TLDR;

- A new standard way of messaging across CCPs could achieve some of the objectives.

- Taylor series expansion of IM changes day-to-day would provide necessary transparency.

- I believe that it is unlikely that Clearing Mandates will build, maintain and monitor margin replication tools for 30+ CCPs.

- All bullet points in the content below are AI-generated by Google Gemini. I promise I did read the BCBS paper, but I wrote only the opinion, not the summaries.

For anyone interested in the BCBS paper/consultation on “Transparency and responsiveness of initial margin in centrally cleared markets – review and policy proposals” (and with a title like that who wouldn’t be interested in it?!) I will try to summarise the 64 pages in 1,200-odd words.

Some of the thoughts that I have on the proposals may be a little surprising….

Policies One & Two

- Policy Proposal: CCPs should provide margin simulation tools to all clearing members and their clients.

- Functionality: These tools should allow users to calculate IM requirements under various market conditions for different portfolios.

- Objective: Improve transparency and risk management for participants in centrally cleared markets.

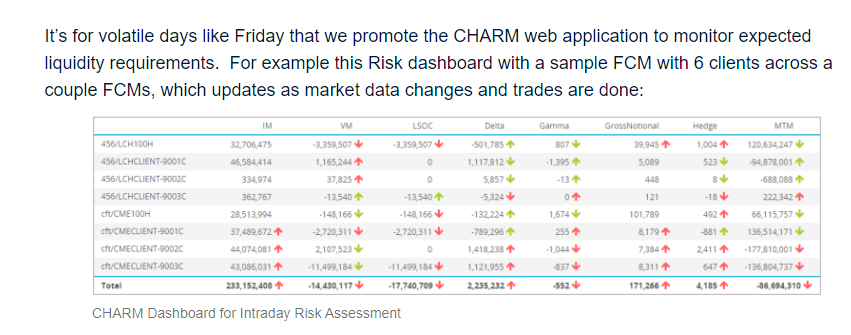

As a reminder, Clarus CHARM calculates Initial Margin and provides analytics to forecast potential liquidity requirements.

This policy could almost have been written by Clarus themselves…BUT…

My personal take is that most CCPs already provide margin simulation tools. Most of the time, the issue is not the availability, and sometimes not even the functionality, of these tools. It is a question of large Clearing Members having to maintain connections to over 30 CCP margin tools without any standard messaging, functionality or formats.

CCPs, largely as a result of the Clearing Mandates, have been able to enforce their own standards on their members. There is no standardisation across CCPs.

I would therefore recast this policy as “CCPs should create a single standardised messaging format/protocol so that Clearing Members can access margin simulation and portfolio positions in an identical manner across different CCPs”.

Comment below if you agree/disagree….

Policies Three & Four

- Disclosure of CCP model documentation: CCPs should make documentation regarding their margin models available to clearing members. This includes explanations of how key model parameters are calibrated and the logic behind margin add-ons.

- Public disclosure of anti-procyclicality (APC) tools: CCPs should publicly disclose the tools they use to achieve anti-procyclicality in their models. Anti-procyclicality refers to adjusting margin requirements in a way that counteracts economic cycles.

- Standardized metric for margin responsiveness: CCPs should disclose a standardized metric to measure how responsive their margin requirements are to changing market conditions.

Will the level of detail in the proposed disclosures be sufficient for Clearing Members to replicate margin calculations themselves? This is a very conservative approach for a clearing member to take (which is probably a good thing) and is certainly necessary if you are going to dispute a CCP’s calls. But are you? Should you? Can you?

A Taylor series expansion of where the IM call is generated (change in risk, change in tail scenarios, change in add-ons) should be sufficient to sanity check the IM call.

There is surely room for someone, somewhere to check the validity of the CCP IM calls. When I traded, I never left the office if I had more than £25k of “unexplained” PnL (positive or negative) after closing my book. That may say more about me than about risk management practices, but you can imagine a process whereby a CCP has to manually check any IM call that has more than “X” variation from the predicted Taylor Series calculation.

(I assume that readers are familiar with Taylor Series: change in market rates * risk at start of day + value of new trades booked today = expected PnL + time decay of portfolio from T-1 to T).

Policy Five

- CCPs should provide more granular reporting of margin-related data through Public Quantitative Disclosures (PQDs). This would include breakdowns of important components of initial margin (IM) requirements.

