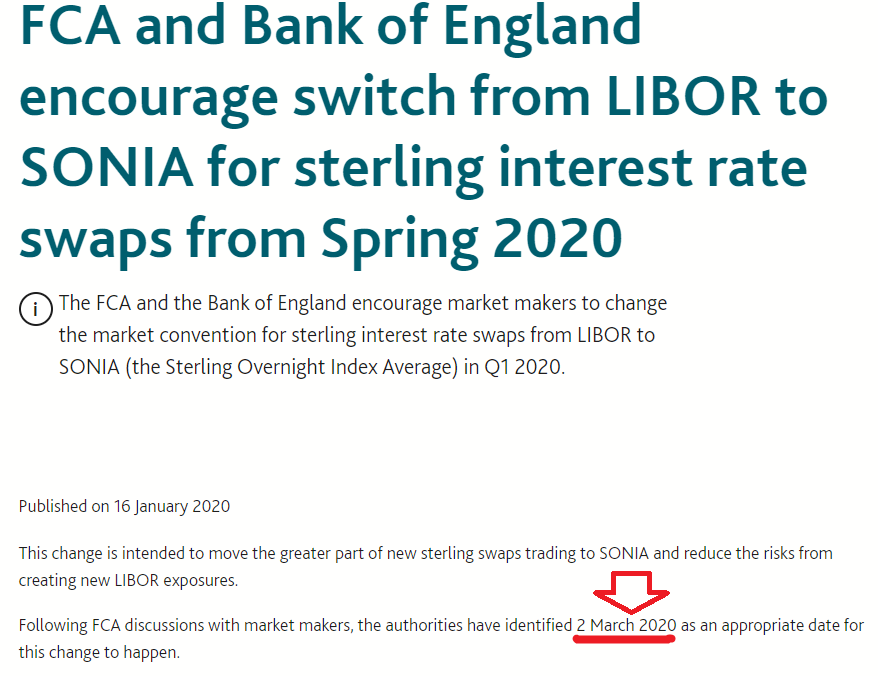

Today has been circled in the calendar for a while now. Monday 2nd March is intended to see a change in GBP swap markets. From now on, the market convention should be to trade SONIA swaps instead of LIBOR. We covered the original announcement in this blog.

19:24 London

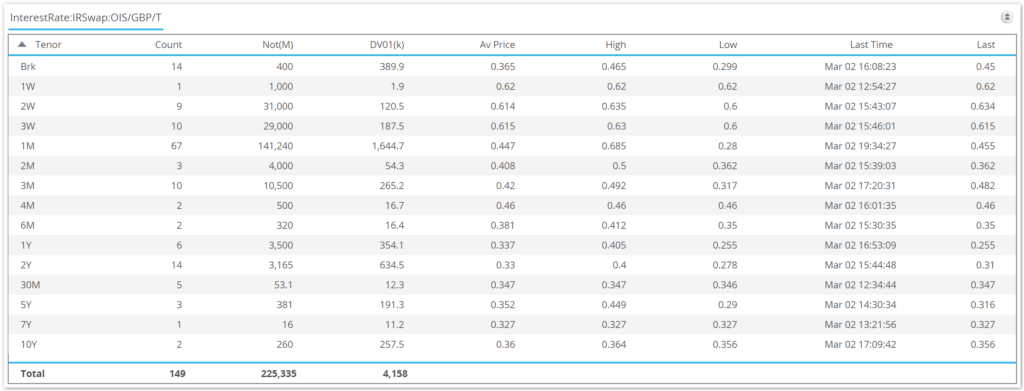

Final post for this live blog. This is how we ended up the day:

- 149 SONIA trades vs 238 in LIBOR.

- £225bn SONIA notional vs £13.2bn LIBOR.

- £4.16m DV01 SONIA vs £6.97m LIBOR.

- SONIA longest maturity 2049 vs 2068 LIBOR.

And just those 2 SONIA trades in 10Y!

There is clearly work to be done to move the market standard for GBP swaps away from LIBOR and into SONIA.

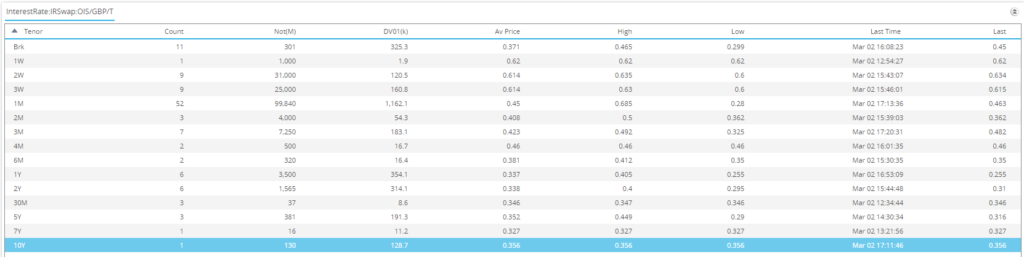

16:47 DMO Closes

According to Tradeweb, the Gilt closes are snapped at 16:15 London time. This can be associated with a wave of activity, so let’s assume we’ve now seen all of those trades reported to US SDRs (allowing for at least a 15 minute delay).

So final state of play is £3.17m DV01 in SONIA versus £6.36m in LIBOR. A gap of £3.2m DV01, or roughly double the amount of SONIA risk actually traded today.

16:45 London

What’s happening? I guess some activity on the close in GBP? 10Y SONIA has now traded twice. TWICE! And both are in block size, so proper risk.

Let’s hope some market makers are moving all of their net 10Y risk as the last thing they do today!

16:43 London

Finally 10Y SONIA traded. Whoop!

