What’s new in CCP Disclosures – Q2 2025?

Clearing houses have published their latest CPMI-IOSCO Quantitative Disclosures for Q2 2025. Key takeaways Background Under the CPMI-IOSCO Public Quantitative Disclosures, central counterparties (CCPs) publish over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing, and more. CCPView has more than 8 years of these quarterly disclosures for 44 clearinghouses, each with multiple Clearing […]

What’s new in JPY swaps in 2025?

Following our blog in April 2024, we further explore the volume expansions and market transitions in JPY IR derivatives. Key takeaways Cleared OTC interest rate derivatives (IRD) volumes As noted in our quarterly CCP IRD volumes blog, JPY IRD volumes exploded in 2024 and 2025. I wanted to look over a longer period to see […]

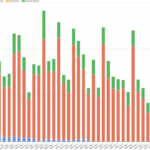

Volumes and most active names in credit derivatives – July 2025

Today we look at issuer names most actively traded in trades reported to US SEC Securities Based Swap Data Repositories (SBSDRs) in July 2025. The prior similar blog covered April 2025. Today’s iteration also includes a brief review of overall single-name CDS volumes. CDS on sovereigns We start with USD CDS on sovereign names. Table […]

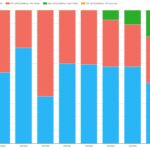

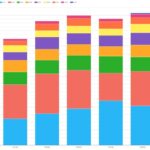

Q2 2025 CCP volumes and share in CRD and FXD

This blog reviews central counterparty (CCP) volumes and market share for cleared credit derivatives (CRD) and FX derivatives (FXD) in Q2 2025. For all-currency CRD, comparing Q2 2025 with Q2 2024, we see 45 percent volume increases, with indexes up 46 percent, single-names up 11 percent, and swaptions up 152 percent. Analyzing by currency shows that: […]

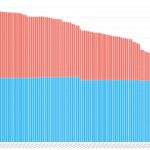

Swaption volumes by strike – Q2 2025

This post looks at USD swaptions activity in Q2 as part of our regular quarterly coverage, the most recent of which was Swaption Volumes by Strike – Q1 2024. We use SDRView data, which shows all trades reported by US financial firms to US SDRs. If you are new to swaptions, some basics are outlined […]

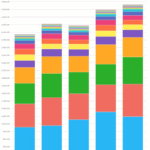

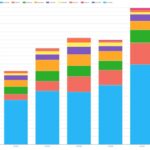

Q2 2025 CCP volumes and share in IRD

Clarus CCPView has daily volume and open interest (OI) data published by each CCP, which is filtered, normalized, and aggregated to allow meaningful volume comparisons. This blog looks at single-sided gross notional volume in vanilla cleared swaps referencing IBORs and RFR indexes for quarter two (Q2) 2025 and the prior four quarters in all major currencies and regions. This comprises: Read […]

CAD swaps – what’s new?

Given that over a year has passed since CORRA cessation, I wanted to illustrate the transition using CCPView and SDRView volumes. So, I will bias the 2025 edition of this blog towards CDOR-CORRA volumes review, while briefly covering CAD derivatives volumes along the way. Last year’s edition of this blog is here and our prior […]

How much margin? The 2024 edition

This blog covers the 2024 edition of the “ISDA Year-End Margin Survey”, published on 14 May 2025, which covers over-the-counter (OTC) derivatives uncleared initial margin (IM) and variation margin (VM) for all asset classes, and cleared IM for interest rate derivatives (IRD) and credit derivatives (CRD) only. We combine the ISDA survey data with more […]

Q1 2025 CCP volumes and share in CRD and FXD

This blog reviews the volumes and central counterparty (CCP) market share of cleared credit derivatives (CRD) and FX derivatives (FXD) in Q1 2025. Comparing Q1 2025 with Q1 2024, we see 44 percent overall volume increases in cleared CRD – index, single-name, and swaptions. Comparing Q1 2025 with Q1 2024, we see 31 percent overall volume […]

What’s new in AUD swaps in 2025?

This blog looks at another year of AUD swaps activity, continuing from the blog with a similar title published at about the same time last year. Should you want more information on AUD swaps, the blog linked above contains links to several other blogs on the topic. AUD market total size First, we extend the […]