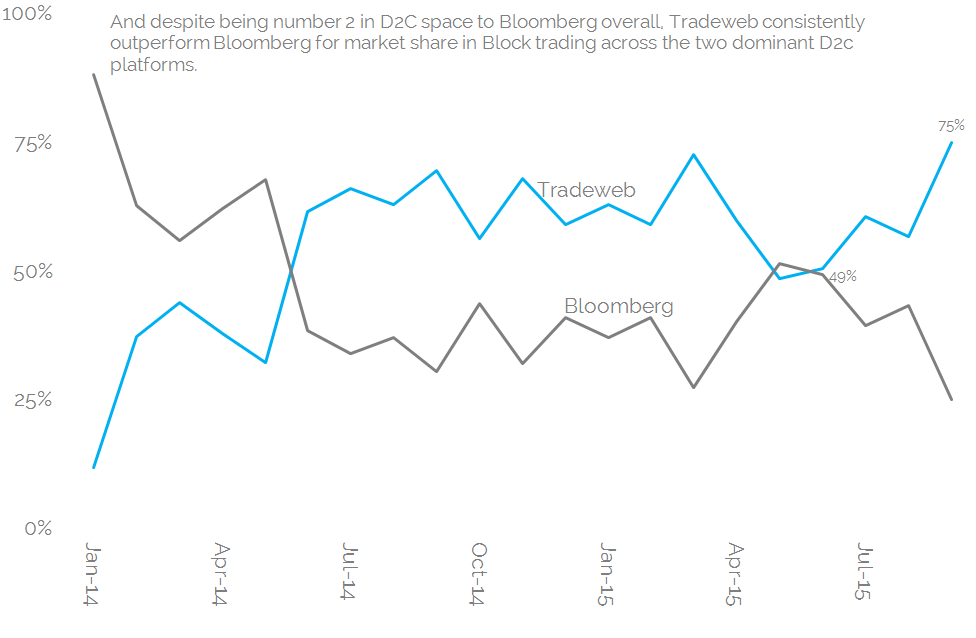

- Tradeweb appear to have a 75% market share for Dealer-to-Customer Block trading

- which has increased substantially since the early days of SEF trading

- This is against a backdrop of fairly stable overall block activity…

- …but more and more block trades are being done on-SEF rather than off-SEF.

- Sadly, this may raise a question over good ol’ voice broking…

- ….as shouldn’t these huge trades all be done off-SEF, secret-squirrel style?

Tod has covered the background to this topic before when he looked at block trading in a blog last year – “CFTC Block and Cap Sizes”. I’ve done some googling, and I’m pretty certain we are yet to transfer to the “post-initial” phase, but I sure hope Tod has taken the garbage out by now….

Stuck as we are with the same cap and block size thresholds since trade reporting began, I thought I’d have a look at the data available and see if there’s been any changes. And do it quickly, in case the CFTC should, ahem, maybe think about re-running its’ analysis….possibly via an easy-to-interrogate, curated data service like Clarus provide?

D2C and D2D Dichotomy

One thing is for sure – there seems to be a distinct difference between the handling of Block trades between the D2C and D2D SEF platforms. I’m assuming this is due to the fact that the D2D SEFs always have the ability to transact a trade off-SEF. But it’s worth noting that Tod mentioned there is indeed confusion over the rule:

“Block Size: The notional threshold for which a trade can be a “Block” and hence must be executed away from a SEF. (Disputing “must be executed away” and “can be executed away” is the subject of another article).”

As a potential result of this confusion, we know the block amounts transacted on-SEF at the D2C SEFs (Tradeweb and Bloomberg, available via SEFView). But D2D SEFs do not strip out what is block-related notional and what is transacted “normally”. We’ll revisit this at the end of the post.