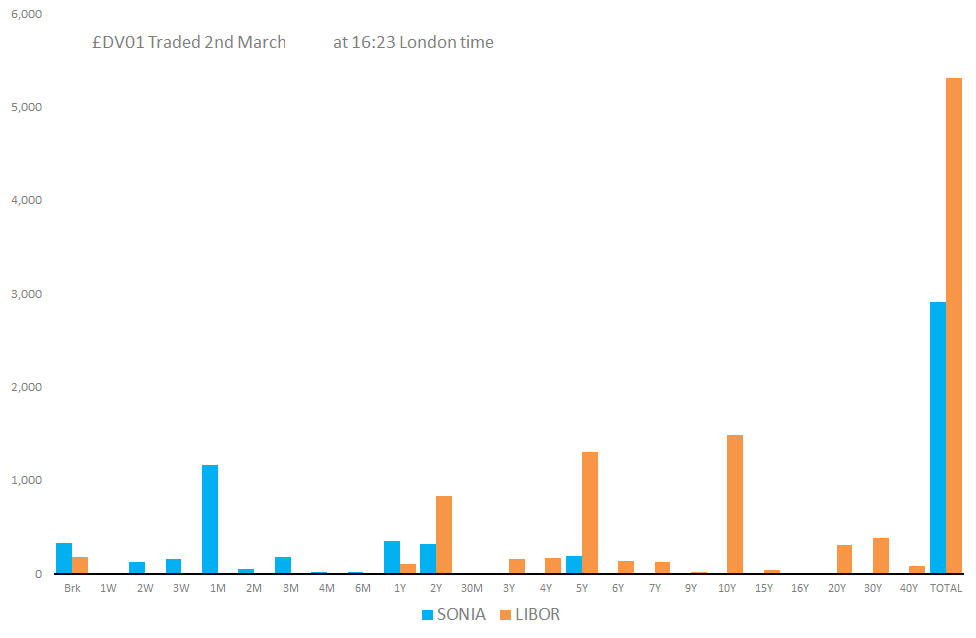

16:23 London

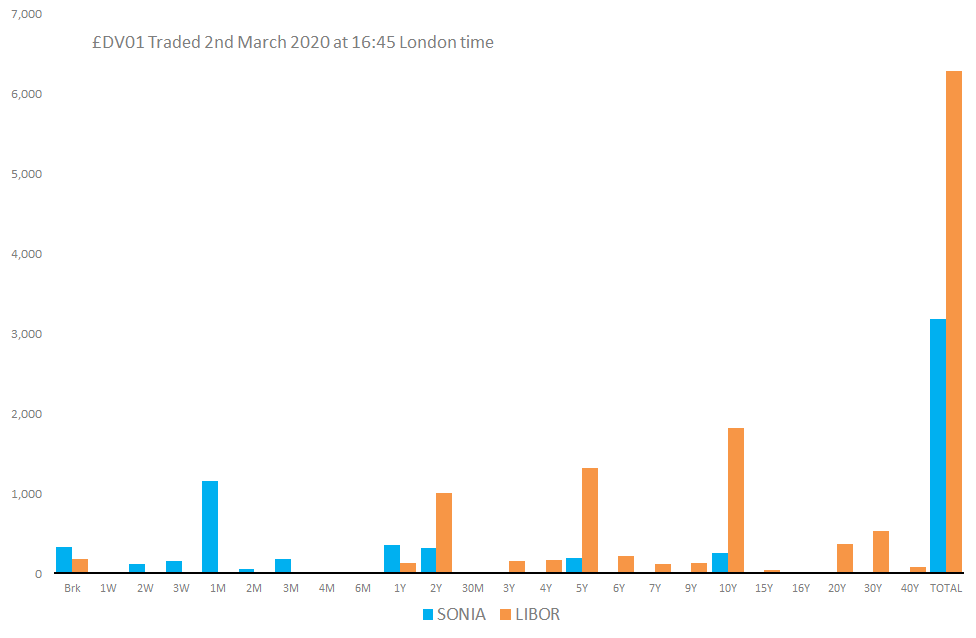

We are approaching the close of play for today. I doubt that there will be any meaningful new stories happening from this point on in terms of the balance of LIBOR vs SONIA risk that is traded.

We’ve seen nearly £3m DV01 of risk traded in SONIA swaps. This is very positive, but most of it has been short-dated.

82% of SONIA risk transacted was 2 years and shorter. 58% of SONIA risk was 3 months and shorter.

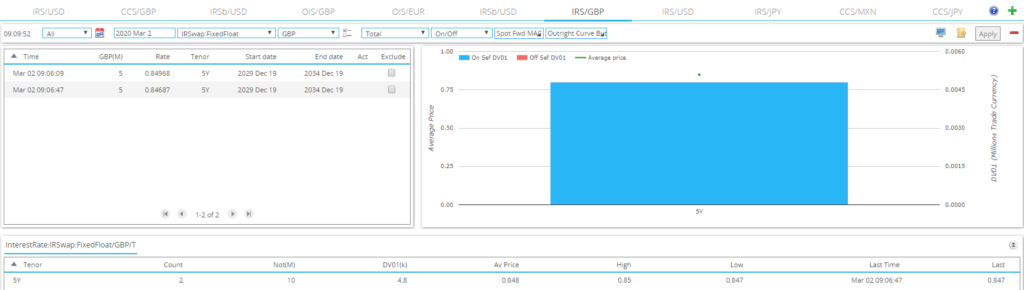

There wasn’t a single 10Y GBP SONIA trade, a benchmark maturity in UK swaps due to the Gilt future.

The amount of risk traded in GBP LIBOR 5y and 10y swaps alone was equal to the total SONIA risk traded today.

Liquidity in those two benchmark tenors has to transition to SONIA products before we can consider that the market convention for sterling swaps has moved to SONIA.

In case I fail to update again, it is just worth noting that this blog is based on US data from US SDRs. This is because US markets continue to set the gold standard for transparency in derivatives markets.

However, it also means that we do not have a complete picture of all trading in the market. We believe US SDR data to be representative of the market as a whole, and certainly for structural facets such as the split of SONIA and LIBOR risk there is no reason to think there would be a difference between US and Global markets. Nonetheless, it is always worthwhile to take a moment to understand the data behind this blog.

