seen some growth over the past year, which is to be expected as USD Libor is also widely expected to cease by 2022.

Here I turn to the USD OIS markets to see if there is any sign of SOFR uptake to replace USD Libor. The likely cessation date for Libor (end of 2021) is rapidly approaching and we should start to see SOFR volumes growing to replace Libor fixings post 2021.

The ARRC (Alternative Reference Rates Committee) in the US has published a timeline which looks for growth in the SOFR volumes in 2019.

But how is this progressing?

The USD OIS Markets

The USD OIS market is actually two markets: one referencing SOFR and the more established one referencing EFFR (Fed Funds).

The EFFR market has been trading for many years and has been used by many market participants.

The SOFR market dates from the introduction of SOFR by ARRC and first published by NY FED in April 2018. SOFR is the benchmark selected by ARRC in 2017 for use in certain derivatives as a replacement (or fallback) for USD Libior.

SOFR traded volumes should increase relative to Libor before 2022 and probably surpass EFFR in volumes as we approach the end of 2021.

Changes to OIS volumes since January 2018

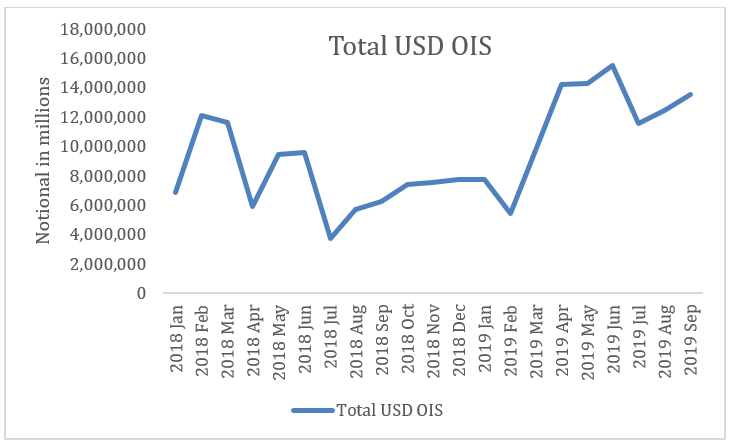

Firstly, I look at the total (EFFR plus SOFR) volumes from January 2018 until now. But note that the OIS volumes before April 2018 are only EFFR as SOFR was not published until then.

From CCPView the cleared volumes of USD OIS trades from January 2018 until October 2019 .

The graph does show growth in the USD OIS markets since 2018. Certainly, over the past year we have seen some growth in the total market.

As we have seen, the USD OIS market is actually the sum of the EFFR and SOFR OIS markets.

But how much SOFR and EFFR is traded?

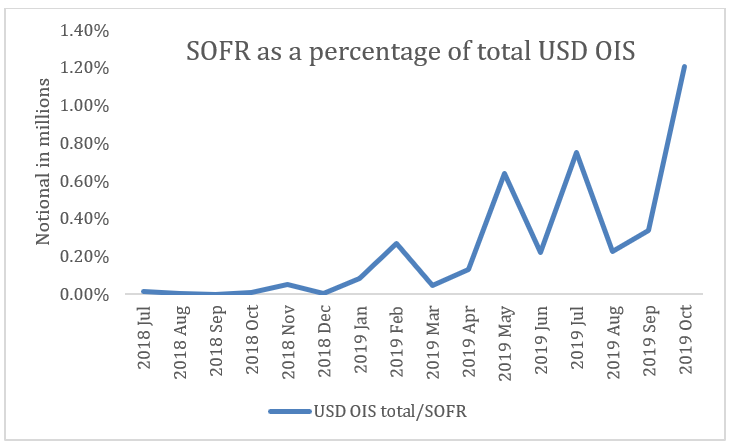

The following chart shows the percentage of the total OIS market that is attributed to SOFR volumes. (I used the Volume&OI tab in CCPView to get the total OIS and the RFR tab to look only at SOFR.)

And note the scale on the Left hand axis!

Yes, we are seeing an increase in the percentage of the total OIS market traded against SOFR but the percentages (currently 1.2%) are still rather small.

The OIS market is still largely traded against EFFR but the SOFR component is increasing, albeit from a low base.

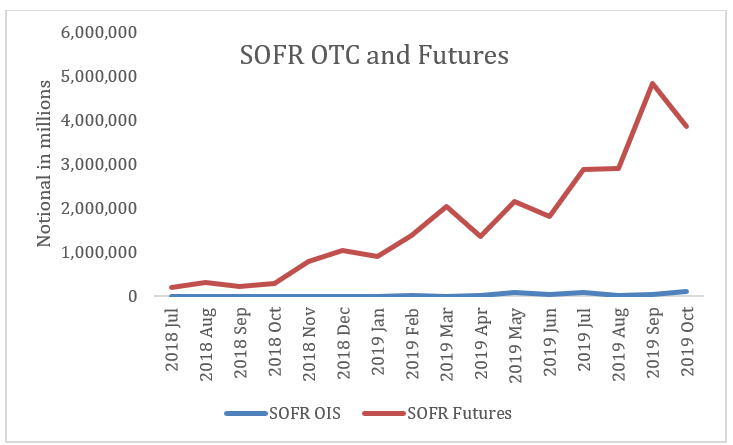

But there is also another SOFR market: futures contracts. Again, using CCPView, I have also looked at the exchange traded (ETD) SOFR volumes and charted then with the OTC OIS volumes in this chart.

