As LCH SwapClear plans to start clearing Inflation Swaps I thought I would look at what the US SDR data shows for this product. While this is only part of the global market, it still provides very interesting insight into the market.

Summary

- Inflation Swaps trade in USD, EUR, GBP

- Gross Notional volume averages $2 billion a day

- An average 45 trades a day, making the standard trade size $40m

- 1Y, 2Y, 5Y, 10Y are the common maturities

- All volume is Uncleared

- On SEF is 75% in USD

- January was the highest volume month

- BGC dominates market share

Now lets look into the detail and charts (which we know are worth a hundred words or is it a thousand?)

Historial Volumes

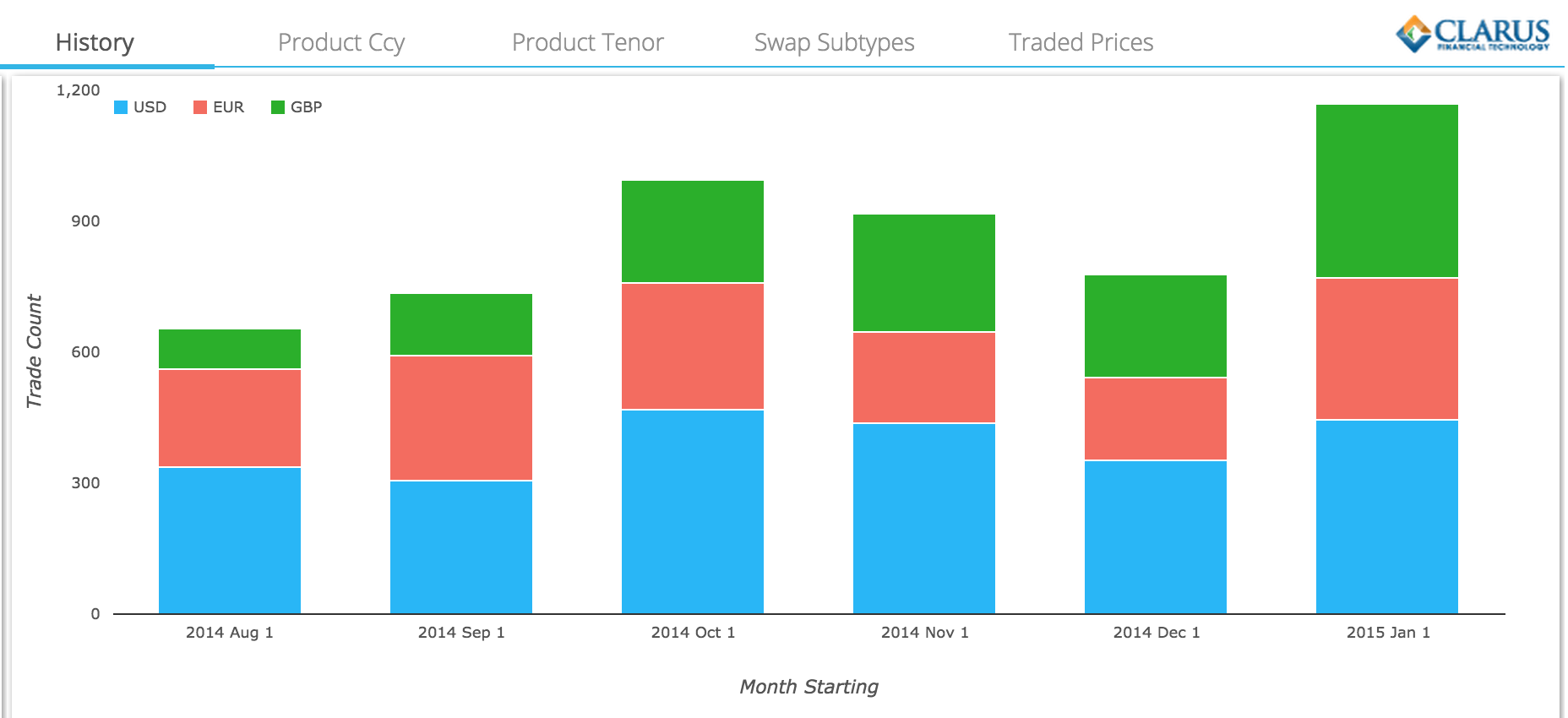

First using SDRView Res to look at USD, EUR, GBP Inflation Swap trade counts in the last 6 months.