Hopefully we’ll have one more update for you today before markets close.

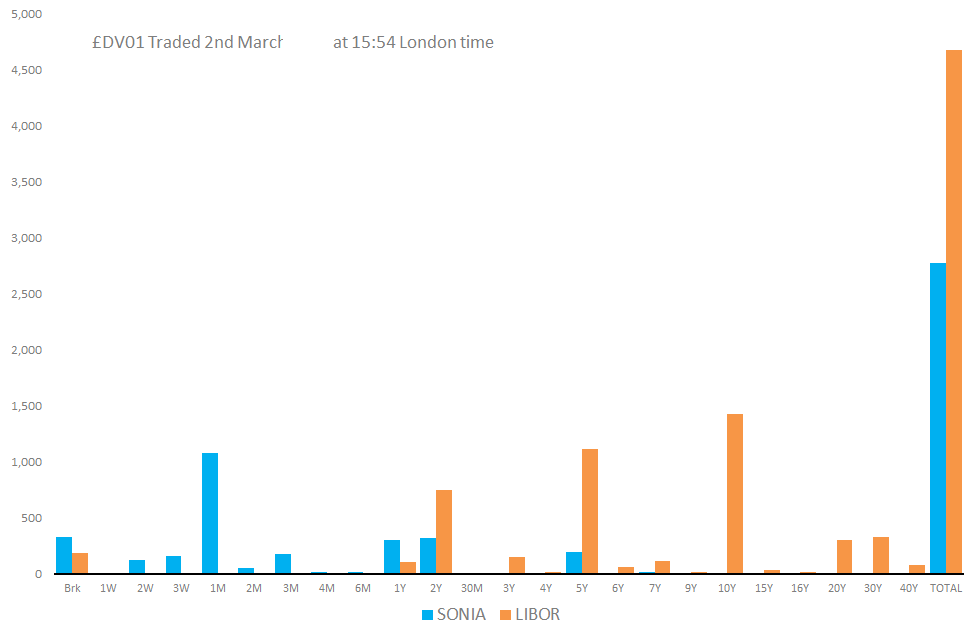

15:54 London

This latest bout of trading has really ruined my day. £1m DV01 of GBP LIBOR risk has traded without answer in SONIA markets.

It means that £2.77m DV01 in SONIA now plays £4.67m DV01 in LIBOR. Undoubtedly an unassailable lead.

15:35 London

£1m in DV01 separates the two markets. Total activity in 5y and 10y GBP LIBOR swaps is now £2m DV01. These are the most standardised, most liquid parts of the curve. Why haven’t they moved?

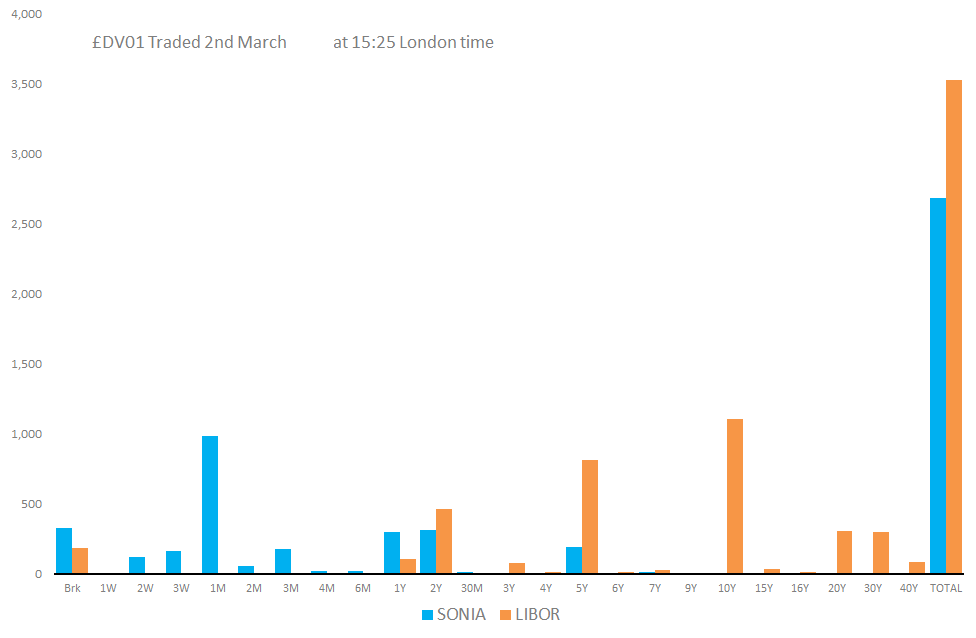

15:25 London

15:13 London

Needless to say that there hasn’t been a decisive switch today. SONIA and LIBOR are both trading. What this means is that secondary instruments, such as Swaptions and Cross Currency Swaps, remain firmly LIBOR-centric. It was not expected for these markets to transition today, but it does help to highlight how long a complete transition will take.

There are a lot of markets still addicted to LIBOR.

14:50 London

Another hour into the trading day, but this one saw a strong showing from SONIA. LIBOR risk hasn’t extended its lead.

- £2.47m DV01 of SONIA plays £3.18m in LIBOR.

I’ve decided I will continue to gripe about a lack of 10Y SONIA activity. Why aren’t people trading it versus the Gilt at least? Trade LIBOR today, pay twice (trade inception + unwind). Or just trade SONIA now.

13:50 London

This is somewhat disappointing. As more activity occurs in the US, our SDR data becomes a better indication of the entire GBP swaps market.

And this afternoon, there has been a marked move back to LIBOR activity.

Current situation:

- 71 SONIA trades vs 109 in LIBOR.

- £107bn SONIA notional vs £4.2bn LIBOR.

- £1.57m DV01 SONIA vs £2.21m LIBOR.

- SONIA longest maturity 2049 vs 2060 LIBOR.

