Welcome to 2015 everyone! I thought I’d start the year with some simple thoughts on Initial Margin, before later applying these to what may (or may not!) be charged when dealers quote on a compression run that we identified using the SDRView Pro API.

Initial Margin Basics

As Amir has covered in a number of articles, Initial Margin is the amount of cash and/or government securities that you must post at a Clearing House for a CCP to be comfortable that they can liquidate your position in the event of default, without a resulting catastrophic loss. Where-as in the past, uncleared derivatives resulted in un-heard-of levels of leverage, Initial Margin at a CCP effectively reduces the leverage inherent in your position. Because Initial Margin must be maintained for the life of the trade, it has to be either borrowed, or is capital that is unavailable to invest elsewhere. It therefore has an associated cost of funding and hence negatively impacts the total return on any trading position or hedge.

And what are you funding?

This cost of funding can be fairly substantial due to how the Initial Margin is calculated at the CCP. In general, you are asked to effectively pre-fund losses equivalent to the 99.xth percentile of previously observed (or simulated) market moves on your portfolio, over a five-day period.

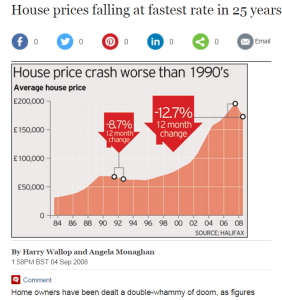

Whilst this sounds like a huge amount, we can make an analogy to the amount of leverage available in the housing market. If we take the UK as a guide, a bank will take an estimate of X number of months it will take to sell your property (e.g. 12) and combine this with previously observed market downturns in a period this long (2007-08, -15%; 1991-92, -7%). This helps to explain why banks are happy to lend at loan-to-value ratios of 70-90%, and higher LTVs are available for lower priced properties that spend less time on the market.

Whilst this sounds like a huge amount, we can make an analogy to the amount of leverage available in the housing market. If we take the UK as a guide, a bank will take an estimate of X number of months it will take to sell your property (e.g. 12) and combine this with previously observed market downturns in a period this long (2007-08, -15%; 1991-92, -7%). This helps to explain why banks are happy to lend at loan-to-value ratios of 70-90%, and higher LTVs are available for lower priced properties that spend less time on the market.

In a similar manner, a CCP wants to ensure there are sufficient margin funds in case a member defaults. They therefore kindly ask you to “deposit” the losses that your portfolio may incur in the event that they have to close your positions.

Cost of Funding – Incremental or Standalone?

The fact that a CCP considers your portfolio as a whole is the key concept here. Although swaps are not (yet) entirely fungible trading instruments, CCPs correctly recognise the economic equivalence, and hence participants can offset payers (buys) and receivers (sells) when calculating IM. IM is therefore calculated across the net risk of your whole portfolio. This tends to have opposing effects for end-users versus liquidity providers. Amir has explored this idea previously here, which I urge you to read.

There are therefore two (potentially very) different measures of IM for each trade – what I call a Standalone versus an Incremental amount. This concept is part and parcel of our Margin Optimisation tool, CHARM, and we look at an example below. But first the definitions of the terms I like to use:

Standalone Initial Margin : The IM of a swap if this were the only position in the account.

Incremental Initial Margin : The change in IM of a portfolio due to the addition of a new swap (or swaps).

