- We look at the mechanics and definitions of a Forward Rate Agreement (FRA)

- It is the simplest interest rate derivative to price, trade and settle

- Market conventions tend to be split between Commonwealth currencies and the rest of the world

- There are many reasons to trade the product, resulting in nearly $10trn per month in volume.

Forward Rate Agreements

The FRA market is inherently linked to the Short Term Interest Rate futures market in the appropriate currency. So if you haven’t already, please head over to our “Mechanics and Definitions of Short Term Interest Rate Futures” blog before you go any further.

Definition

We define an FRA as:

A cash-settled contract-for-difference on a short-term interest rate that fixes on a future date.

I make that 14 words. The investopedia entry extends to 750+ words, which is somewhat concerning for the most simple of the products we trade in Interest Rate Derivatives!

Mechanics

- Define the Index you are going to trade. For example, 3m USD Libor.

- Pick a value date in the future – e.g. 14th December 2016.

- Decide whether you think rates will go higher or lower between now and the fixing date – which in the case of USD Libor is two days prior to the value date, on 12th December 2016.

- If you think interest rates are heading higher, then you should buy the FRA. This means that you agree to “pay” a fixed rate of interest. If 3m USD Libor fixes higher than the agreed contract rate on the 12th December 2016, then you make money. If 3m USD Libor fixes lower than the agreed contract rate, then you lose money.

- You now need to calculate how much you have made or lost. For most FRAs, this is very simple:

\( \ (Contract Rate – Fixing Rate) * Notional * \frac{Days}{DayCount} * Discount Factor\)

A Subtlety

What discount factor should we use in the above equation? That is a good question. Bear in mind that FRAs were initially traded in a much simpler world – namely, the one in which we discounted all cashflows at Libor. Therefore, for almost all FRAs currently traded, we calculate the Discount Factor as:

\( \frac{1}{1 + (Fixing Rate * \frac{Days}{DayCount}))}\)

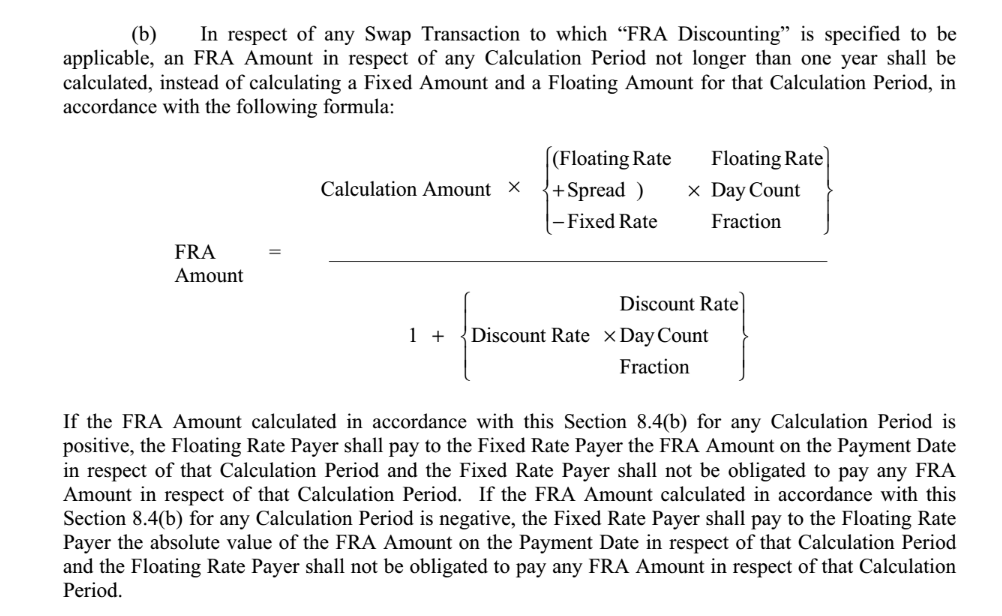

This enforces Libor discounting on the product. A couple of offshore markets were wise to this back in the day, and as such the AUD and NZD FRA markets actually employed a “FRA Discounting” methodology as defined in the ISDA 2006 definitions:

It was up to the counterparties to therefore define a “Discount Rate” or the “Spread” to use. In practice, some confirmations were poorly worded and you ended up arguing on each settlement date over whether to use the Floating Rate (like all other currencies) or the Contract Rate to discount the cashflow!

Market Conventions

Broadly speaking, we can split the market into Commonwealth Currencies (AUD, CAD, GBP, HKD, NZD, ZAR) and the rest of the World.