I’m not giving up on SONIA and it’s not been a bad day. But I’m not sure I would say that the market standard (from our data) has convincingly moved to SONIA today.

13:05 London

No surprise to see the SDR busy as New York is active. Recent trades have caused LIBOR to extend its lead over SONIA however.

We now have £1.37m DV01 of SONIA risk versus £1.73m DV01 of LIBOR risk. That might be an unassailable lead for LIBOR. But it is well short of the 3x multiple that we saw on Friday. So certainly some signs of transition taking hold.

It does shock me that 10Y GBP LIBOR swaps can trade 23 times today. That is about 25% of all LIBOR activity. And yet not a single SONIA 10Y swap has traded. Something seems wrong with that, no?

12:57pm London

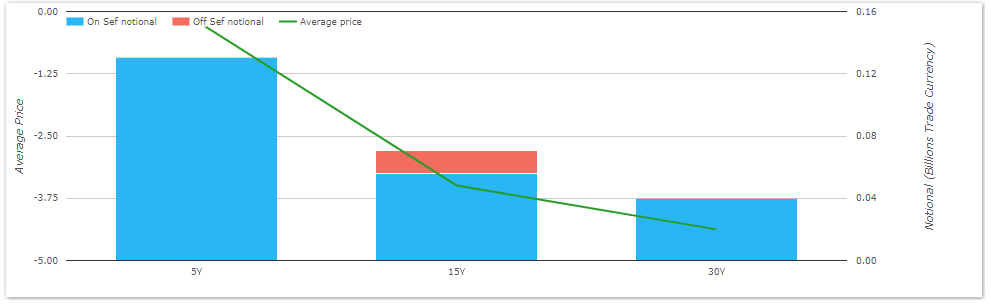

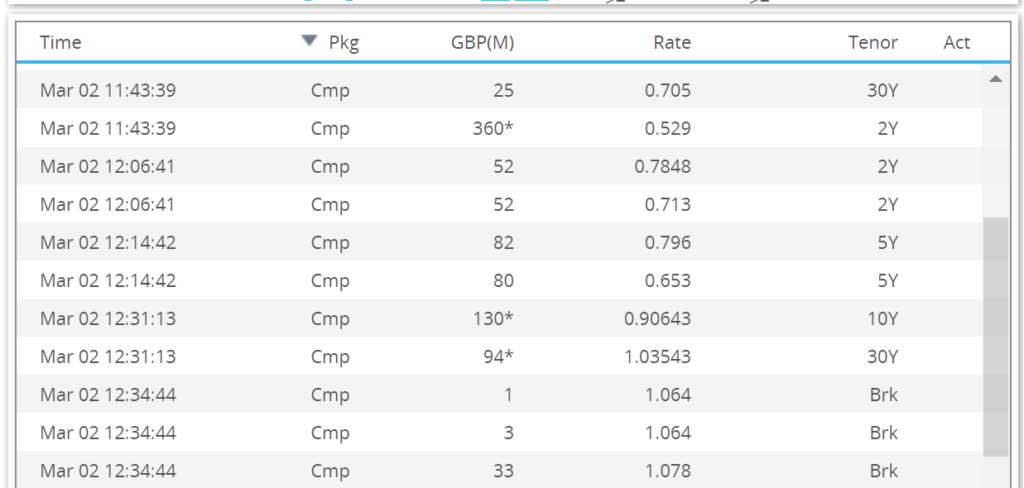

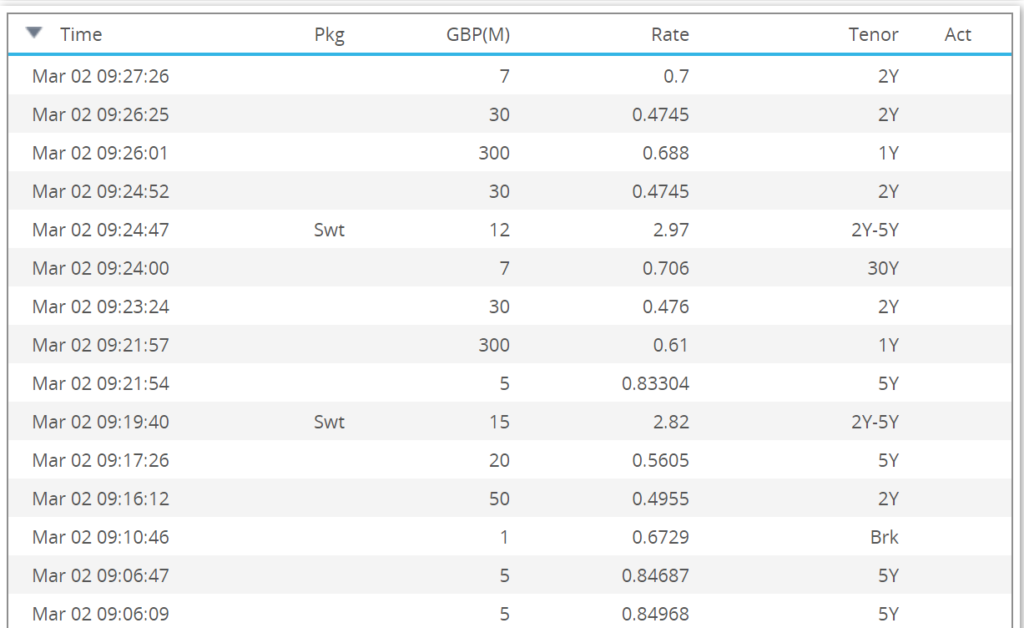

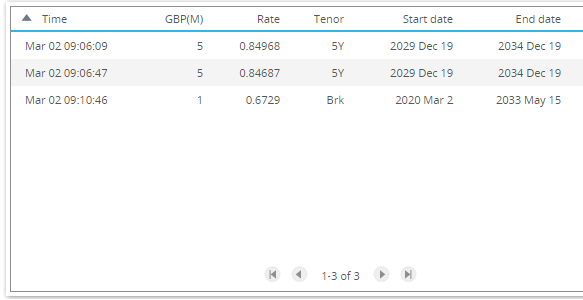

More long-dated SONIA trading again, this time out to September 2037. That looks like an asset swap versus the 2037 Gilt to me:

12:45pm London

More SONIA coming through again now, taking total risk up to £1.26m DV01. That is still lagging the (compression excluded) LIBOR total of £1.44m DV01.