Example

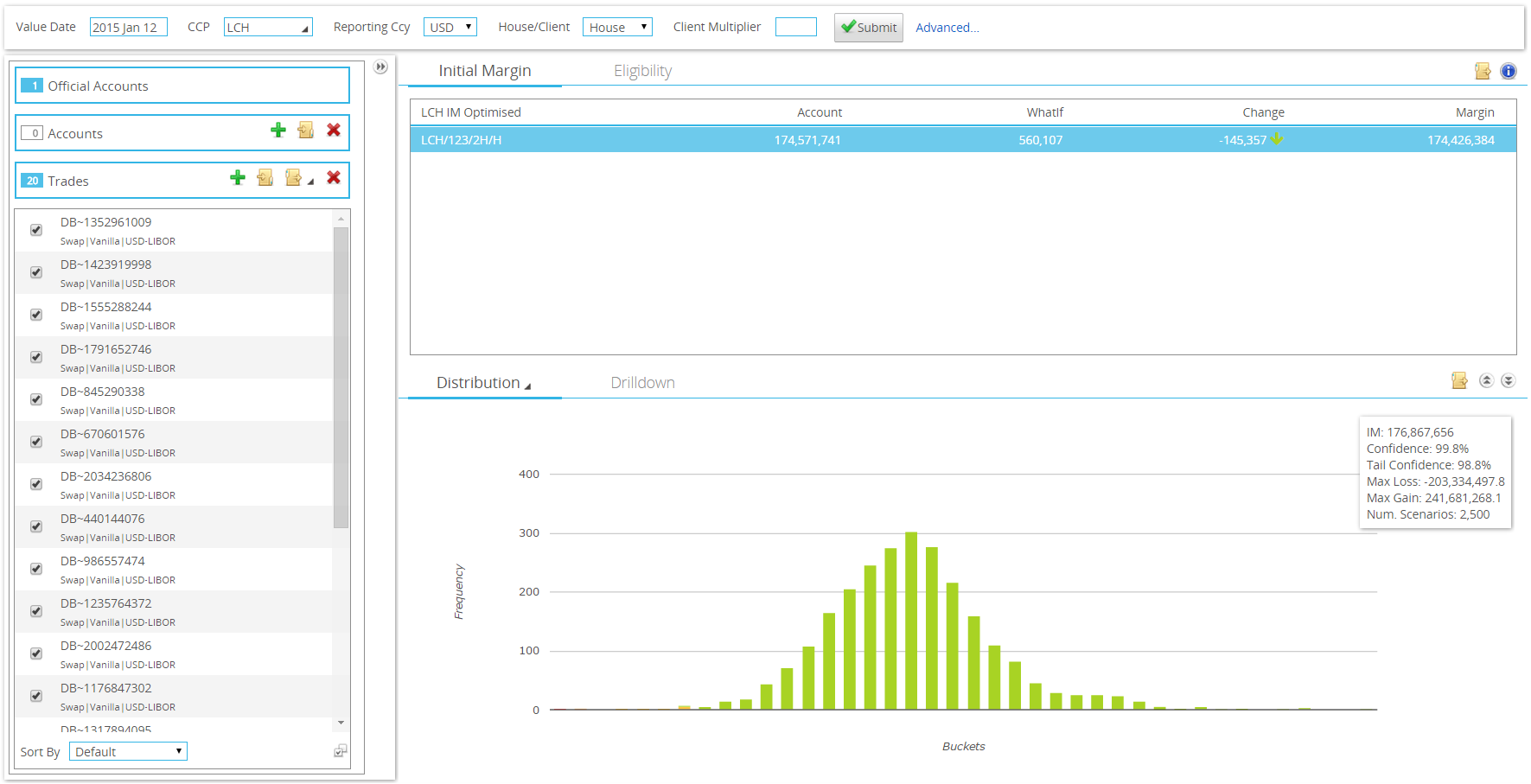

The simulations below are run against a hypothetical house account with 1,000 trades cleared at the LCH. I have input 18 swaps from a compression run in the SDR data that I have used to model a “real” pricing scenario, and added two further swaps that represent a particular funding scenario.

In CHARM, we can run the IM calculations to see the effect of these 20 new swaps on the portfolio of 1000 existing trades. On the screenshot below we see the difference in IM on a standalone versus an incremental basis:

Showing:

- “Account”: The IM requirement of the house account before adding any new swaps is $174.571m.

- “WhatIf”: The Standalone IM (i.e. the IM of the 20 swaps being analysed is $560k).

- “Change”: The Incremental IM (i.e. the IM effect of adding the 20 swaps to the house account is a reduction of $145k).

- “Margin”: The new IM requirement of all 1020 swaps would be $174.426m in the house account.

A dealer with a house account at a CCP may consider all of these IM measures when providing liquidity to the market on a single swap, or (as in this case) on a portfolio of seasoned swaps to a particular client.

Armed with these figures, we can make a couple of deductions:

- The dealer quoting on these swaps should be motivated to win the portfolio, as it reduces their (large) IM burden.

- The dealer may try to guesstimate the IM impact from their client’s point of view. In this example, the client is asking for a number of historic trades to be priced, which therefore probably represent an IM burden for a relatively delta neutral portfolio. The impact on the client’s IM is therefore likely to be closer to the standalone value (+$560k).

Initial Pricing Impact

Now that we have looked at the IM scenarios, we can calculate the impact on the price of the portfolio. The exact price will depend upon each counterparty’s cost of funds. However, we can use an estimate for the industry as a whole and use a financials CDS level for the purposes of illustration. This is approximately 110bp. Therefore:

- If the IM of $560k had to be funded for five years, the cost of these funds would be approximately $27k.

