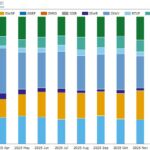

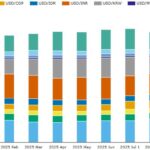

Q1 2026 shares of D2D platform core rates swaps

This blog covers D2D platform shares of core rates swaps in G6 currencies in Q1 2026. Key takeaways Read on for further analysis and explanation. All the charts and statistics in this blog were sourced from SDRView. Background We focus on the core rates swap products: cleared OIS and fixed-float IRS, of which at least […]

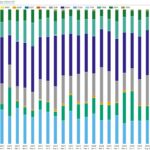

Swaption volumes by strike – Q4 2025

This post continues our quarterly strikes analysis of USD swaptions, which are typically 50 percent or more of swaptions volumes in all currencies. If you are new to swaptions, some basics are outlined at the start of the earlier Q1 blog. You may also wish to keep open on the side our recent blog on […]

2025 swaption volumes and market shares

This blog reviews 2025 full-year swaption volumes, their split between on- and off-platform, and the market shares of platform groups. We focus on the swaptions in the top four (G4) currencies using SDRView to aggregate volumes and trade count. Key takeaways For G4 swaptions in 2025 compared with 2023: Read on for the charts and […]

2025 rates ETD exchange and CCP competition

This blog looks at competition for trade volume in Q4 2025 and for the whole of 2025 between rates exchange-traded derivatives (ETD) exchanges and CCPs. Key takeaways In 2025, only EUR money-market (MM) futures, JPY MM futures, and USD MM futures show real competition now or potential for real competition in the future. Read on […]

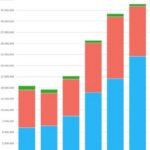

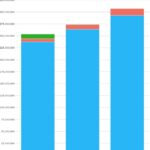

2025 cross-currency swap volumes and market shares

This blog reviews 2025 full-year cross-currency swap volumes, their split between on- and off-platform, and the market shares of platform groups. We focus on the cross-currency basis swaps in the top five currencies, using SDRView and SEFView to aggregate volumes, DV01, and trade count by month and year. Key takeaways For the top five currencies’ […]

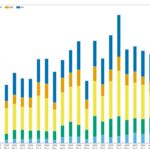

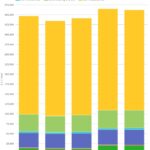

2025 CCP Volumes and Share in IRD

This blog reviews 2025 volumes and market share of interest rate OTC derivatives reported by clearinghouses (CCPs). We focus on “core swaps” including cleared IRS, OIS, and basis swaps, using CCPView to filter and aggregate daily volumes and open interest data published by CCPs. Key takeaways On core swaps in 2025: Read on for the […]

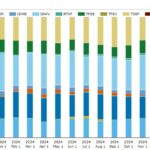

FX derivatives volumes at the end of Q4 2025

This blog covers the volumes of FX derivatives (FXD) in December 2025, following on from our prior blog on September 2025 FXD volumes. Key takeaways Read on for more analysis and further explanation. All the charts and details in this blog were sourced from CCPView and SDRView. Cleared FXD volumes First, we look at cleared FXD […]

What’s new in CCP disclosures – Q3 2025?

Clearing houses published in December their latest CPMI-IOSCO Quantitative Disclosures for Q3 2025. Key takeaways On 30 September 2025: Background Under the CPMI-IOSCO Public Quantitative Disclosures, central counterparties (CCPs) publish over 200 quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing, and more. CCPView has more than 8 years of these […]

Derivatives innovation: RTX and D2D execution automation

This blog looks at RTX Fintech & Research (RTX), a recent start-up interest rate swap SEF (Swap Execution Facility). Key takeaways: Read on for more details. All the charts, data, and statistics in this blog were sourced from SDRView. D2D SEF development After the 2008 Global Financial Crisis (GFC), the G20 consensus and national regulators exerted pressure […]

Q3 2025 rates ETD exchange and CCP competition

This blog looks at competition for trade volume in Q3 2025 between rates exchange-traded derivatives (ETD) exchanges and CCPs. Key takeaways: In Q3 2025, only two currency and product type combinations – EUR money-market (MM) futures and JPY MM futures – had material competition between CCPs. Read on for more details. Competition overview CCPView gives […]