That’s not fitting my anticipated narrative very well. Come on SONIA traders, more long-dated risk please.

12:30pm London

What should I make of my inbox today then? I set up alerts every time GBP LIBOR was reported to the SDR. There have been 81 trades so far today. And in that time, I haven’t received a single alert for SOFR activity:

What does this mean for LIBOR transition and RFR activity? Are these 81 trades going to be followed up on today, to find out why they absolutely had to be transacted versus an index that won’t exist at trade maturity?

A tap on the shoulder like that would surely accelerate RFR take-up, no?

12:24pm London

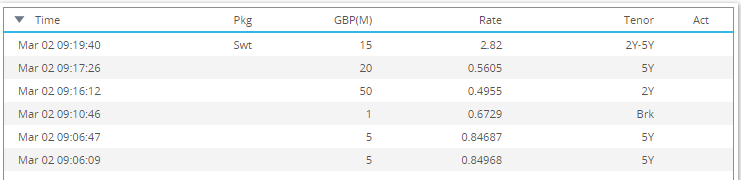

We’ve now seen our 50th (and 51st) SONIA trade of the day. Activity has extended out the curve, with trades maturing in 2049, 2030 (including a 5y5y forward maturing in 2030), 2028, 2027 and a 2y4y forward maturing in 2026 that traded above block size.

All of this has helped to accrue £1.1m DV01 in risk and £77bn in notional for SONIA swaps.

That is all good, but LIBOR has also seen a more activity recently, pushing total risk up to £1.36m in DV01.

SONIA caught up last time it started to lag – will we see more SONIA activity in the next hour as a result? Stay tuned…

12:03pm London

Some big LIBOR trades have been compressed/unwound today, including three block trades in 2Y, 10Y and 30Y. This is a potential good sign that LIBOR exposures are being unwound. It would be even better to see some evidence of them being replaced by SONIA trades!

11:59am London

Yes SONIA! We finally have our long trade of the day. Maturing 2049, £17m.

This means that the risk split SONIA vs LIBOR is now roughly back to equal at £1.1m DV01 in each.

11:53am London

State of play:

- 48 SONIA trades vs 72 in LIBOR.

- £70bn SONIA notional vs £2.1bn LIBOR.

- £1.05m DV01 SONIA vs £1.16m LIBOR.

- SONIA longest maturity 2030 vs 2050 LIBOR.

LIBOR figures exclude Compression and aged trades, as I figure any activity in these is a good sign for LIBOR transition!

11:08am London

Some GOOD GBP LIBOR trading activity. Compression in 2 year swaps. This should be getting rid of gross notional outstanding, reducing firms reliance on LIBOR. Bravo!

11:01am London

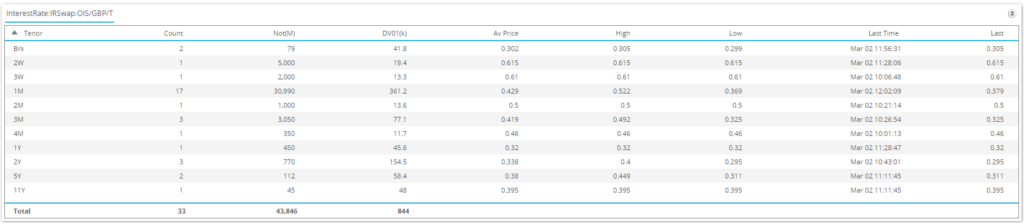

SONIA is catching up again. £844k DV01 now transacted in total for SONIA markets. Maturities from 2 weeks through to 11 years. A huge notional amount of £44bn as well (mainly in 1 month maturities).

Trade number is telling though. 33 SONIA swaps plays 62 LIBOR swaps. That says to me that clients (smaller tickets, more of them) need to step up and transition to SONIA as well today.