Clearly the SOFR ETD volumes are substantial, rising and significantly greater than the OTC volumes.

If we add the ETD and OTC SOFR volumes, they are actually a reasonable percentage of the OTC EFFR market (about 20 – 30%).

But remember, the ETD Fed Funds futures contracts also trade very large volumes – so it appears EFFR trading is still very much larger than SOFR trading.

OIS/Libor trading volumes since January 2018

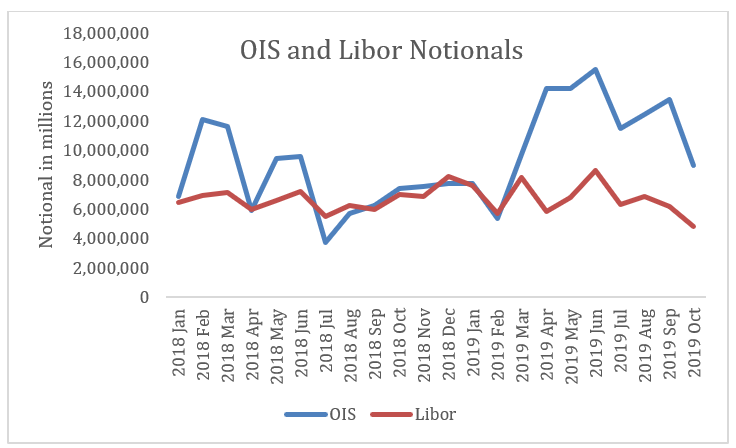

l now compare the USD Libor/OIS (total) derivative trading volumes.

The next graph shows the total market traded volume per month since January 2018.

The total OTC OIS notional volumes traded per month are now actually greater than the Libor notionals. But remember, the OIS volumes are largely EFFR rather than SOFR.

It is important to also look at the different maturities to look for any changes. Historically the USD OIS markets were very active in maturities less than two years while Libor trading dominated longer maturities.

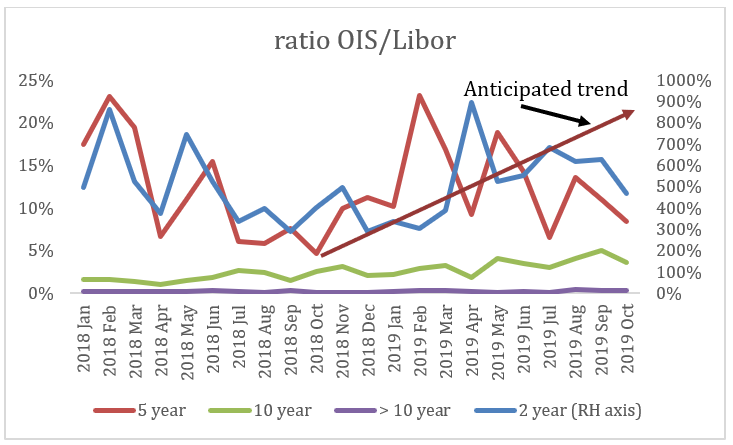

The following chart shows the OIS percentage of the notional volumes per maturity since January 2018. Note that the 2-year bucket is the right-hand scale.

As expected, OIS dominates trading in maturities less than 2 years with percentages around 400 – 900%. This is quite expected.

But trading in longer maturities is less: around 5 – 20% for the 5-year maturity and less than 5% for longer maturities.

The trend line relates to the 5-year maturity but the growth has not been consistent. There is no substantial migration from Libor to OIS evident at this stage and particularly in maturities longer than 2 years.

Why does lack of migration in longer tenors matter?

My previous blog on SONIA stated the following:

‘The expected date for Libor cessation is 2022 so trades longer than 2 years (i.e. after December 2021) with a Libor rate fix after 31st December 2021 will likely have exposures to a benchmark that may not exist!

Certainly trades out to 5 years (and longer) tenors will reference a benchmark (Libor) that will be subject to probable cessation and revert to a fallback. So why are traders and hedgers taking this risk and not simply moving to SONIA?

This lack of urgency remains a mystery but is still a fact. The derivative markets must be waiting for something to produce the risk longer than 5 years that will create demand for the derivatives.

The missing component could the cash trades; for example bonds, loans and securitised products. The risk generated from these trades has historically created a need to hedge with derivatives which, in turn, drives a secondary derivative market to spread the risk.

Also, speculation is a major component of longer-dated derivative traded volume. We will need to see a significant migration of this activity to SONIA if volumes are going to exceed Libor turnover.

Either way, volume creates liquidity which attracts further volume. The challenge is how to start a significant migration to SONIA. So far in 2019 there is little evidence that derivative markets are making a significant move to SONIA from Libor.’

Rather than repeat myself here, exactly the same comments can be made for USD OIS and SOFR in particular.

Summary

Much like GBP, the USD markets are still trading Libor benchmarks well past 2022. Despite the obvious challenges this will create there is no significant move towards SOFR.

The US OIS markets have the additional challenge of trading two different benchmarks: SOFR and EFFR. Trading in EFFR is still significantly greater than SOFR.

The ARRC-recommended replacement for USD Libor is clearly SOFR so why is EFFR still so popular and why are traders still referencing Libor well after 2022?

Perhaps 2020 will be the pivotal year rather than 2019.

As the countdown to 2022 continues, it appears there is still much work to be completed to fully establish SOFR trading in longer maturities.

And the longer this takes, more Libor-referencing trades will be traded and will therefore need to be amended as we approach 2022.