SOFR has been topical for over a year as markets become more used to the near-new USD Risk Free Rate (RFR). The ARRC identified SOFR as the preferred replacement for USD Libor in 2017 and has stated:

‘The ARRC has identified the Secured Overnight Financing Rate (SOFR) as the rate that represents best practice for use in certain new USD derivatives and other financial contracts. To support the transition to SOFR, the ARRC developed the Paced Transition Plan, with specific steps and timelines designed to encourage adoption of SOFR. In order to develop sufficient liquidity, the ARRC is focused on supporting the launch and usage of SOFR-based financial products in the market and creating a forward-looking term rate based on SOFR.’

My blog on 10th September looked at the trading so far this year in derivatives and compares the SOFR with the EFFR (Effective Fed Funds Rate) trading volumes. Swaps and Futures on EFFR arefar more liquid than SOFR at the time or writing but there is a preference to further develop SOFR trading as soon as possible.

On Sep 19th we covered SOFR Fixed at 5.25% What Happened to the Volumes? SOFR had been settling at around 2.10 to 2.20% for a few weeks but jumped to 5.25% on 17th September. Since then SOFR has set at 2.55%, 1.95% and 1.86% on 18th, 19th and 20th September respectively. The FED Target range was 2.00 – 2.25% (until 19th September and changed to 1.75 – 2.00% explaining the drop in SOFR from that date) but SOFR set 3% above the Target.

Meanwhile, EFFR was set at 2.30% on 17th September: so no real change.

This blog looks at the basis between EFFR and SOFR as well as their relationship with the Target Range. I will also review the 1, 3 and 6 month compounded rates from EFFR and SOFR over a 5 year history.

Some basics

In our blog Four Things to Understand about SOFR we explained the components of SOFR and how they are compiled and used in the calculation. SOFR uses a wide range of trades based on secured (repo) and typically shows around $1,150 billion daily volume.

EFFR is calculated from a much narrower base of trades and counterparties. The typical volume each day is in the range $50 to 70 billion which significantly smaller than SOFR.

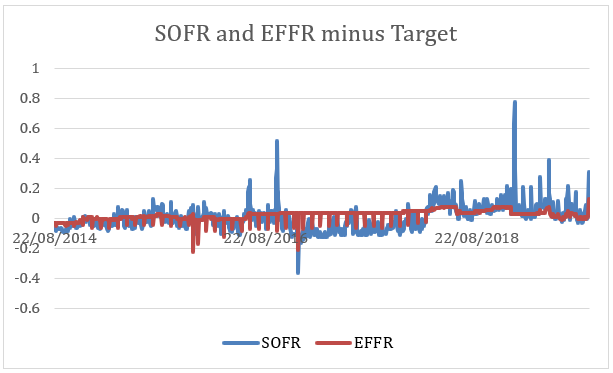

EFFR typically tracks the FED Target Rate/Range with very occasional deviations. SOFR, however, shows some significant differences to the FED Target as shown below. The chart shows the differences of SOFR and EFFR to the mid of the FED target for the past 5 years up to 16th September (one day before the recent spike).

Quarter and year ends can have funding challenges for market participants which shows in the occasional spike in SOFR rates. These are reasonably expected by markets and could be considered a feature of SOFR.

Interestingly, EFFR dips occasionally but shows few spikes.

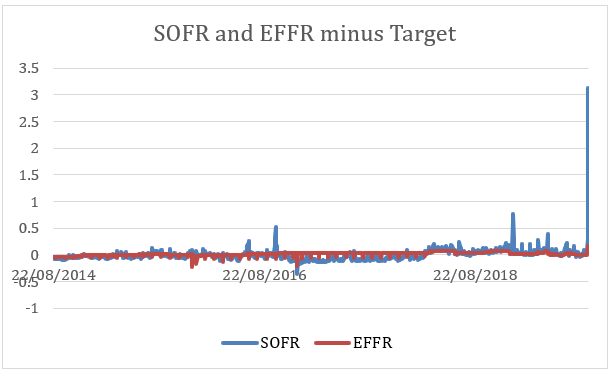

But what happens when I add the 17th September to the series? This is the chart below which shows the size and extent of the spike in SOFR on 17th in relation to the past 5 years.

The recent SOFR rate spike is certainly much more significant when compared with the past 5 years of data! Note the scale on the left compared with the earlier chart.

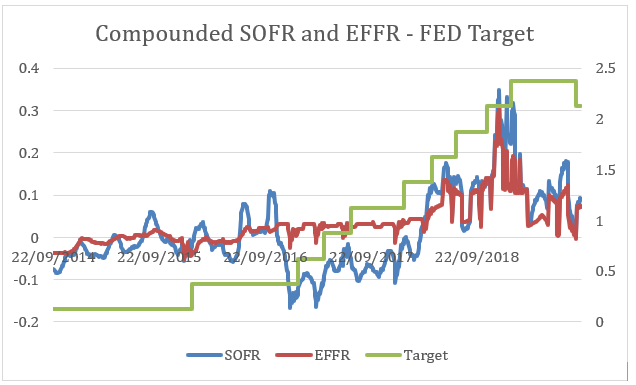

Compounded SOFR and EFFR Rates

Since the 17th September, the ARRC FAQ commented (in point 16) on the impact of the volatility when SOFR is compounded (or averaged) over a month or longer. The impacts will clearly be less when combined with other days where SOFR is closer to the FED Target.