The Data

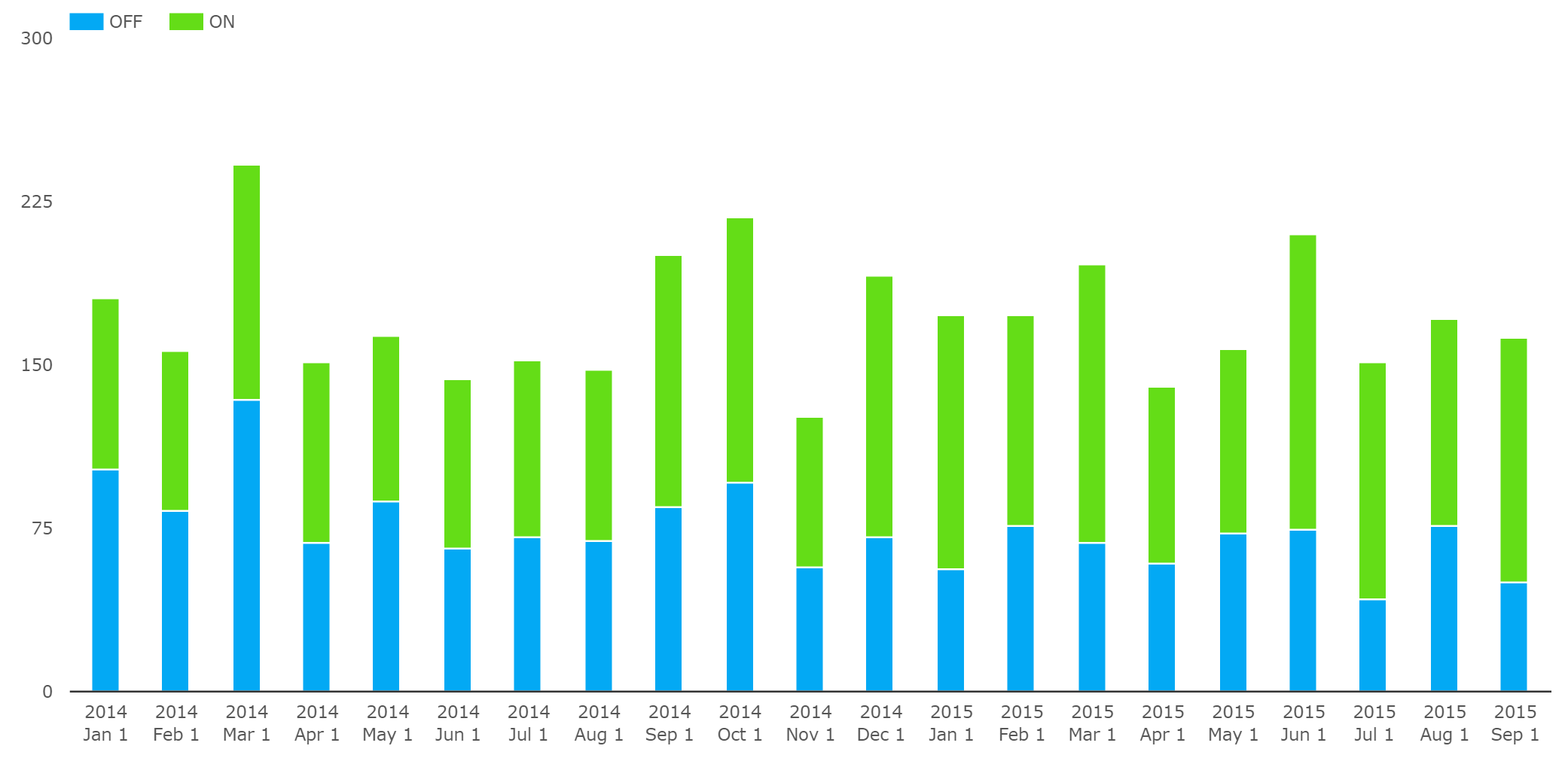

We’ll use the new CustomView within SDR Res to look at the first cut of the data. This shows how much block trading activity we’ve seen since the beginning of 2014 on a month-by-month basis:

Showing:

- Block trades executed both On- and Off- SEF in DV01 terms for vanilla USD IRS Fixed/Float swaps.

- If there is still any confusion over the Block trading rule, it is clear that block trading activity does occur both On and Off facility!

- No clear pattern for when peak block trading activity occurs, although there appears to be slightly more activity during IMM roll months.