Which shows:

- USD trades are 300 to 470 a month, or on average 20 per day

- EUR trades are 200 to 300 a month, or on average 12 per day

- GBP trades are 100 to 400 a month, or on average 12 per day

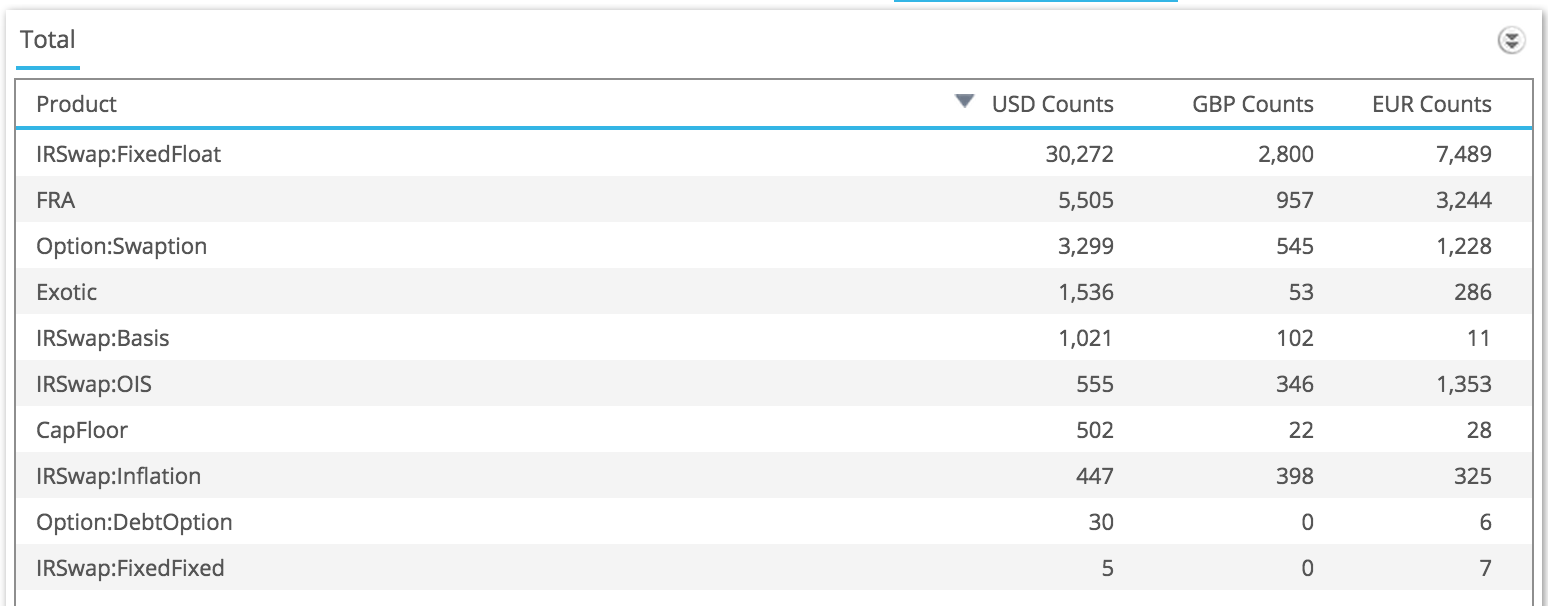

To put that into perspective we can look at January trade counts for all IRD products and see that Inflation Swaps rank fourth, fifth and eighth in GBP, EUR and USD respectively:

So while it would seem to be a small market, switching to gross notionals shows us another perspective.

Which shows:

- January has the highest volumes for each of the currencies ($20b, $17b, $16b in USD, EUR, GBP)

- USD notionals are $12b to $20b per month, on average $780 million per day

- Very few USD trades are larger than the capped notional thresholds, only 1 or 2 a month

- Implying an average trade size of $40 million

- EUR notionals are $9b to $17b per month, on average $600 million per day

- Implying an average trade size of $30 million

- Only 3 or 4 trades a month exceed the capped notional threshold

- GBP notionals are $2b to $15b per month, on average $465 million per day

- Implying an average trade size of $23 million

- In some months up to 14 trades exceed the capped notional threshold

In aggregate we can say that average daily volume is $2 billion.

