NEX Regulatory Reporting operates a MiFID II APA and it is great that their public website now supports a Market Identifier Code (MIC) level search for post-trade data, which is then easily exportable into a csv file.

Brilliant. Lets take a look at the data available.

NEX APA

The public website is here and selecting Trades shows that MIC is a criteria in the search.

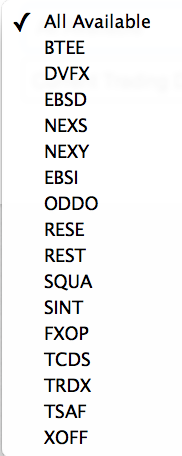

The list of available MICs is:

Sixteen MICS, of which the standout ones are; Brokertec, EBS, NEX, Reset and Tradition.

Tradition has three venues:

- TRDX, an MTF

- TCDS, an OTF

- TSAF, an OTF, registered in France

Lets look at some of the data published by two of these.

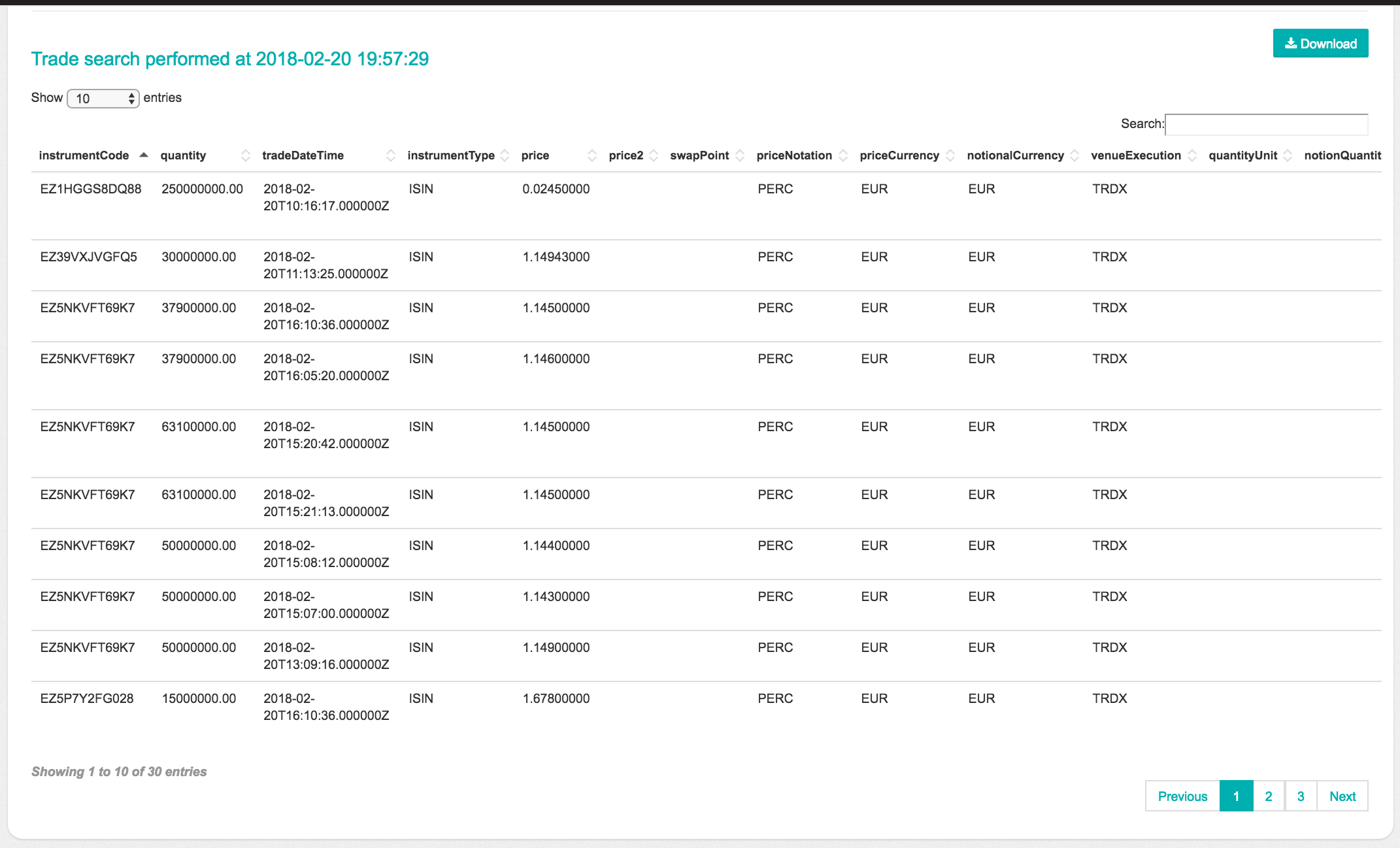

TRDX

Selecting TRDX and Current Trading day (on Tuesday 20th Feb 2018 at 19:57):

We see 30 entries each with an ISIN starting with “EZ” and the quantity, trade time, price and currency.

The required fields for MiFID RTS2.

Unfortunately like everyone looking at this data and wanting to know what these financial instruments are, I am flummoxed. (See the ISIN Debacle for details).

Even if I had a photographic memory and I remembered yesterdays trade data from this venue, the ISINs would all be different today and I would be none the wiser! Of course based on my prior knowledge of price levels, I could assume that EZ5NKVFT69K7 is EUR IRS 10Y as the trade prices are around 1.1% and there are many of these trades in the list.