10:58am London

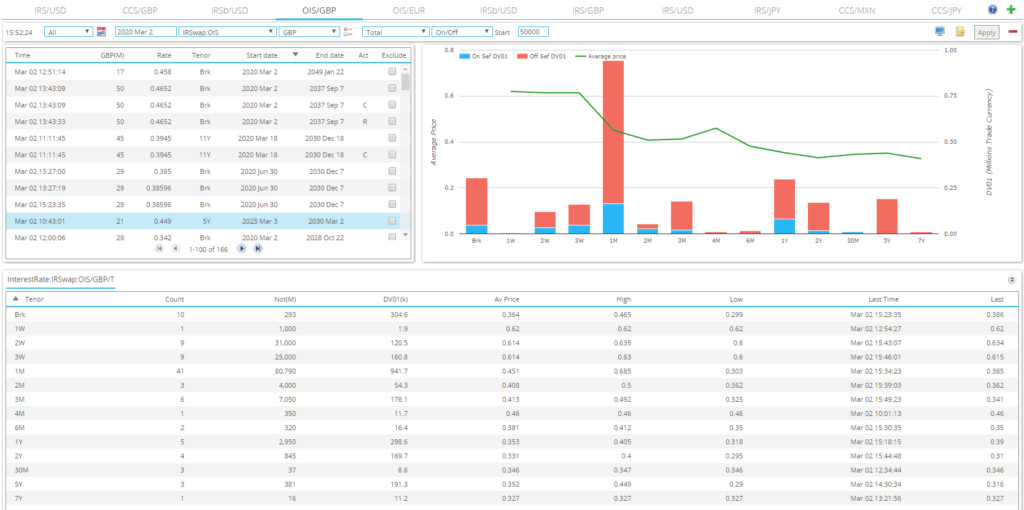

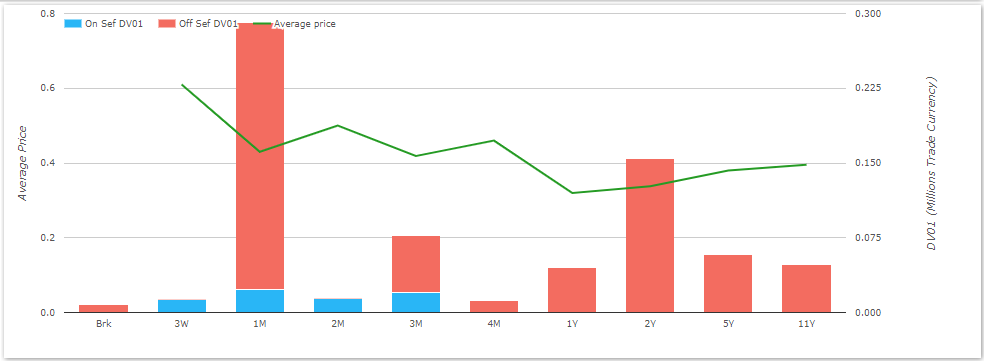

Here’s a reminder to all the SEFs out there that the market standard is now SONIA in GBP Swaps. Why is so much SONIA traded off-SEF?

10:40am London

LIBOR risk is continuing to tick higher right now, and is fast approaching the £1m in DV01 marker (£991k to be exact). This is now some 30% higher than in SONIA. We need some long-dated SONIA to trade!

Elsewhere, there has been a 5y5y swaption reported. And this was done versus LIBOR. Looking through the SDR history, I can only find one single swaption transacted versus SONIA, done back in November.

So GBP options traders. Today would be a good day to trade another SONIA swaption please!

10:35am London

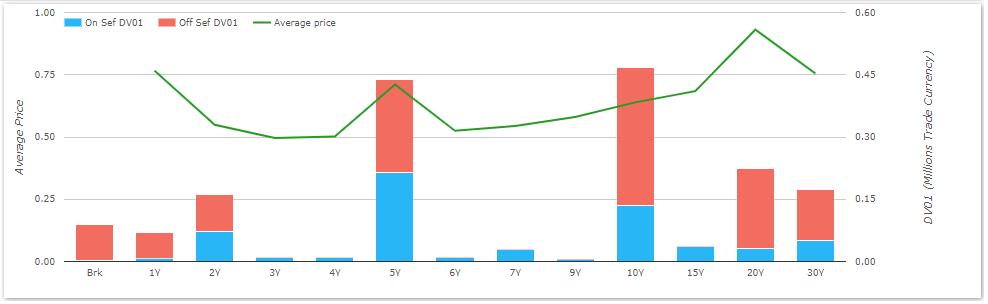

Over halfway through our morning session in London and LIBOR markets have edged out a lead. However, we have seen more long-dated SONIA trading, with 11Y the latest to hit the SDR tape.

£701k DV01 in SONIA now plays £847k in LIBOR.

Not quite the 50/50 split we had earlier, but still way short of the relative amount of LIBOR risk that traded as recently as Friday.

09:55am London

As we follow the markets in close to real-time today, it’s fascinating to wonder how “normal” this situation is. The total amount of DV01 traded in SONIA swaps is still higher than in LIBOR today. Markets really seem to have listened.

I’d like to see some 10y and 30y SONIA trade to be sure that something is really happening.

But right now, £505k DV01 in SONIA plays £475k DV01 in LIBOR. On Friday, three times as much LIBOR DV01 traded as SONIA (£9m versus £3m DV01).

Are we actually seeing the transition play out today?

09:45am London

Alright SONIA traders! Now we have some news. 5y SONIA just traded. This takes the total risk traded to £440k DV01, pretty much level-pegging with LIBOR markets today.

It really does seem that liquidity is beginning to move. Quite a change from our first 60 minutes of blogging today.

09:29am London

So things changed quickly since the start of this hour. There has been more risk transacted in SONIA swaps than in LIBOR swaps. SONIA has now traded out to 2 years.

To stress, there have been no block trades in LIBOR. But SONIA has seen block-sized activity transacted. That is a really good sign for liquidity moving away from LIBOR and into SONIA.

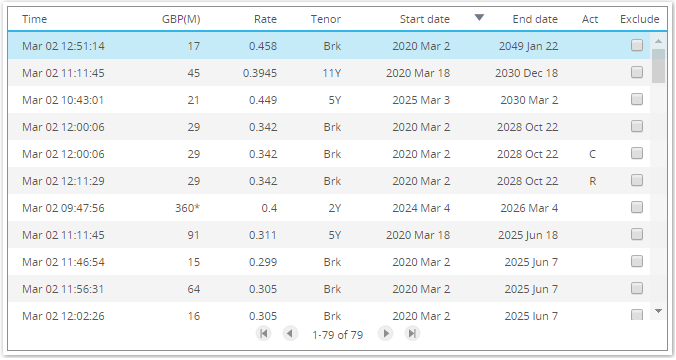

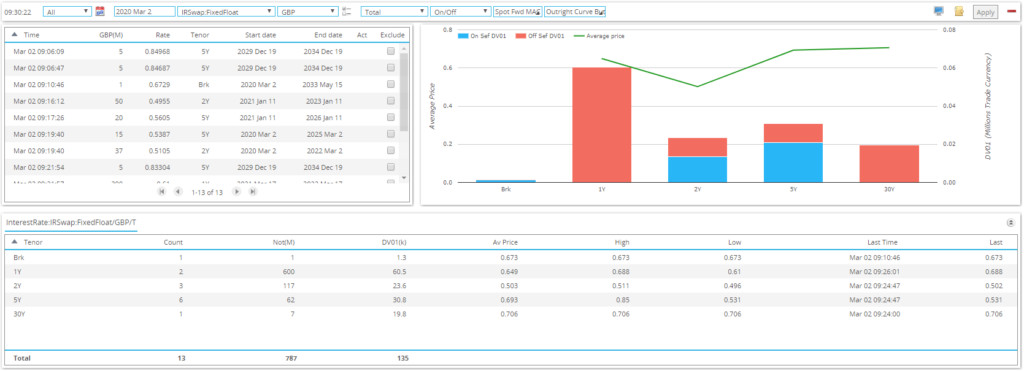

Here’s a review of the 15 SONIA trades, accounting for £18.5bn in notional and £391k DV01 of risk:

09:24am London

Two large block trades in 2y SONIA mean that a lot of risk is now going through SONIA markets. They were both executed off-SEF, so I won’t be able to tell you their exact size. But we generally believe GBP block trades are 25% larger than their reported notional amounts. So the £360m notional amounts marked with an asterix below should be assumed to be £450m in reality:

09:22am London

I want to dwell and highlight the below a little bit more. In the past 20 minutes, thanks to large activity in 2y SONIA, the amount of risk transacted in SONIA is now greater than in LIBOR.

That’s what the BoE wanted to happen on this Monday morning.

Well done GBP Swaps traders.

09:20am London

Scores on the doors after the first ~90 minutes of trading:

- 12 SONIA trades vs 28 in LIBOR.

- £14.4bn SONIA notional vs £1.1bn LIBOR.

- £316k DV01 SONIA vs £309k LIBOR.

- SONIA longest maturity 2026 vs 2050 LIBOR.

09:02am London

SONIA activity finally extending out the curve! Sadly, it’s only made it out to the 30th June 2020, so not too much to blog about in SONIA markets just yet.

08:57am London

As the initial spate of outright hedging calms down a touch, we see more packages transacting, particularly 2s10s. Maybe now that knee-jerk reactions to the outright move lower in rates this morning has calmed down a touch, we can see more activity transitioning to SONIA?

Total risk transacted in LIBOR swaps just ticked over £305k DV01. Last week we averaged about £9m DV01 per day in GBP LIBOR swaps for context.

08:55am London

SONIA keeps on trading. We’ve now had £120k DV01 of risk reported to the SDRs, all in the first two MPC dates. May just traded at 0.39%, already up off the earlier lows.

08:50am London

And a 2s10s spread in GBP LIBOR markets takes us over a £1bn of notional transacted within an hour of GBP swaps markets opening this morning. Not a particularly meaningful landmark. Far more interesting is that we continue to have activity all the way out to 30 years in LIBOR markets, and that no long-dated SONIA has yet been reported.

08:47am London

More SONIA trading….amidst an otherwise LIBOR-dominated landscape. We’ve now had 6 SONIA trades, all ~4-6 weeks in maturity, corresponding to the first two MPC dates. A total of £10bn notional has traded, it is just such a shame that activity remains concentrated in the very short-end for SONIA markets:

08:40am London

3y5y7y butterfly just traded in GBP LIBOR swaps. Without outright exposure, with the basis in SONIA-LIBOR static post 2022, these should be the first pockets of liquidity that will only be traded in SONIA space. Aren’t they?

08:37am London

Looking at the ticker of activity in GBP LIBOR swaps today, I’m not sure anything has changed with regards to market standards. All long-dated activity continues to be in LIBOR swaps.

I was warned this would happen. Liquidity isn’t just a switch that can be transferred on a given day:

Or are we missing some data? Let us know if you think SONIA activity has picked up today.

08:32am London

Phew, more SONIA activity! I was beginning to get worried.

And this is proper size. 5 yards of the March MPC has just traded, at 0.475% – almost certainly pricing-in a cut for the 26th March by my maths.

Still no SONIA executed longer than June 2020 though.

08:30am London

It’s a busy open for GBP swaps traders. We now have activity across the curve from 1y swaps all the way out to 30y. And all in GBP LIBOR. £787m in notional has now been reported, and the amount of risk has increased substantially in the last five minutes, to hit £135k DV01.

All of the meaningful activity remains in GBP LIBOR swaps at this early point in time:

08:25am London

Plenty of activity, enough for me to consider turning off my GBP LIBOR email alerts for today!

State of play in DV01 traded is £55k GBP LIBOR plays £15k GBP SONIA. So over 3.5 times as much LIBOR risk has traded today. And in SONIA, nothing longer than June 2020 has been reported to the SDRs:

08:23am London

You have to have some sympathy with the GBP market here. Rates are plummeting – with the May MPC now trading at 0.369%. Good to see SONIA activity even when markets are volatile, but LIBOR exposure (measured by trade count and DV01) is so far outstripping SONIA today.

08:20am London

Our first proper sized trades of the day and they are all in…..LIBOR. Doh.

5y GBP and 2y GBP (which I think has traded as both outright 5y and 2s5s maturity spread):

08:15am London

Okay, so 3 LIBOR trades play 2 SONIA trades so far. Let’s see where that count will end up during the day.

And just a note. If you happen to see one of your trades here on the blog and want to tell us more about it, please feel free to reach out. We’re more than happy to help get the message out there if these LIBOR swaps are flattening exposures or any other reason for putting on fresh LIBOR positions today.

08:12am London

More GBP LIBOR. Just £1m notional. Maybe an unwind?

08:10am London

My first email alerts of the day just went off. This is bad news. It means someone has traded GBP LIBOR swaps. Uh-oh, don’t they know it is SONIA DAY today?

These are 5 year trades starting in 9 years. Not only is it surprising to see forwards trading right at the open, but these are maturing way past the 2022 date for no more GBP LIBOR.

08:05am London

Another trade. SONIA again. May MPC again. This time even lower at 0.40%. Both trades have been sized identically at £400m, which is just shy of £5k/$6k DV01, so fairly small so far.

