A couple weeks ago, we noticed some notable changes in the Mexican Peso swap market. When I began asking around, I discovered that mandatory clearing had hit Mexico. Why then write a blog about it? Well, it has become clear that I’m not the only person that hadn’t been told mandatory clearing had hit the 15th largest economy in the world.

Evidence

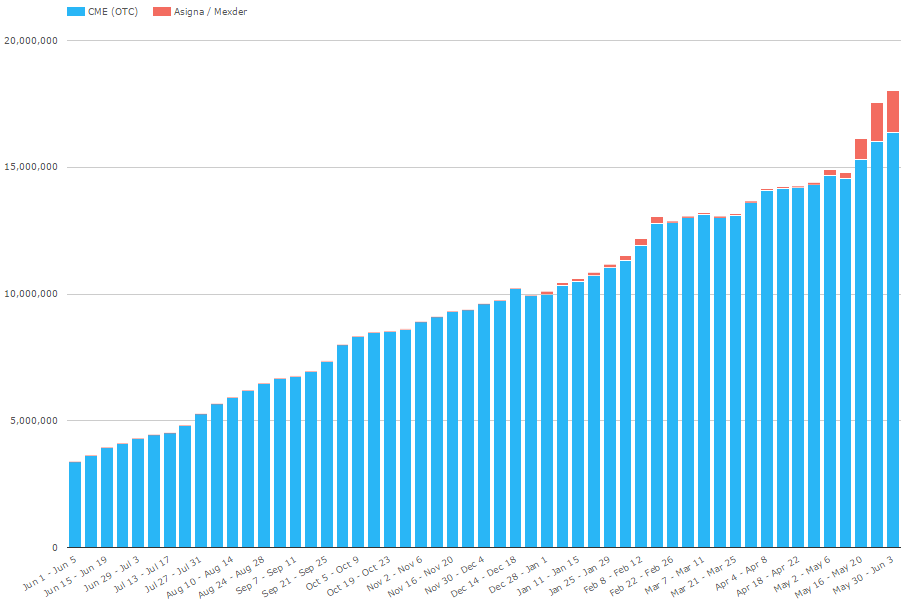

First, the evidence that piqued my interest was the growth in cleared open interest at CME and Asigna as seen in CCPView:

CME is clearly dominant in this space, having MXN open interest of over 15 trillion MXN.

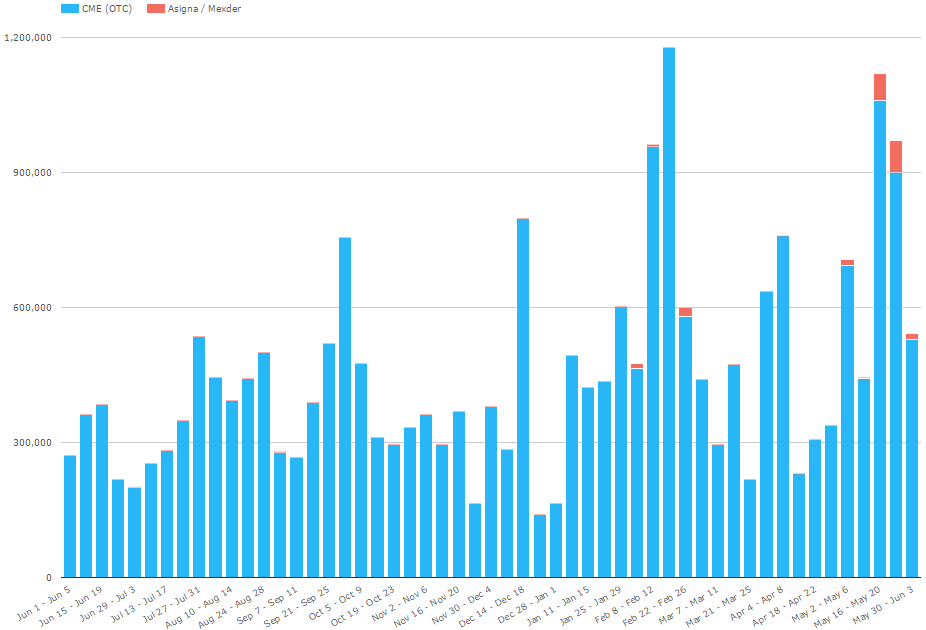

Looking at Cleared MXN IRS volume over this same period, we see some slight increases:

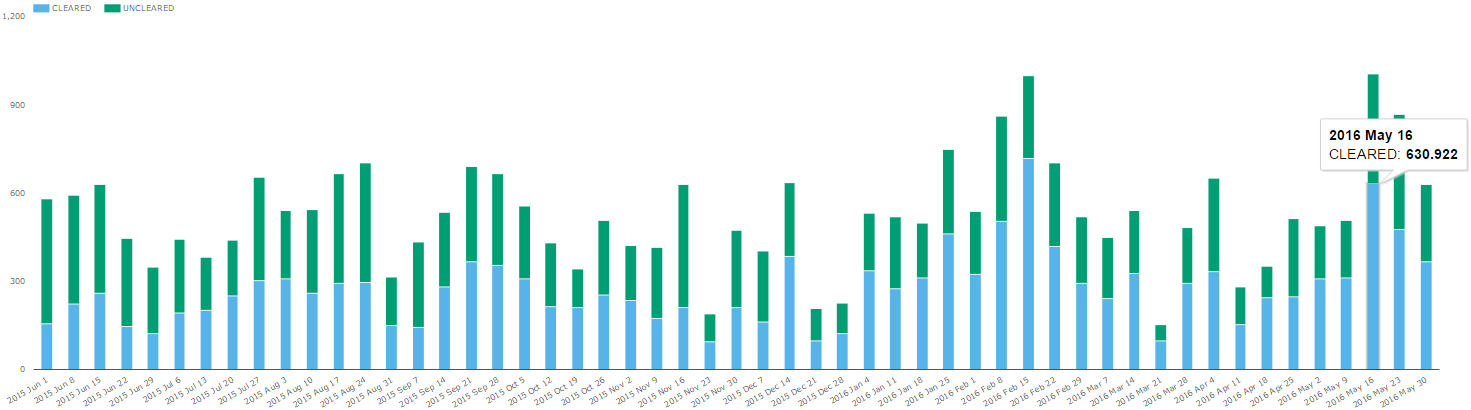

And if I go to SDRView to see US-named trade activity, while the total trading activity hasn’t seemed to change over the past year, the portion of the market that is cleared (blue) seems to have increased. Note this might not corroborate directly to CCPView given that CCPView will have uncapped, global cleared volumes, and SDRView will show US-named business, along with bilateral trading:

Finding the Rules

If you are like me, you might simply google “MXN swap mandatory clearing” to find the rules, right? Well, if you do, you will not find anything. (You will however find some Clarus blogs!)

I eventually was pointed to this document “CIRCULAR 4/2012” which is from the Banco de Mexico. Besides the fact that it is in Spanish, it’s slightly confusing as it was written initially in June 2012, then amended twice, in April 2015 and March 2016, each time apparently refining the details.

So I did what any foreigner would do, and ran it through google translate, where you get 48 pages of poorly translated mumbo-jumbo. And I also asked some friends what it says. Together, I am able to glean some rules:

- The doc seems to generally cover swaps in Credit, Interest Rates, Credit, Currencies, Commodities, Securities or Indices

- The initial mandate is for execution and clearing of MXN swaps

- It started April 1st, 2016

- Covered entities initially include:

- Mexican Banks and Mexican Broker Dealers

- Mexican Institutional Investors (if trading with a Mexican Bank as counterparty)

- Come November 16th, it will expand to include foreign entities when dealing with Mexican banks

Execution

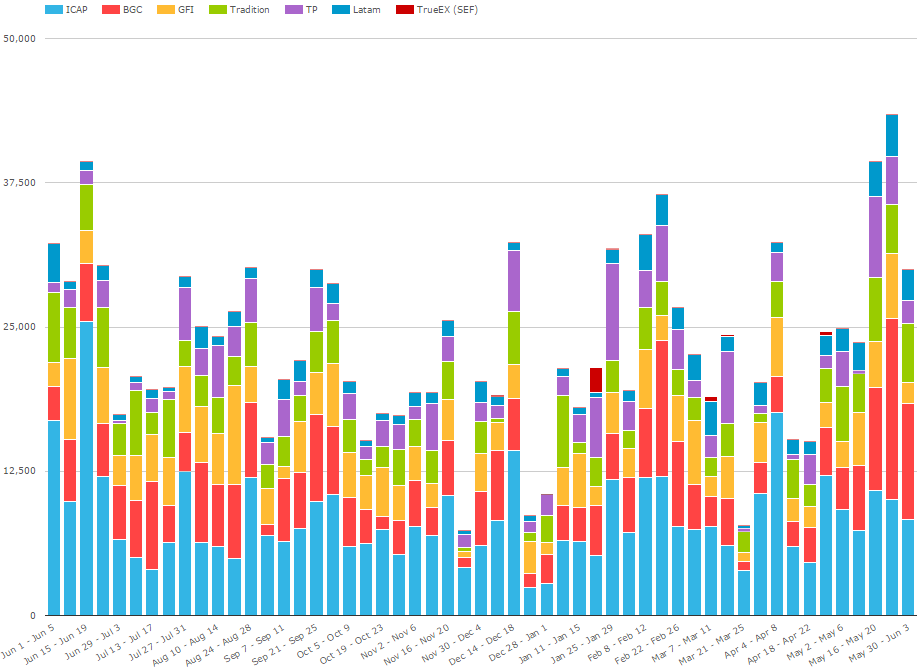

In case you didn’t catch it, I did say that there is both an execution and clearing requirement. Now, I have not had the time to research what a SEF is called in Mexico, or if they even exist. But I did query SEFView for MXN IRS to see if there is any stories to be told, over this same 52 week period:

I’m not sure I can make much out of that, but it does seem that Latam SEF, which is the SEF-version of interdealer broker Enlace, might be enjoying the benefits of any new regulations.

Summary

Legal Warning: Please, do not take any of the content of this blog as legal advice. If you are trading Mexican swaps in Mexico, I urge you to do some more homework. And if you are a salesperson at an FCM or SEF, I urge you to get on a plane to Mexico.

There seems to be some new rules in effect in Mexico, and more to come. We’ll be keeping an eye on it.

Update

I’ve had the pleasure of speaking with an MXN market structure expert, who has clarified:

- The Clearing mandate is as I mention above in the blog

- The Execution mandate requires trades done by banks/brokers to be executed and reported to registered Mexican IDBs. Block trades are allowed to be arranged away, but do need to be reported after the fact. There is a SEF-like framework in the rules, but nobody has registered for that.

- Trade repository rules are considered in the law, but existing legislation in Mexico already covers trade reporting of everything (swaps, securities, etc) to the central bank. There is no SDR requirement, nor any public access to the existing data at the moment.