But guess-work is not generally how we want to operate.

Oh for a descriptive short name of the instrument! Why ever did ESMA not require that to be published? (answers on a post-card please).

So like the tens or hundreds of others, I now have to decipher these ISINs to make sense of this data and worse I have to decipher them again every single day. Comment ennuyeux et intuile.

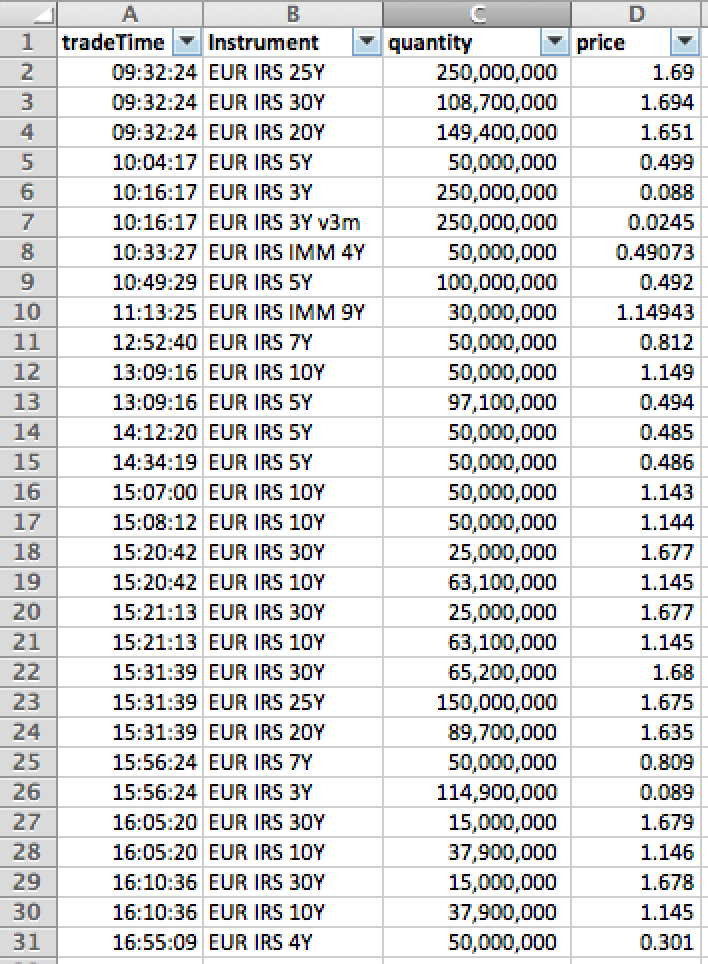

EUR IRS on TRDX

Using either the ESMA FIRDS data or DSB-ANA queries, I can convert the ISIN to a descriptive short name. Or more specifically I can glean more information on the ISIN, such as maturity date and reference index to use my knowledge to come up with a simple descriptive short name. An exercise that anyone wanting to use the public data will have to repeat.

This shows the following trades:

- 30 trades, summing up to €2.4 billion, a quiet trading day post US holiday on 19th Feb

- Actually it is more correct to call these trade legs, as many are package trades.

- The first three rows have the same time stamp

- And represent a Butterfly 20Y/25Y/30Y in €250m at 3.5bps (see definitions)

- At 10:04:17, we see a 5Y outright in €50m at 0.499%

- At 10:16:17, what looks like a 3Y switching between Euribor 6M and 3M

- At 13:09:16, we see a Spread 5Y/10Y in €50m at 65.5 bps

- In-fact the most common tenor 10Y, only has two outright trades

- While it is included in five Spread packages

- With 10Y/30Y trading four times

Interesting insights into the trading data, which require some market knowledge to piece together.

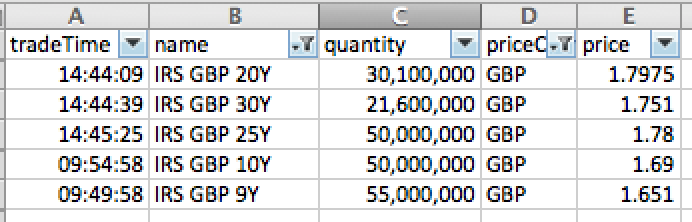

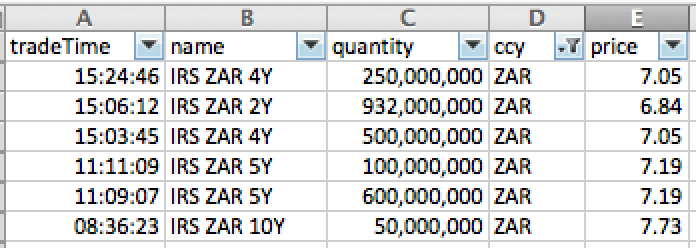

TCDS

The Tradition OTF has trades in IR Swaps, FX Forwards, Bonds, Commodities (Elec and Emissions) and Equity Derivatives. Looking at some of the IR Swaps, we can produce tables for GBP and ZAR.

Other Venues

There are a lot of other Venues with a lot more data, which I would like to look at.

NDFs on NEXS, FX on EBS, Bonds on BTEE, FRAs on RESE, ….

But those are tasks for another day.

If you cannot wait, please try yourself at the NEX APA.

NEX have made it is super easy to use.

I hope other APAs and Venues will follow.

The only tricky part is then the ISIN to instrument short name transformation.

But that requires ESMA and National Regulators to consider the rules.