- USD SOFR is made up of both general collateral (GC) and non-GC trades.

- Recent data suggests that there is a difference (a “basis”) between GC and non-GC repo trades.

- USD SOFR combines Dealer to Dealer and Dealer to Customer trades.

- Only a limited history of SOFR is available.

USD SOFR Components

The transactions that make up SOFR are:

- FICC cleared GC Repo transactions – so called GCF Repo. Reported by DTCC (who owns FICC).

- GC Repo trades that are not cleared at FICC. Reported by BoNY Mellon.

- FICC cleared repo transactions that aren’t versus GC but versus particular securities. Reported by DTCC.

I included a more detailed explanation of these different flavours of repo in SOFR – What You Need to Know.

Each flavour of repo has slightly different market participants – GCF Repo and FICC cleared transactions tend to mainly be interdealer.

The Real SOFR Experts

Many thanks to David Bowman over at FEDS Notes, who published the excellent research article below in July:

It is quite frankly awesome and saved me a hell of a lot of research when writing this blog. I strongly urge all of our readers to check out the original article.

My take-aways from reading this important article are:

- SOFR has three different components, all of which have varying degrees of history and transparency available.

- There is an extended history for Repo rates that has been made available by the New York Fed.

- This history is known as the Prime Dealers Survey Rate and is only for GC trades.

- This history may be important for calibrating USD LIBOR fallback spreads.

ISDA Fallbacks and SOFR

ISDA ‘IBOR fallbacks are going to be calibrated versus historic data. The parameters of calibration will be defined by a market-wide consultation:

Whatever those parameters end up being (is the consultation out yet?), we will probably need a history of SOFR prior to 2015 to calibrate USD LIBOR fallbacks. So far, our analysis has focused on the available SOFR data:

To further the history that our app can analyse, I wanted to study the technical differences between the available history of repo rates (Prime Dealer Survey Rate) and SOFR itself.

1. GCF Repo

Let’s start with the easiest component of SOFR which is GCF Repo. These are repos against general collateral that are cleared by FICC. DTCC provide data on their GCF Repo Index page, albeit I can only access history for the past year. Note that volumes, in true CCP style, are double counted.

I’m sure more data is available for paying customers!

2. Other GC Trades

For the GC trades that are not cleared at FICC, the administrator of SOFR (the New York Fed), receives all of the data from BoNY Mellon. This is called the ex-GCF Tri Party data. BoNY have a page for historical rates of their Treasury Repo Index. I couldn’t find much volume data on there unfortunately:

What I did find was that I didn’t really need this BoNY data! It seems to be replicated on the New York Fed website. The Tri-Party General Collateral Rate seems to be a replication of this data. Of course, that means that it probably isn’t available prior to 2015 (same as SOFR), but it does provide us with some recent data to analyse.

3. FICC Cleared non-GC

This seems to be the missing part of the data puzzle. I cannot find any data from DTCC that shows volumes or rates for repos that were cleared at FICC but were not against GC. Anyone?

Making Sense of the Data

Therefore, I set about reverse engineering the FICC non-GC data. It is pretty trivial – if I know the end result of SOFR, I can work out the implied rates for the missing FICC non-GC data from the known GCF Repo and ex-GCF Tri Party.