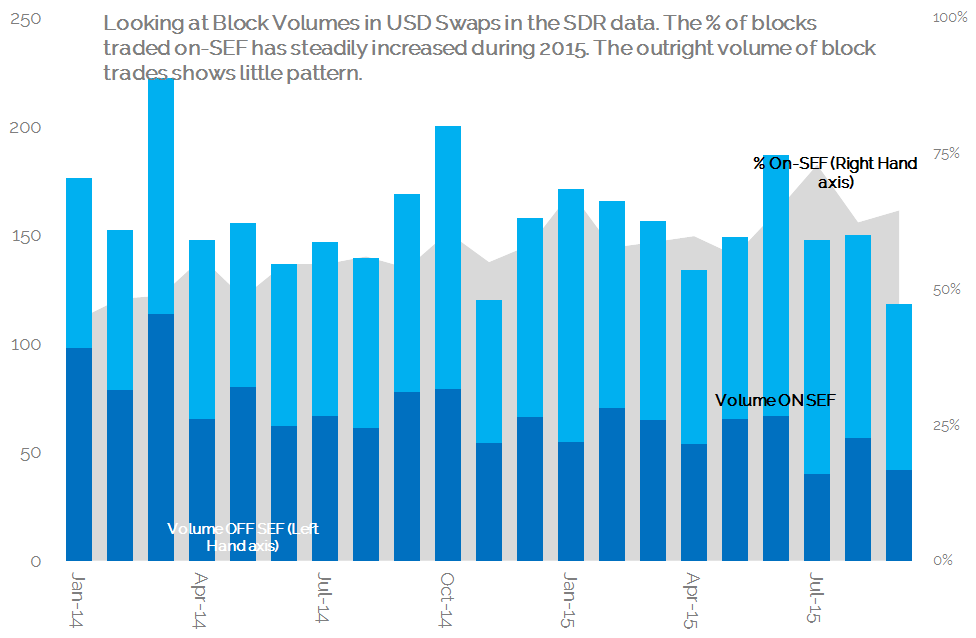

The custom view also allows us to strip out Compression and List activity. We know that this form of execution has been a feature in our markets over the past 2 years, and may not necessarily reflect where true liquidity lies. Stripping out these volumes and looking at the percentages traded On- or Off-SEF is interesting:

Showing:

- Back in January 2014, only 44% of block trades were transacted on-SEF.

- This was the low for the time-series, and we’ve seen a steady rise ever since, reaching a peak of 73% in July and averaging over 66% for the past quarter.

- Put another way, at least 2 out of every 3 block trades now occurs on-SEF.

Huh! So, in answer to Tod’s confusion, I guess the market has voted with its’ feet and decided that Block trades are fine to execute on-SEF!

Customer vs Dealer SEFs

There’s something else in the data that makes for fascinating geekery as well though. As we know, D2C platforms have shown stellar performance during 2015, accounting for almost 100% of on-SEF volume growth in Rates space this year.

And these SEFs are the only ones (that I can see) who separate out Block volumes from non-Block on their daily reporting. And that gives us yet another time-series to interrogate!

