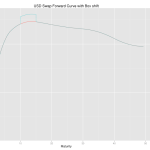

Swap Equivalents via Waves

In a recent paper, “Calculating Delta Risks and Hedges via Waves (2015)“, Hagan deals with an old practical problem–determining risk and hedges on an interest rate book. In older systems a delta hedge report is often implemented by perturbing quotes used to construct the yield curves, restripping the curves and then revaluing the book. As […]

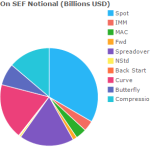

May 2015 Review – CCP Basis and Increased Client Flows

A lack of market volatility didn’t prevent healthy volumes this month. CCP Basis trading emerged in the D2D market. In USD IRS, extensive activity in Butterflies led to a rebound in volumes from the April lows. Most of this increase was seen on Dealer to Client SEFs, helping them to a 55% market share year-to-date. USD On-SEF […]