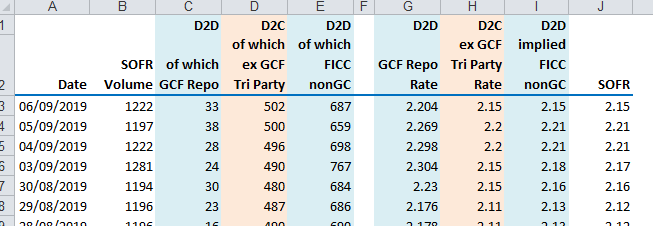

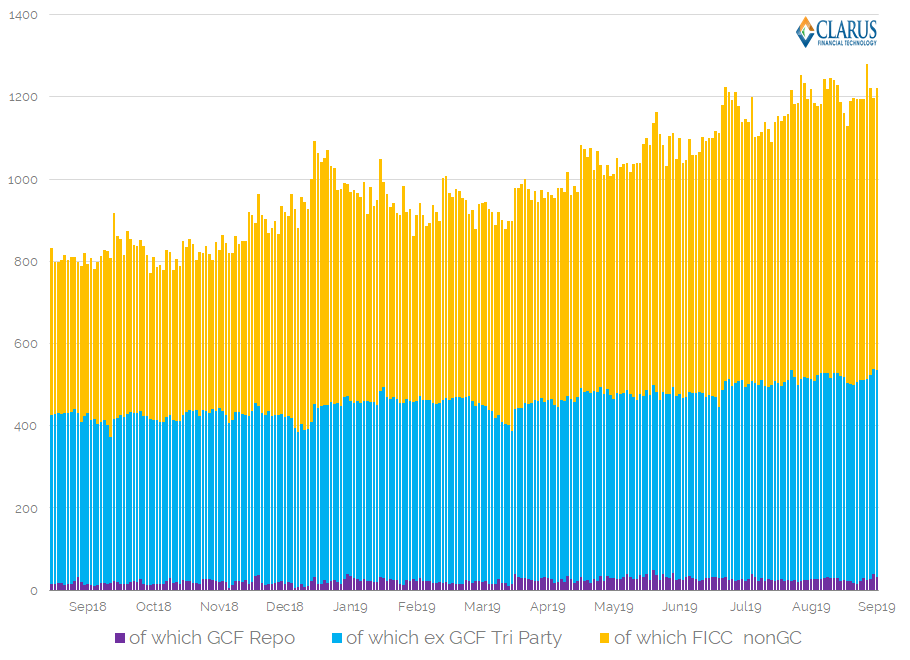

I took this data and looked at the relative importance of each constituent on a volume-weighted basis:

Showing;

- The volume of each type of Repo.

- In the data table I have colour-coded the activity types according to the FEDS notes article (interdealer = D2D).

For a repo novice like myself I was surprised to see that:

- GCF Repo, which is like a standardised cleared product to my mind, is the smallest component at less than 3%.

- FICC non-GC, which is cleared but against particular securities, is a huge component (over 50% and seemingly increasing). This is the part we do not have any historic information for.

Please note that I have implied the FICC non-GC repo rates using a volume weighted median, as opposed to the exact volume-weighted median that is used. This isn’t perfect, but for the purposes of this analysis I just wanted to see how the rates potentially behaved.

What Information Are we Missing?

So what is the point of all this? I must admit the research into the constituents of SOFR itself I have found useful – I hope our readers agree.

But the main point is to see if we can make an assessment as to whether the published history of a Prime Dealer Survey Rate for repos in GC is a good proxy for the history of SOFR prior to 2015.

From the FEDS paper:

The historical primary dealer survey rate that FRBNY has released includes both dealer-to-customer and inter-dealer tri-party trades reported by primary dealers, and so likewise tends to lie between the tri-party ex GCF rates and the GCF and ICAP rates. Because SOFR includes both GCF and bilateral trades, it has a higher proportion of interdealer trades and tends to trade close to or a bit above the survey rate

Historical Proxies for the Secured Overnight Financing Rate, FEDS Notes

The FEDS paper (which you really should read) argues that the historic proxy is reasonable. It doesn’t lie at either extreme (GCF Repo most likely represents the extreme relative to the SOFR fixing). The paper also shows that an approximated SOFR can be (accurately) modeled as a time-series using a small adjustment to the available survey rate:

\( \tag {1} SOFR = {Survey Rate} + .38*(GCF – {Survey Rate} – .05)\)However, I was still a bit uncomfortable. Why?

GC vs Non-GC

When I looked at the Prime Dealers Survey Rate (which is available all the way back to 1998) and SOFR, I wanted to understand what the technical differences were. I think:

- The Survey Rate only includes GC trades.