- CCPs should report margin-related data more frequently and with shorter reporting lags. The proposal suggests moving from quarterly reports with a two-month lag to potentially daily reports.

- All PQD data should be reported consistently and accurately. The Margin Group notes that this may require the development of standardized definitions for key terms.

This could have been Policy One as it is simple, easy to implement and highly achievable (and would fit nicely into CCPView Disclosures). A big “yes please” from us.

Policy Six

- Public disclosure of a new standardized measure of margin responsiveness: CCPs would disclose a metric showing the relative change in initial margin (IM) compared to the relative change in volatility over the same period. This aims to help market participants understand how much IM requirements respond to changing market conditions.

- CCPs to disclose additional qualitative information alongside the standardized metric. This could include reasons for significant margin changes, such as price movements or changes in risk assessments by the CCP.

- Potential for CCPs to report margin responsiveness at the single-contract and portfolio level. The current proposal focuses on portfolio-level reporting, but further consultation is requested to determine if users would benefit from more granular data.

This sounds like some very interesting academic work here. Again, this is “Taylor Series”-like to me. What is the “gamma” of the IM model (how does it change with a change in underlying rates)? This policy isn’t about Clearing Members replicating CCP margins, but better understanding how the margin model reacts/has reacted.

Policy Seven

- CCPs should identify and define an analytical and governance framework to assess responsiveness. This framework should consider the CCP’s business lines, risk profiles, and how the model responds to changing market conditions. The aim is to balance margin coverage, cost, and responsiveness.

- CCPs should communicate this framework to relevant authorities. This would allow for regular monitoring of the performance of initial margin models and to trigger reviews of model parameters if needed.

- The framework should be used to assess the effectiveness of anti-procyclicality (APC) tools. APC tools aim to adjust margin requirements counter to economic cycles, so they are less stringent during downturns.

I imagine all CCPs have these “frameworks” already in place as part of their own internal governance/risk monitoring. They probably also already communicate these to their lead-regulators.

Policy Eight

- CCPs should have clear governance procedures in place for using model overrides. These procedures would define when it’s appropriate to override the CCP’s standard margin model and who has the authority to do so. The procedures should also outline how these overrides are documented and reviewed afterwards.

- CCPs should publicly disclose relevant information on when and how they use model overrides. This disclosure should include the types of scenarios where overrides might be used and the rationale behind them. The CCP should also disclose the aggregate size and duration of these overrides compared to the unadjusted model requirements.

- CCPs should establish clear guidelines for monitoring overridden risk variables. This would ensure the CCP can track the impact of the overrides and assess their effectiveness over time.

When can a CCP break from “BAU” and manually intervene? There are probably stringent reasons for this in each of the CCP Rulebooks, so maybe this is trying to take some of the discretion/wriggle room away?

Policy Nine

We now move away from CCP-focused policies and turn attentions to Clearing Members (and their relationships with their clients).

- CMs should provide sufficient transparency to their clients regarding how client add-ons are calculated. This should include a detailed explanation of how client add-ons are calibrated (e.g., through margin multipliers, buffers, or internal margin models) and how the triggers or thresholds for their use are set.

- CMs should inform clients when they are adjusting their calibration of client margin add-ons. Clients should be informed without needing to request this information, and should be provided with sufficient notice.

- CMs should disclose to their clients backward-looking information on the maximum, minimum and average differences between client margin requirements set by the CM and the margin requirements of the CCP over a defined period of time. This disclosure can be made through reports or other means.

This all sounds very reasonable in light of what the CCPs are potentially being asked to do…

Policy Ten

- CMs report more data to CCPs quarterly: This includes details on exposures, default fund contributions, and margin calls, allowing CCPs to better assess risks.

- CMs disclose client add-on calculations: Clients get clearer explanations on how these add-ons are calculated and adjusted.

- CMs inform clients about add-on adjustments: Clients are proactively notified when their specific client margin add-ons change.

Does Policy Ten teach us that market participants cannot just ask, ask, ask of CCPs without there being some type of comeback? Will Clearing Members really report to CCPs their positions at other CCPs? Would CCPs even know what to do with this data? This sounds a bit like policy over-reach to me, despite the fact it would indeed be fascinating information!