Following on from my article on Fundamental Review of the Trading Book – What You Need to Know, I wanted to look at the pros and cons of the Internal Models Approach over the Standardised Approach.

Background

In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum Capital Requirements for Market Risk; also known as the Fundamental Review of the Trading Book (FRTB). These new standards replace parts of the Basel 2.5 reforms, which were introduced in 2009 to address the material undercapitalisation of trading book exposures during the 2007-08 financial crisis. (Document is here).

Capital and RWA

Banks are required to hold sufficient capital to absorb losses and regulations specify how to determine the minimum amount of capital. A bank with riskier assets is required to hold more capital than a bank with safer assets using the concept of Risk-Weighted Assets (RWA). This adjusts the assets of a firm for risk in order to determine a real exposure to potential losses.

These losses arise from different types of risk; Credit Risk, Market Risk and Operational Risk and consequently the Total RWA for a Bank is derived from individual RWAs for these risks. Our focus here is the Market Risk RWA (or Market Risk Capital), which is the potential loss from positions held in trading books that are subject to mark to market accounting.

Capital is both a constraint and a cost to a business. A constraint as the amount of capital determines how large a business can be and a cost as this capital has to be raised and so paid for. Consequently it is important to the success of a business that it holds the appropriate level of capital, too much and it is not as profitable as it could be, too little and it is taking undue risk in that it may be forced to raise more capital at short notice.

Internal Model or Standard Approach

The choice of Internal Models vs Standardised Model Approaches, comes down to the decision on which method gives a more appropriate level of capital for the risk that a firm is taking. Certainly under Basel II many banks much preferred the Internal Models approach as the Standard Approach did not appropriately reflect market risk of derivatives and resulted in much higher capital requirements.

With the new Minimum Capital Requirements for Market Risk, the choice between Internal Models and Standardised Approach will need to be re-evaluated. Firstly as both have been significantly improved and secondly as their are now more complexities in using IMA.

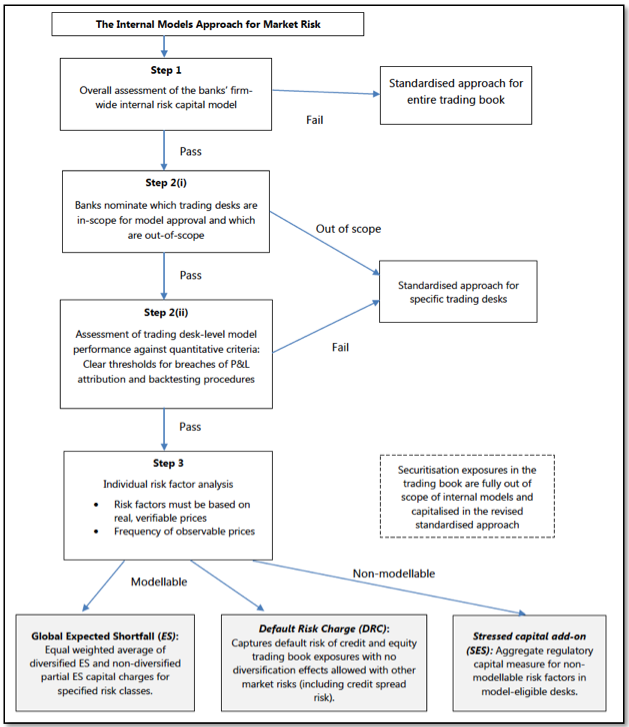

Internal Models Approach (IMA)

Lets start by looking at the Overview chart from the BCBS document.

A number of points stand out:

- Banks need to satisfy an overall assessment by their supervisor, before being allowed to use IMA

- Banks need to nominate those trading desks they want to use IMA for

- Quantitative P&L Attribution and Back-testing criteria need to be passed for these trading desks

- Securitisation exposures (e.g. CDOs) are out of scope for IMA

P&L Attribution and Back-testing

While Back-testing has always been a requirement, the need to pass a P&L Attribution criteria is new.

This requires that the “risk-theoretical” P&L for a trading desk calculated using just the risk factors used in the IMA, can explain the hypothetical daily desk P&L based on the mark-to-market value of the trading desk’s positions including all risk factors. An entirely sensible requirement.

The test applied consists of two metrics that must be calculated monthly:

- Mean unexplained daily P&L over the standard deviation of hypothetical daily P&L is -10% to +10%

- Ratio of variances of unexplained daily P&L and hypothetical daily P&L is less than 20%

Where unexplained daily P&L is defined as risk-theoretical P&L minus hypothetical P&L

If either of these metrics is not satisfied, then that constitutes a breach and if a trading desk has 4 or more breaches within the prior 12 months period then it must be capitalised under a Standardised Approach (SA).

This is not such an easy test to pass.

Particularly when you consider that most firm-wide internal models for market risk use risk sensitivities and not full-revaluation, while a desk’s P&L is calculated by valuation with a pricing model. Either a firm will need to move to full revaluation for its IMA (a computationally much more comprehensive approach) or it will need to carefully increase the granularity of the risk sensitivities in its IMA. Most likely full-revaluation will be the safer path to take.

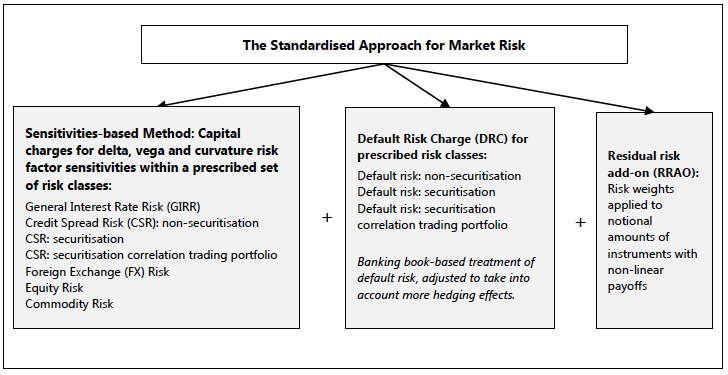

Standardised Approach (SA)

The Overview chart from the BCBS document:

SA must be calculated not only for those desks that are out-of-scope for IMA, but for all desks as a quantitative breach for an IMA desk requires a an immediate change to SA.

As the SA method is based on risk sensitivities, it is not a computationally expensive method, just that the explicitly specified sensitivities need to be calculated for each instrument and aggregated for trading desks.

While the SA is likely to lead to a materially higher charge than IMA for most trading desks, there is no requirement to pass Quantitative P&L Attribution and Back-testing criteria, making it a much easier method to implement and operate.

Internal Models vs Standardised Approach

The decision to use IMA or SA is not as straight forward as it was with Basel I or Basel II.

Each bank will need to evaluate the pros and cons for its own trading desks before deciding on one over the other. As cost-income ratios are also under management focus (targets to get to <60%), the added cost and complexity of an IMA approach needs to be considered. Particularly as the SA needs to be available for all trading desks anyway.

Most banks should perform quantitative impact studies to compare the two methods for their trading business.

Final Thoughts

The 2007-08 Financial Crises caused large losses for many firms.

This led to depletion of loss absorbing capital and the need to raise new capital.

The realisation that there was in-sufficient capital led to regulations to increase capital requirements.

Many firms were also forced to significantly reduce their RWAs to satisfy shareholders.

Capital has become a bigger constraint and a more significant cost.