Which Maturities trade?

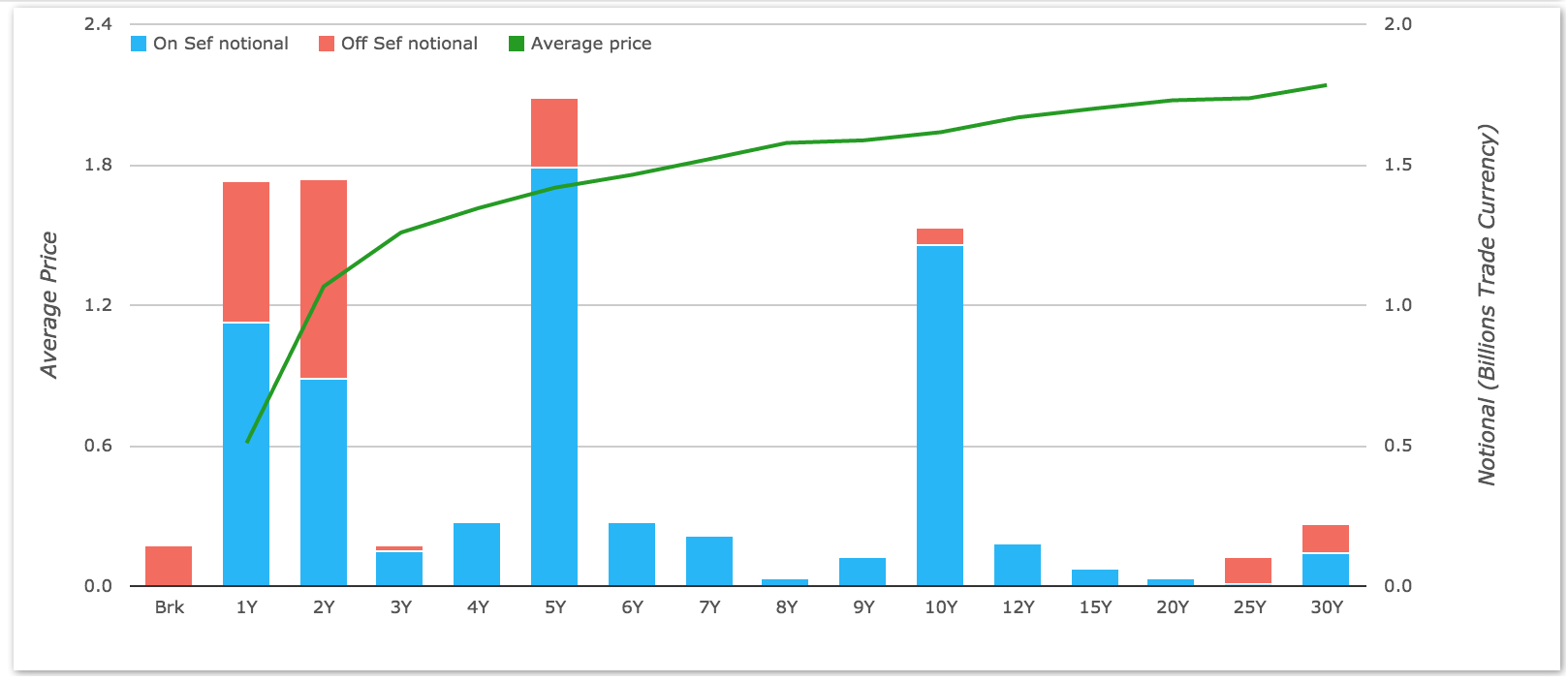

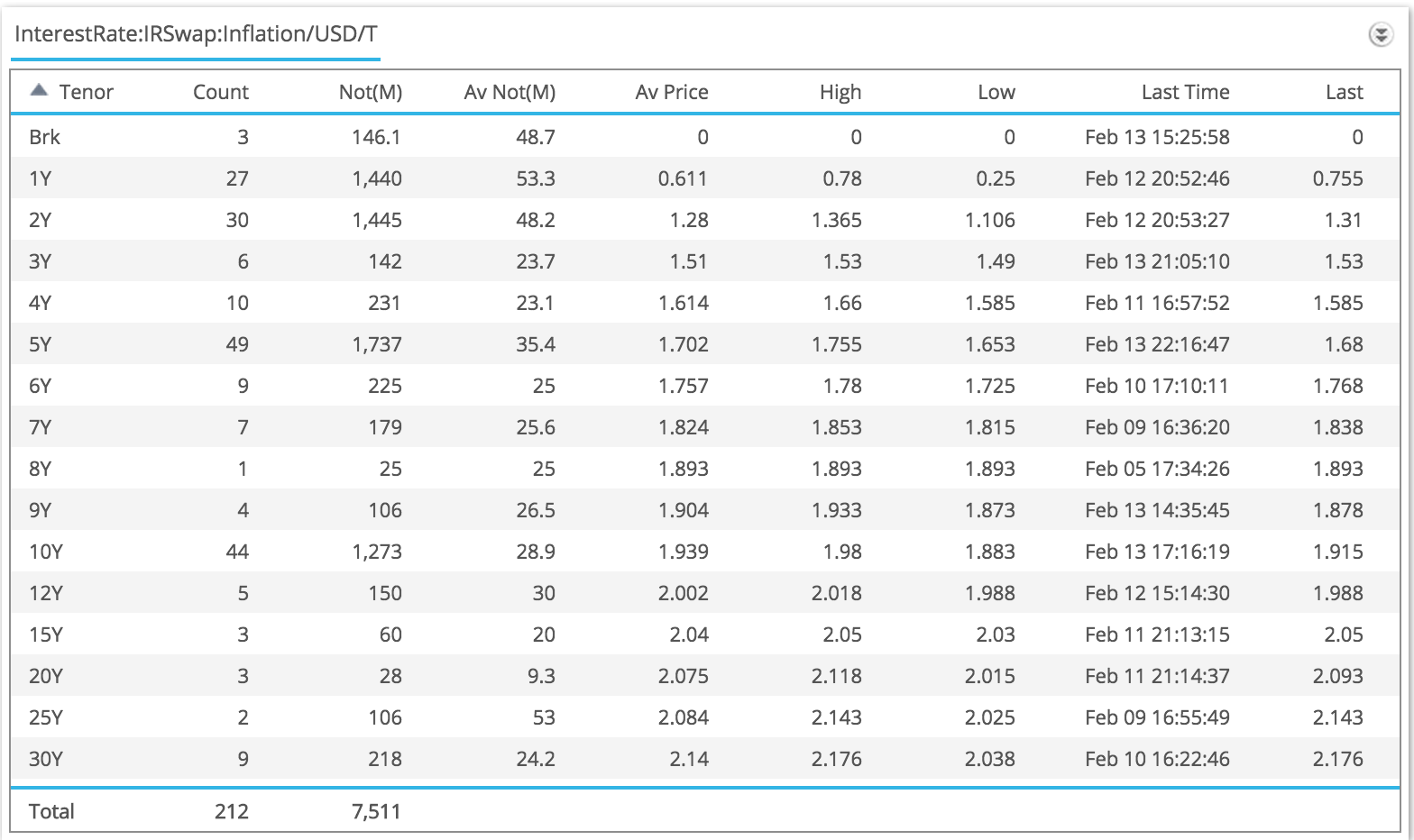

The standard Inflation Swap is a zero-coupon structure that references CPI and it is interesting to look into which maturities trade. Looking at USD Inflation Swaps in February 2015, we see that 1Y, 2Y, 5Y and 10Y are the common maturities.

And the same data in a table shows:

I let you digest all those numbers, while I stick to charts (Is a chart worth a hundred words or more?)