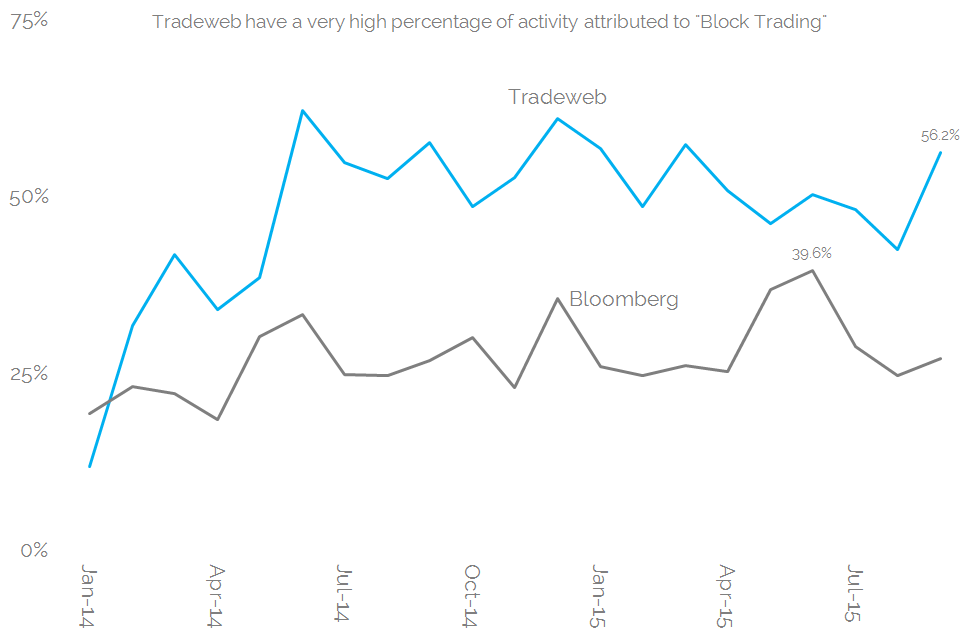

So what percentage of D2C business is Block trading?

We know that D2C now make up over 55% of all trading volumes in USD swaps, even when excluding compression-related activity. So how much of this is related to block trading? That question actually largely depends on whether we are looking at Tradeweb or Bloomberg:

From that chart, we can see that:

- Both platforms have seen increased block volumes relative to their overall volumes since Jan 2014.

- These charts are in DV01 terms, but much the same applies if the numbers are re-based to notional volumes.

- So it is fair to say that some of their market share growth has been driven by this increase in block volumes.

- Block trading is particularly active on Tradeweb, where we’ve seen up to 60% of their volumes being traded as block.

- We cannot strip-out for Tradeweb how much of their block activity is Compression related…..

- …but we can for Bloomberg.

- On average, only 4% of block trading on Bloomberg has been Compression-related. BUT June 2015 showed that over 50% of their block trading was done via Compression. I’m positing the IMM roll for that particular outlier!

Overall, it’s interesting that the best performing platforms this year are also the best places to go and trade a block if you want to do it on-SEF.

And if you have a block to trade on-SEF….

….the market is choosing Tradeweb. We know that Bloomberg are seeing some impressive market-share growth overall, but in this particular area of the market, Tradeweb really does rule. They now see a huge 75% of Dealer-to-Customer block trades go through on their platform:

It’s worth mentioning that this 75% figure is so high that my initial assumption was that Tradeweb have some kind of “block trade reporting” tool for trades arranged off-facility – maybe akin to reporting an out-of-order book block or EFP in futures space. But we checked with them, and no such tool exists. In which case, it’s a mightily impressive market share!

Are we therefore seeing a D2C market place where Bloomberg is used for small trades, and Tradeweb is where you go for execution of good size? I’ll have to revisit that question in the data another time….

In Summary

Given the overall picture, it’s an interesting side-story within the data, which can be summarised as:

- D2C platforms have seen all of the growth in overall on-SEF swap volumes in 2015

- There hasn’t been any noticeable increase or decrease in overall Block trading activity in 2015 in the SDR data. This applies equally to on-SEF or off-SEF trades.

- However, block trading activity IS increasingly becoming an on-SEF activity.

- With nearly 70% of all block trades now occurring on-SEF (by capped volume).

- Even excluding Compression and List trading protocols doesn’t change this fact.

- We can’t tell from the data if IDB-run D2D platforms transact Block trades On- or Off-SEF…

- …because they do not separate out these volumes in their daily reports.

- However, given that Block trading volumes off-SEF are falling relative to on-SEF volumes….

- ….it doesn’t paint a pretty picture for voice businesses (if they are being reported as off-SEF trades).

- But equally, even if the D2D SEFs are reporting block trades as transacted on-SEF, the data shows that Tradeweb and Bloomberg both have a high percentage of their overall activity as block trading – suggesting they are winning market share from the D2D sector even for large trades.

- Of course, D2D SEFs can hopefully point to a higher average block size relative to the D2C SEFs, and higher revenue per basis point of risk transacted…..

- …but they must also be aware that platforms that don’t have a voice-supported work-stream to rely on are doing more and more large trades.