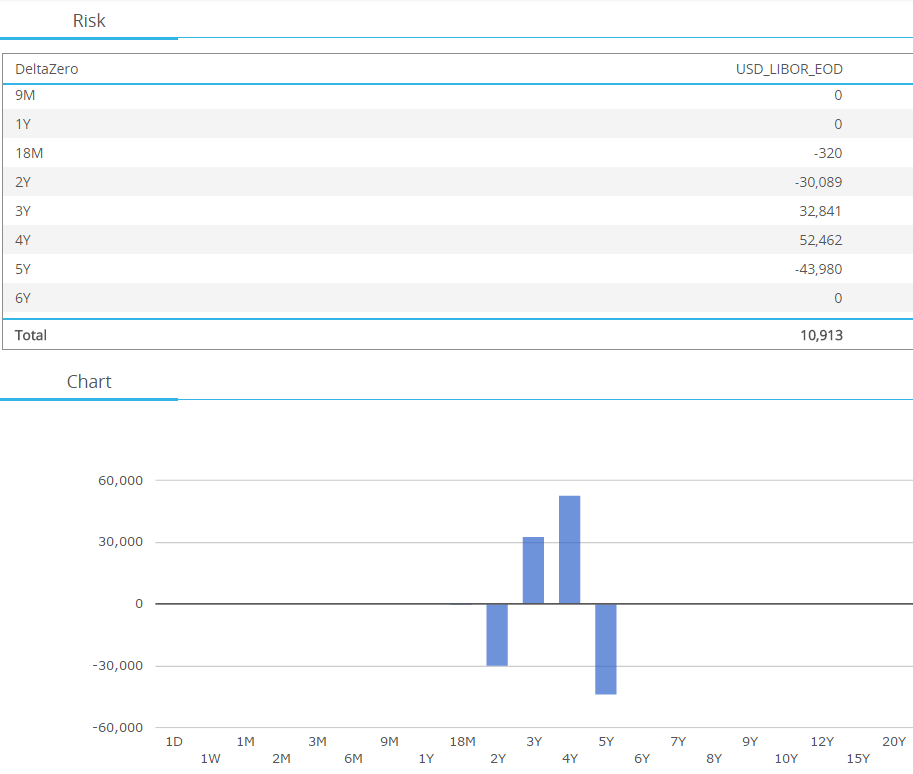

- In this case, the portfolio only has a net delta exposure of $10k! This is shown using CHARM’s Delta Zero analysis below:

- The IM funding cost, under this assumption, is therefore a highly significant 2.5bp on the outright exposure, or over 0.3bp of the “butterfly” exposure across the curve.

- Is this a “fair” charge?

Probably Not….

In the cold and harsh light of the “real World”, a Dealer will typically not pass this full charge onto their client for this portfolio. Here are a number of reasons why:

- The full IM amount does not have to be funded for the entire life of the portfolio. It will typically be assumed to converge towards zero as the portfolio matures.

- If the dealer were able to perfectly hedge this portfolio, the impact on their IM at the CCP would be zero.

- As we’ve seen here, the addition of the 20 swaps will actually reduce this dealer’s IM requirement at the CCP. That is a real benefit. This IM bias may represent a structural facet of the dealer’s underlying franchise – for example, frequently entering into uncleared pay-fixed swaps and hedging with cleared receive-fixed swaps versus the market. This is an opportunity to reduce this structural imbalance.

- It’s a competitive World! Other dealers may also see an IM reduction when quoting on this portfolio.

The Importance of Balance

The Standalone versus Incremental difference in IM is an important concept, and it helps highlight that in the new swaps world in which we live, it is increasingly important for a market-maker to keep a balanced book and actively manage the IM. This is one key aspect of how new liquidity providers can out-maneuver the incumbents. Without a natural bias to their franchise, these new market-makers can offer alternative sources of liquidity at a different incremental cost of risk.

IM – It’s not constant!

I’ll leave you with a simple fact. IM changes over time, even for a static portfolio. We therefore have to introduce a third measure of IM – specifically, a profile of how the IM will change over the life of a portfolio. CHARM is perfectly able to do so and I will explore the pricing implications of doing so in my next blog. Please subscribe to our newsletter to make sure you don’t miss it!