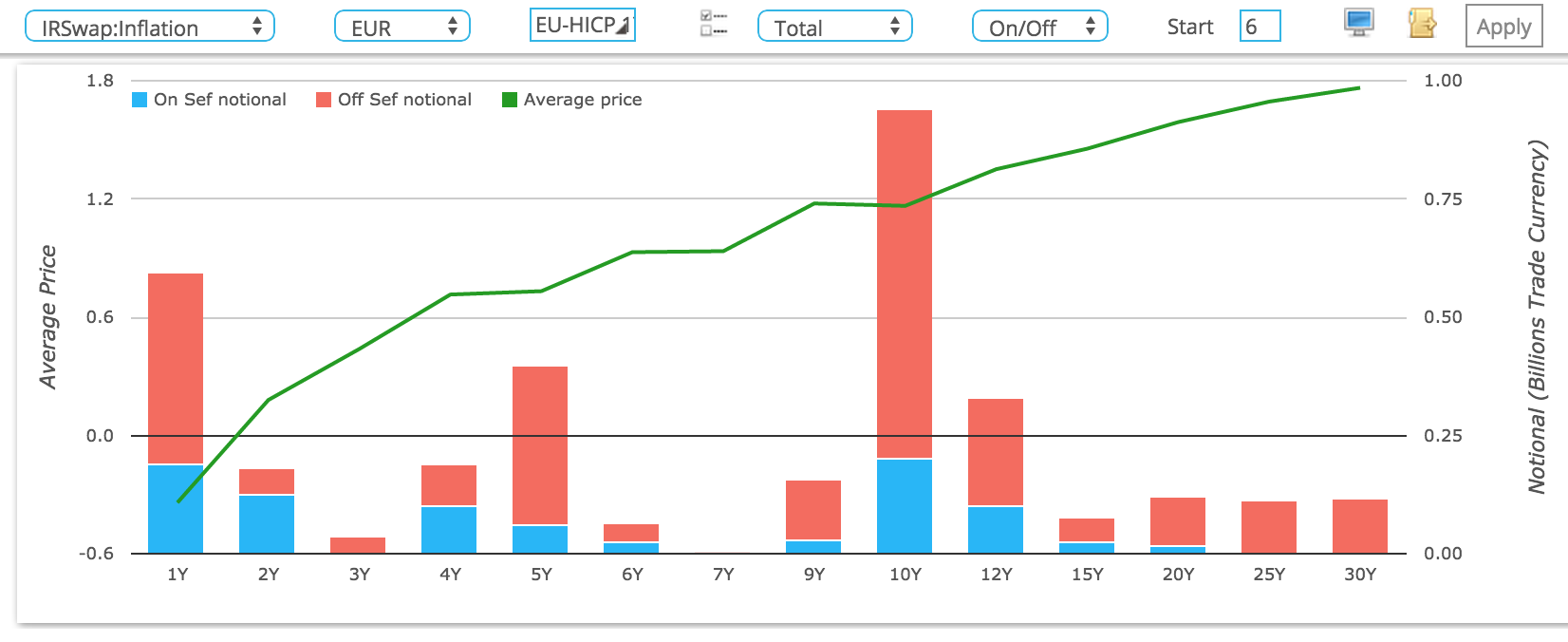

On to a chart for EUR showing that 1Y, 5Y, 10Y & 12Y as most common tenors.

On SEF vs Off SEF

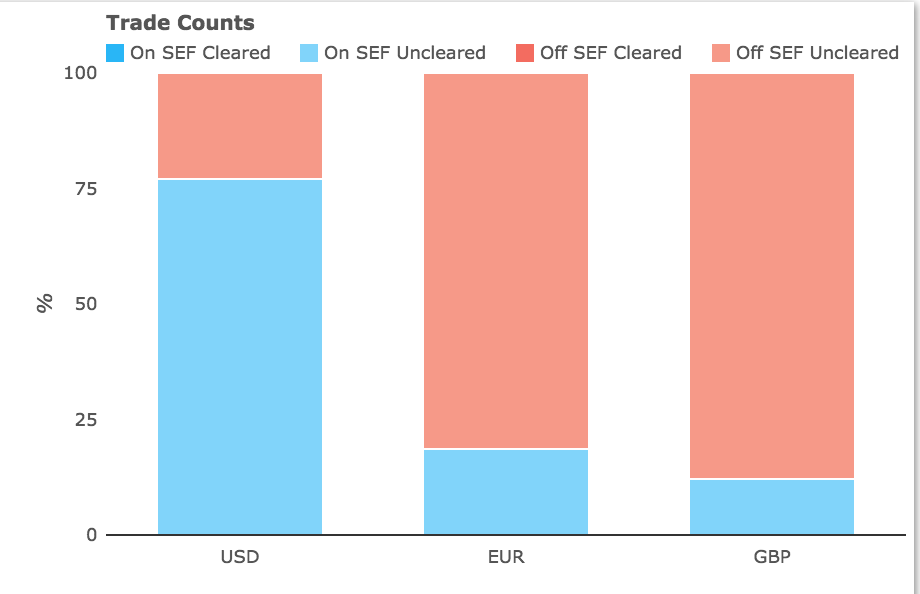

While we know all Inflations Swaps are Uncleared, it is interesting to look at On SEF vs Off SEF trade volumes in January.