This can be shown in the following chart showing the 1 month compounded SOFR and EFFR compared with the FED Target mid.

As expected, the volatility is less than that shown on a daily chart and EFFR tracks the Target somewhat closer than SOFR.

Compounded SOFR and EFFR

The EFFR OIS market is quite liquid with high volumes traded out to 2 years as I described previously in a blog. SOFR trading is less developed at this time and will need to increase volumes in 2020 to be an active market.

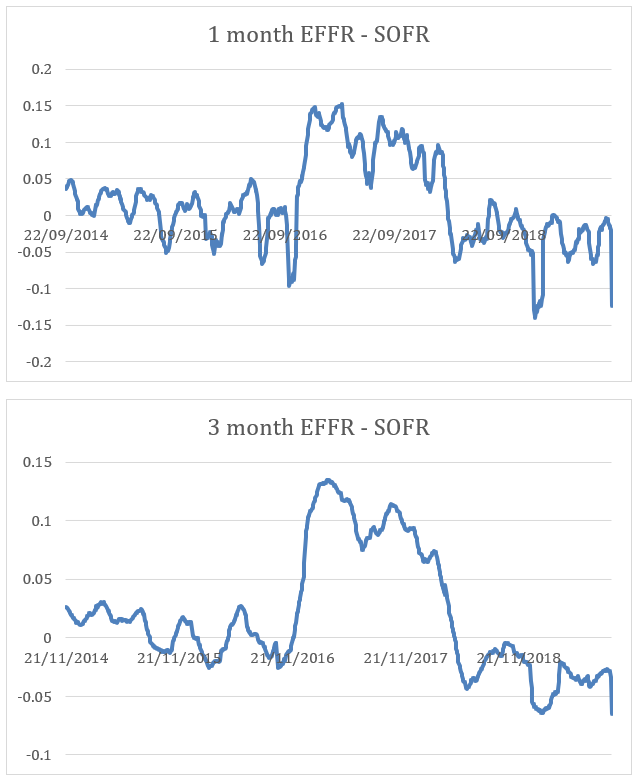

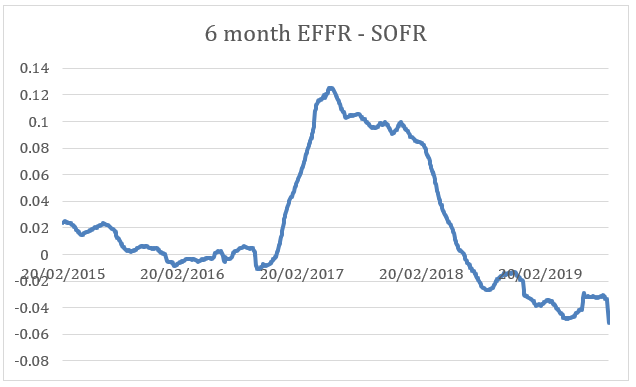

I have calculated the compounded SOFR and EFFR rates for 1, 3 and 6 month tenors each day for the past 5 years to compare the outcomes.

If the SOFR and EFFR generally move together and any spikes are averaged out over the tenors then the charts should show a reasonably constant value for the difference between them.

The following charts show compounded EFFR minus compounded SOFR for the 1, 3 and 6 month tenors. The impact of the recent SOFR spike can be seen on the far right of each chart.

As expected, the 1 month chart shows some volatility in this spread compared with the 3 and 6 month charts: the ‘averaging’ effect is smaller for the shorter tenor and SOFR spikes have more impact for 1 month compounding.

Also there is the long period of time where the spread is positive between early 2017 and mid 2018. This corresponds to a period of FED tightening (rising Target in the first chart) but it disappears in late 2018 while the Target rate is still rising.

The spread is not really consistent and can be positive or negative. The compounded outcomes for SOFR and EFFR are not the same.

Summary

The recent SOFR spike has created much discussion in markets as to the impacts and any lasting implications.

SOFR is more volatile than EFFR and could be reasonably expected to be based on the number and diversity of the trades and counterparties included in the calculation.

This volatility can be ‘averaged’ out if you view the compounded SOFR over 1 month or longer. But there is still an impact especially if the spike is not offset by lower rates on surrounding days.

The volatility of the compounded rate is more pronounced in 1 month tenors as could be expected.

The basis between EFFR and SOFR is not constant even allowing for SOFR spikes and dips. In some cases this basis has been positive for extended periods and negative for others.

Although SOFR and EFFR follow the FED Target rate quite closely, they are not always aligned in a consistent way: the basis does change quite significantly.

The ARRC is very clear in their support for SOFR as a replacement for Libor, but participants need to be aware of the features of SOFR and how it differs from EFFR.

Market participants should be aware of these differences when comparing EFFR and SOFR markets especially as SOFR develops as a benchmark.