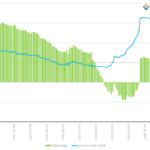

LIBOR Fallbacks – What will the GBP spread be?

We take a look at historic data for SONIA and GBP LIBOR. ISDA’s work on LIBOR fallbacks allows us to look into the potential values of the historic spread. We compare to the forward-looking LIBOR-OIS spreads to the backward looking compounded RFR values. Initial analysis shows that the look-back period will be an important consideration. […]

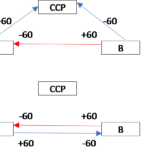

Reducing Counterparty Risk of Uncleared Derivatives

In my previous posts I concluded that uncleared counterparty risk is bigger than traded notional figures suggest and that, so far, UMR has only driven a limited further shift towards clearing. Here, as promised, I take a spin through approaches which complement new trade clearing and can also improve OTC uncleared counterparty risk efficiency. Summary […]