Which shows that 77% of USD, 18% of EUR and 12% of GBP are traded On SEF.

Certainly for USD that is a surprisingly high percentage and highlights the convenience or cost effectiveness for market participants to trades these On SEF in the absence of a MAT mandate.

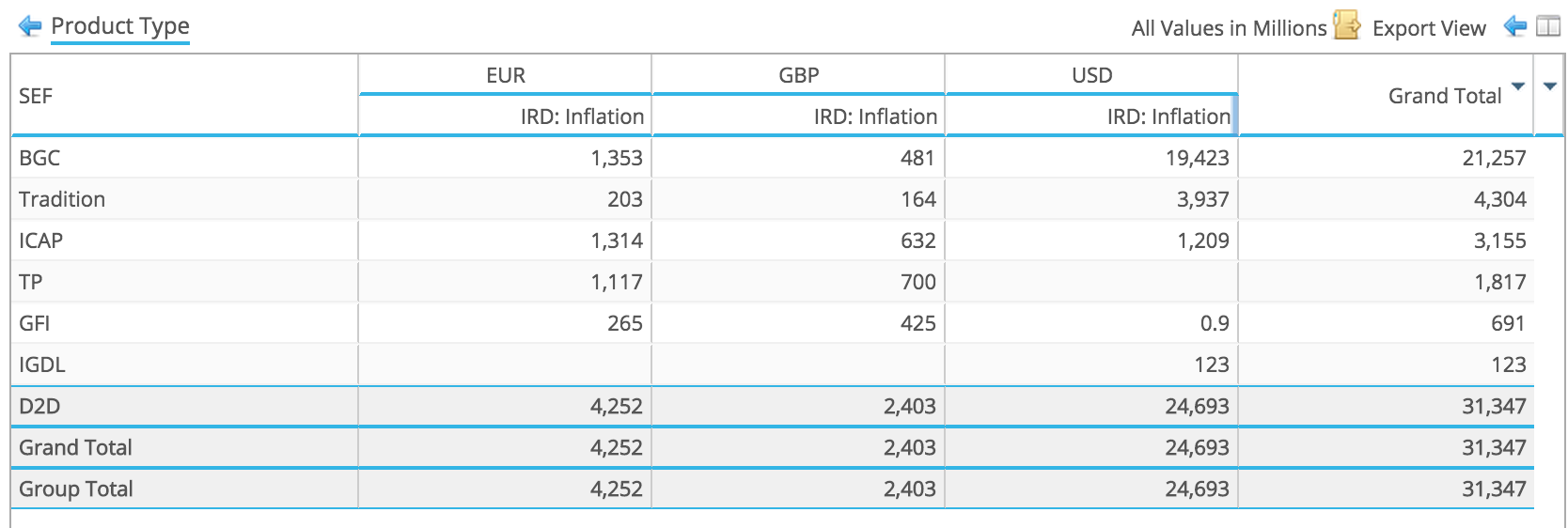

Lets now use SEFView to look at 2015 YTD volumes to see SEF market share.

