On Sep 11, we went public with SDRFix and started publishing this daily on our website at SDRFix Data.

In this article I am going to summarise our progress, lessons learned and our plans going forward.

Press Coverage

To start with the announcement generated excellent press coverage with Risk, Bloomberg, FIA Smartbrief & Euromoney all picking up the story, see Clarus in the News for some of these.

The majority of these picked up the key message of SDRFix being the first index based on data reported to a Swaps Data Repository and contrasted this with the regulatory probes into ISDAFix.

Resulting from this we saw a high number of page views for SDRFix and many requests for more information.

So a great start, better than we had hoped for.

In Practice

But what have we been doing since the announcement.

Well most importantly getting used to the discipline of making sure the index is calculated and then published daily at 11:35 EST.

And doing this in a controlled, repeatable and transparent procedure.

Including following a four-eyes principle with a separate sign-off for the calculation process outcome from the publishing process.

As importantly we have had a chance to observe how the SDRFIX construction methodology performs in practice.

Ex-post and Ex-ante

When designing the construction methodology we perform ex-post backtesting to design and tune the methodology.

The true test only comes ex-ante when you are faced with out-of-sample data.

Will the methodology prove robust enough and hold up to new real-word data?

Well early days, but so far the results are encouraging.

Our Time window of 4am to 11am EST, Index Computation and Hi-Lo Trade Exclusion rules have all worked well.

Contingency detail

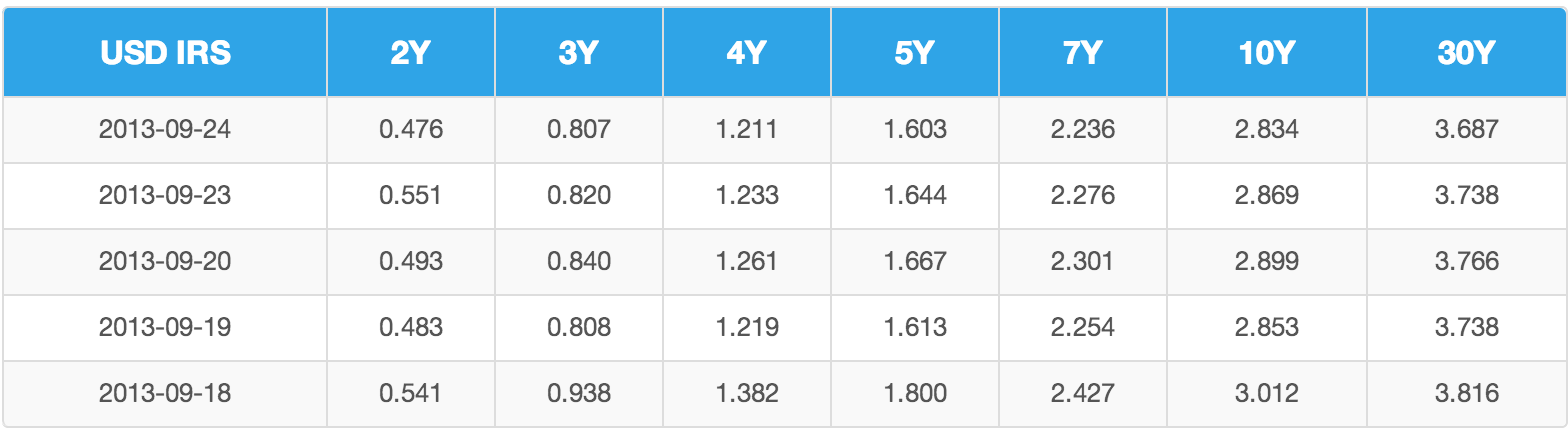

For the first time, on Sep 23rd, we exercised the Contingency plan in our methodology document. So at 11:30am EST there were no reported trades for USD IRS 2Y and EUR IRS 3Y within the required time-slot.

We were always aware that trades can be reported much later the the execution time, either for legitimate reasons (so block trade rule) or for operational failures (not booked in a firms systems till much later) or indeed system failures (reporting firms, SDR, us).

In-fact this is the reason we do not publish at 11:00 am EST, the 30 mins gives us a sufficient time window to pick up block trades that are reported with a 15 minute or 30 minute delay.

Given that we had no trades reports for USD IRS 2Y and EIR IRS 3Y, we went with the contingency plan of reporting the prior day fixing.

However checking on Sep 24, we can now see that there have been trades reported with execution times prior to Sep 23 11:00 am EST.

In-fact for USD IRS 2Y, there are 6 trades with gross notional of $1.7b, with reported times ranging from 11:50am EST to 4:00pm EST, so between 50 mins and 5 hours after the execution time.

For EUR IRS 3Y, there are 11 trades with a gross notional of €1.4b.

So we intend to revise our methodology as follows “if yesterday we had to fall-back to a prior day fixing as there were no reported trades, but today we see that trades have been subsequently reported, then today we will revise and re-publish this fixing using the newly reported trades.”

Applying this for USD IRS 2Y we will revise 0.483 to 0.551 and for EUR IRS 3Y revise 0.821 to 0.819.

Enough of the detail.

What else have we done?

- We have a new URL – sdrfix.com – much easier to remember.

- We added GBP IRS 5Y, 10Y, 30Y.

- Cap Size increases on Sep 20 by DTCC, means more weight is given to large trades.

What do we plan to do?

- Enhance the published data table, to allow drill-down to the supporting calculations and trades.

- More Currencies in IRS.

- More fixings per day where trade volume is sufficient e.g. USD IRS at 4pm EST.

- More Products in Rates.

- Many more ideas on the drawing board.

That is it for the progress report.

Please continue to share your comments and feedback using [email protected]