Commonwealth currencies are “same-day settlement” currencies. This means that a GBP Libor fixing today is for value today. In FRAs, only once the fixing is announced at 11am London time can we calculate the amount of settlement required. This amount must be settled on the same day. This can cause some operational headaches. It is sometimes tricky to make these payments in e.g. AUD if you happen to work on the West Coast of the USA for example.

These “Commonwealth” currencies generally employ an Act/365-Fixed day-count convention. Most other floating rate indices that a FRA might be based on are Act/360, aside from a couple of Asian currencies such as SGD. Having just written that sentence, it strikes me that Clarus may launch a Microservice to verify these market conventions and to monitor new ones. Feel free to contact us if that may be of interest.

These currencies aside, most FRAs have a fixing that has a value date two days in the future. That therefore means that for a FRA value Wednesday, we will know the settlement amount by the end of the day Monday. This gives us time to instruct payments and make sure that settlement is smoothly completed.

Motivations for Trading

In the interbank market, it is common to ask “where is 0x3s today” or “0x3s tom”. Just to be clear, the “x” is not pronounced.

These are important forward-looking instruments:

- 0x3s today describes a FRA fixing today (so value T+0 in GBP and T+2 in USD). This would only be asked before 11am London time, ahead of the published fixing.

- 0x3s tom is therefore a FRA fixing tomorrow. This is commonly asked in the afternoon and used to close curves at the end of the day.

These simple instruments are key components of a curve, particularly during crisis times when fixings can jump 25 basis points from day-to-day. In essence, all of the information value of an FRA (or fixing) is immediately lost as soon as it is published. Therefore most curves do not calibrate to today’s fixing, but rather the T+1 fixing. Retaining the actual fixing is akin to using the opening prices rather than closing prices for futures every day!

The motivation for trading varies depending on market conditions. FRAs can be used for a number of reasons:

- To express a view on central bank policy. Due to their OTC nature, the ability to choose any fixing date can be used to pin-point decisions. However, an OIS is typically a preferable product for these purposes in current markets.

- To express a view on credit worthiness of the banking sector. FRAs tend to trade against unsecured lending indices (e.g. Libor). Under NIRP or ZIRP, Rates can still increase (decrease) when monetary conditions tighten (loosen) – even in the absence of a change in market expectations of the main policy rate.

- Swap book hedging – a 10 year swap traded today will have different fixing dates to one traded tomorrow (or yesterday). The date mismatches in fixings can be hedged using two FRAs on each reset.

Volumes are Significant

I’ve said this before, but it is worth saying again. Volumes in FRAs are huge.

Showing;