Which shows that:

- BGC dominates in USD with 79% share

- Tradition is next with 16% and then ICAP with 7%

- In EUR, BGC has 32%, ICAP 31% and TP 26%

- In GBP, TP has 29%, ICAP 26%, BGC 20% and GFI 18%

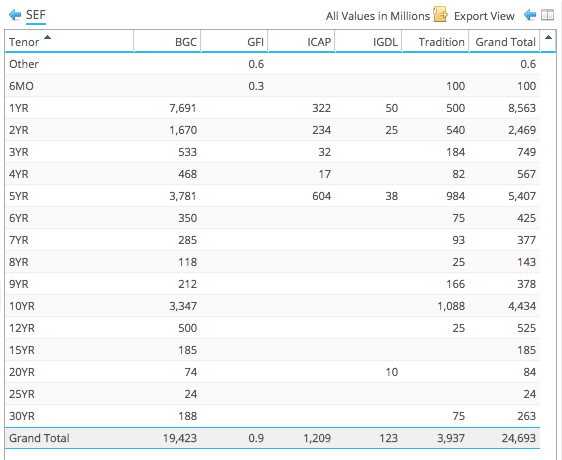

Next lets look at USD by SEF and Tenor.

Which shows that BGC has trades from 1Y out to 30Y, with 1Y, 5Y & 10Y as the largest.

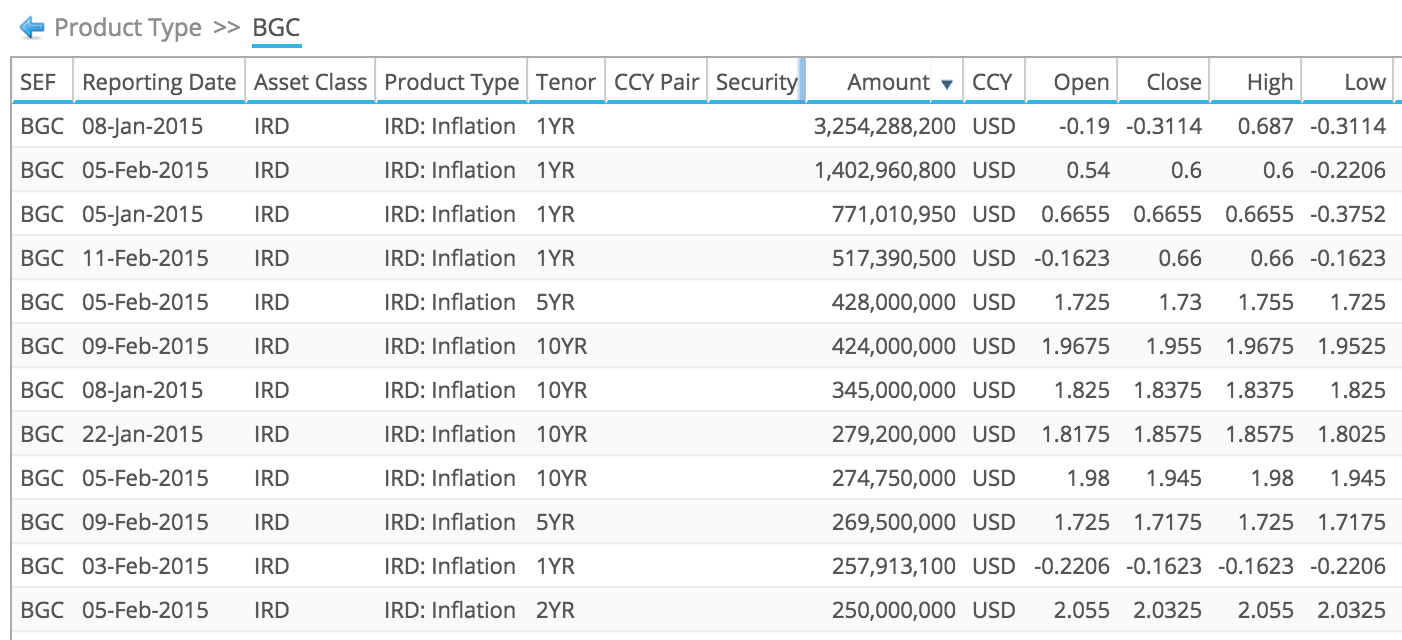

Drilling down on BGC volumes and sorting by largest amount.

We see that the:

- Highest volume was for 1Y on 8 Jan with $3.2billion

- Next highest was 1Y on 5 Feb with $1.4 billion

- Highest 5Y volume was on 5 Feb with $482 million

- Highest 10Y was on 9 Feb with $424 million

Thats about all I have time for today.

Thank you for reading this far and if you are interested in more detail, you will find it in SDRView and SEFView.

I will plan to do an update some time after the start of LCH Clearing of Inflation Swaps.