- SOFR includes non-GC as well.

With my background in cross currency basis trading, this structural difference was enough to spark a worry and shout “BASIS” at me. Maybe it’s paranoia?

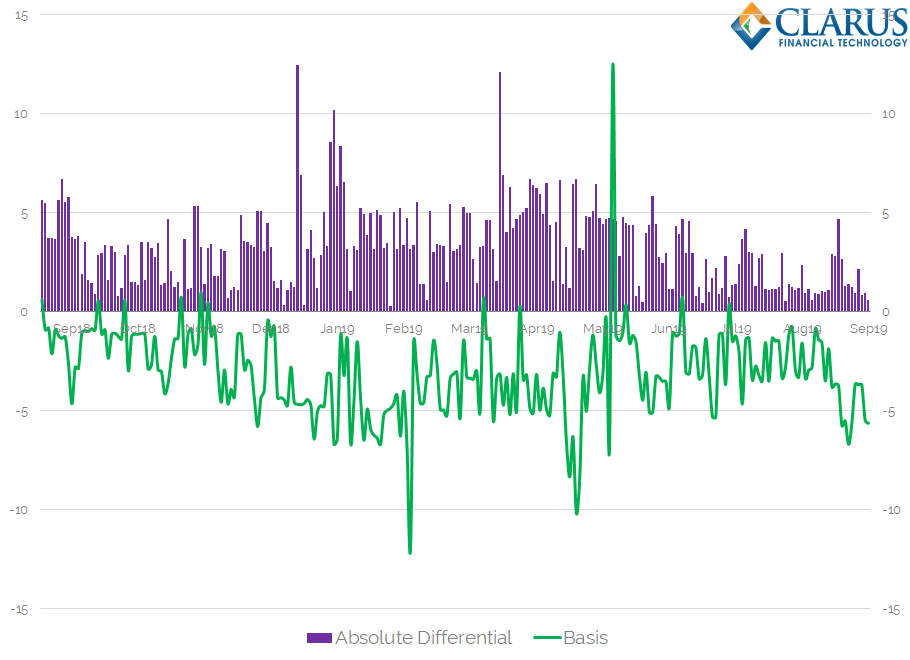

Anyway, I wanted to see what the difference has been between the GC fixing versus the implied non-GC rate since SOFR started. Is GC vs non-GC basis a thing?

Et voila:

Now I might be stating the bleeding obvious here – I am not a Repo trader. But it’s interesting to show with data that:

- There is a price difference between GC and non-GC components of the SOFR fixing.

- It has averaged 3.2 basis points as an absolute measure since 2018.

- It may be structural and I don’t think it is random. The average price is not zero.

- For someone like me who traded cross currency swaps when they always mean-reverted within +/- 1 basis point, this seems like a real basis.

Does it Matter?

The existence (or not) of this basis may not matter if it has been very small throughout even stress periods. It will take a seasoned repo-trader to confirm this – comments are open below please.

But for anyone thinking about LIBOR fallbacks, I thought it was interesting and could be worth raising for the upcoming ISDA fallback consultations.

In Summary

- SOFR is made up of GC and non-GC trades.

- SOFR has a limited history available.

- A long-term price history of GC repo is available from the New York Fed.

- This history might exhibit a price differential to SOFR if, indeed, there is a GC vs non-GC basis in repo markets.

Finally, I would just point out that the equation in the FEDS paper does allow for the existence of this basis. With an R-squared of 99.8%, it suggests that the basis is both very stable and predictable.

\( \tag {1} SOFR = {Survey Rate} + .38*(GCF – {Survey Rate} – .05)\)

Hi Chris,

Great article! I just wanted to point out that the full data (2005-2018) from the DTCC is available, and combined with the last 12 months you can get the full history to date. Available here: http://dtcc.com/data/GCF_Index_Graph.xlsx