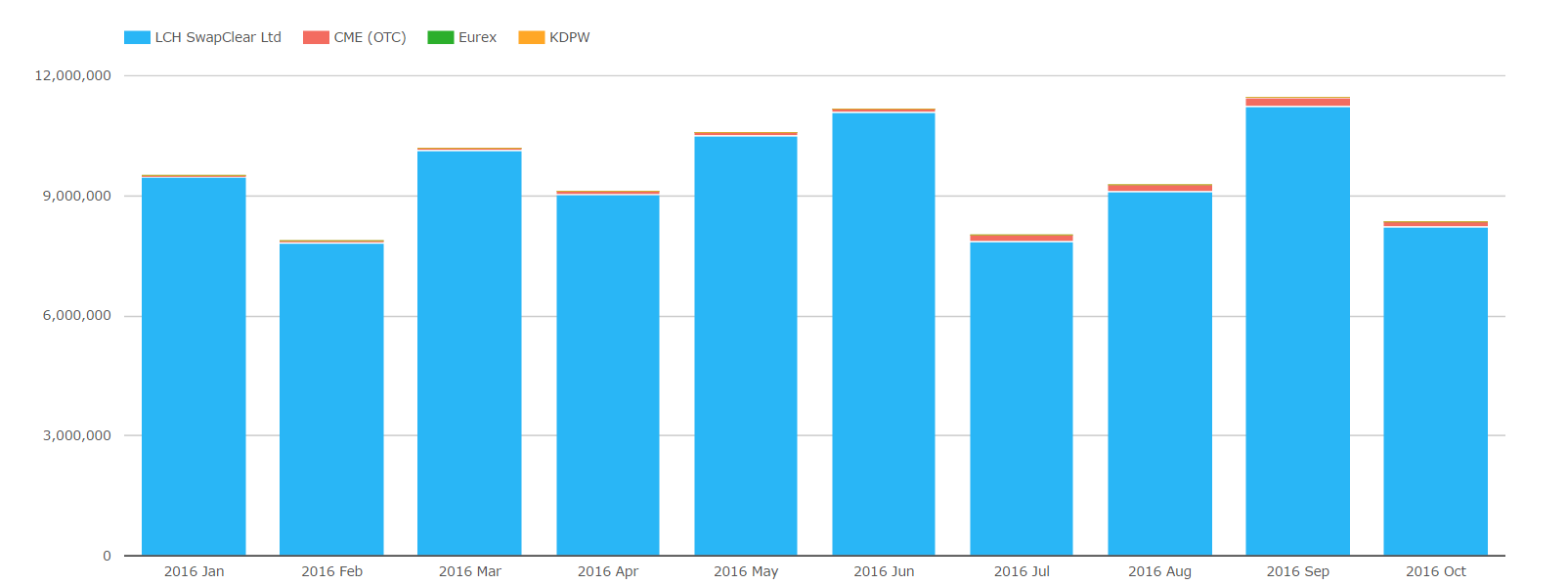

- Our CCPView data product shows the volumes of Cleared FRAs traded per month across all CCPs.

- So far in 2016, $95.6trn has been cleared.

- USD FRAs alone have seen $53trn trade.

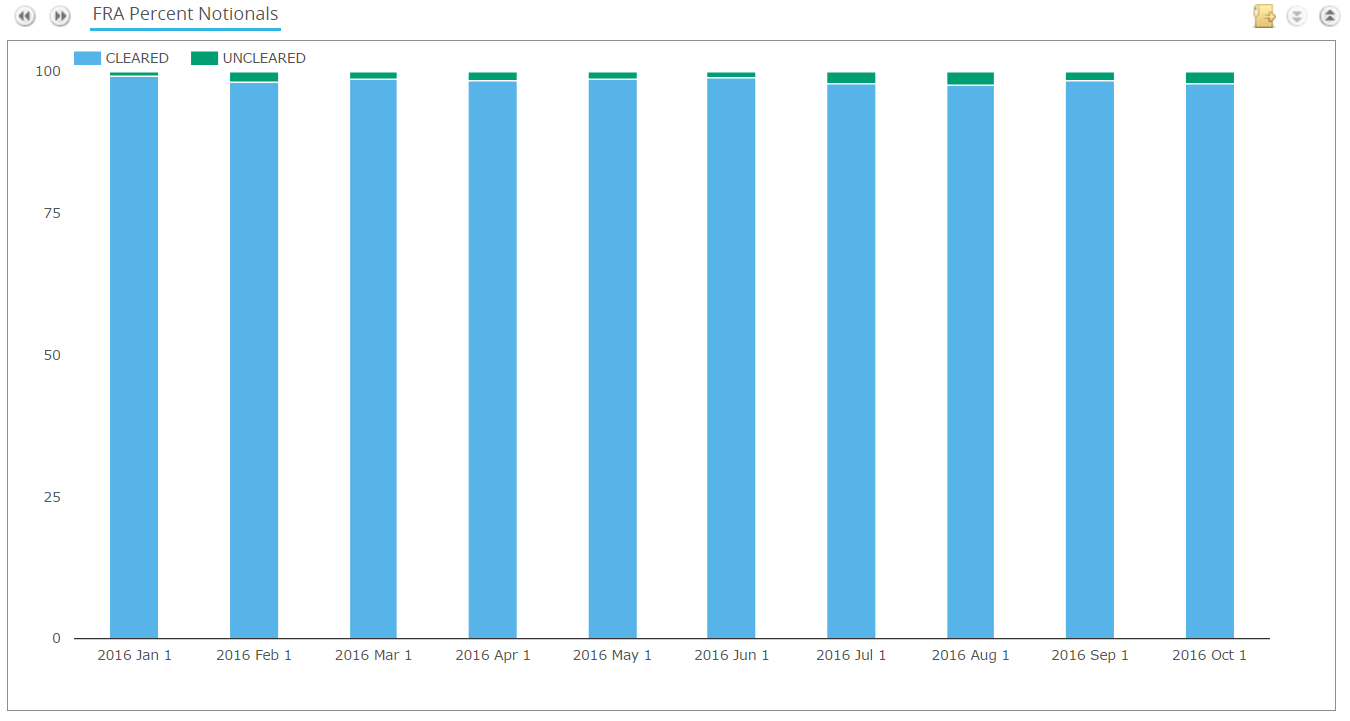

- This is almost exclusively a cleared market. From SDRView, we can see that ~98% of notional every month is cleared:

In Summary

- An FRA is a cash-settled contract-for-difference on a short-term interest rate that fixes on a future date.

- Settlement is a simple calculation that assumes Libor discounting.

- Most currencies settle on an ACT360 T+2 basis, with the Commonwealth currencies settling on an ACT365F T+0 (“same-day”) basis.

- FRAs are used as building blocks on most Interest Rate Swap curves, providing valuable information on market expectations for central bank policy.