07:55am London

I nearly spat my coffee out, I wasn’t expecting GBP swaps traders to actually transact before the Gilt opened!

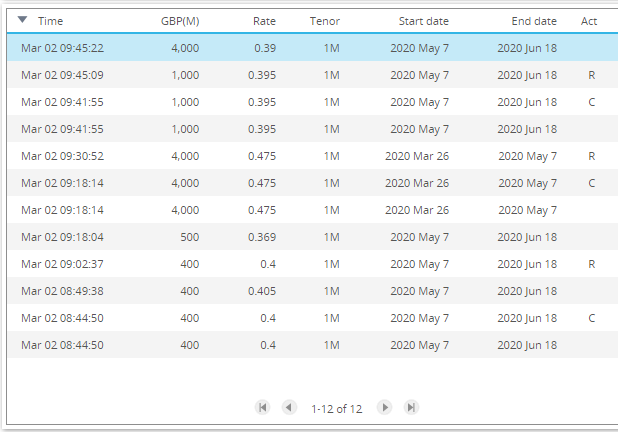

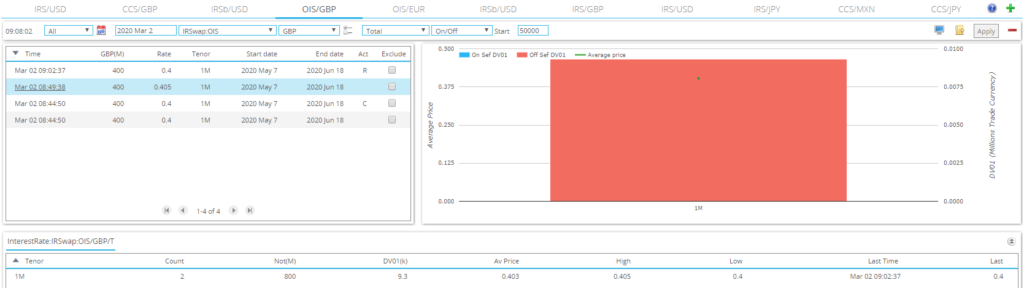

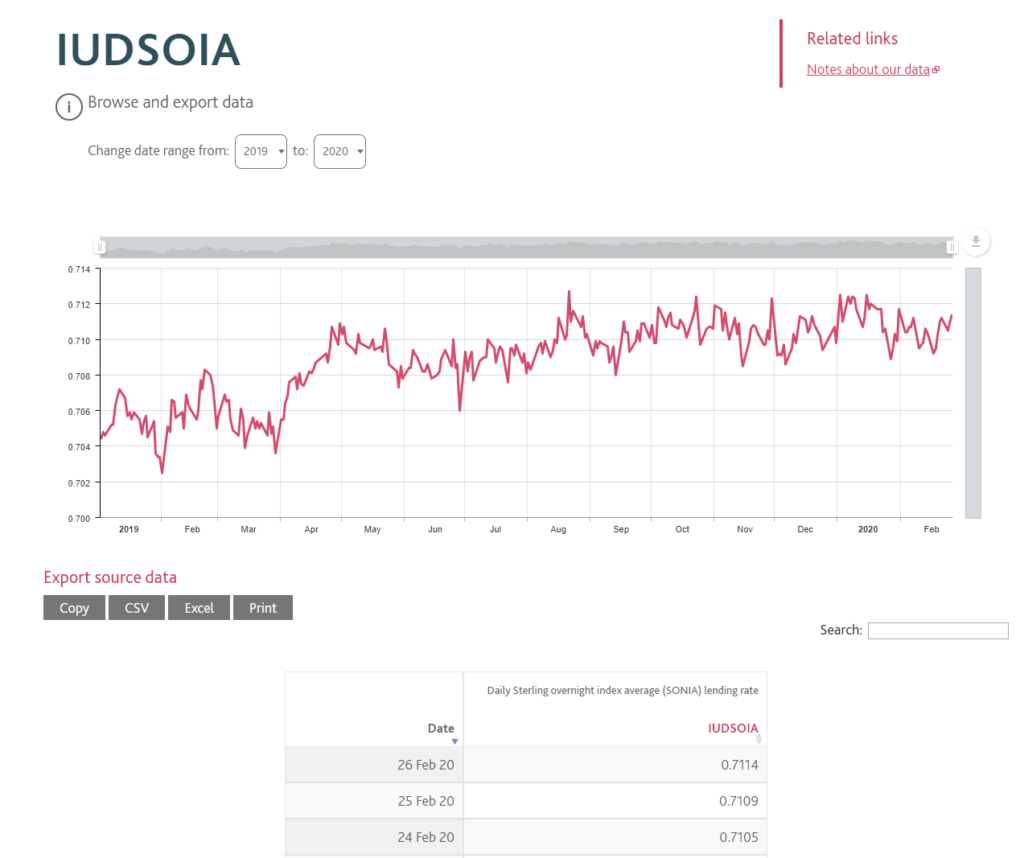

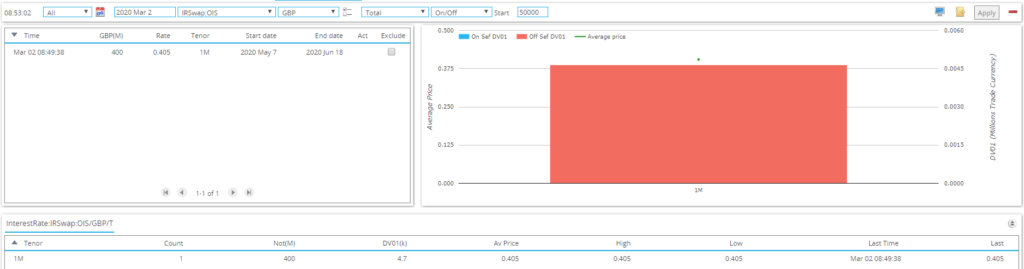

A bit of detail on the first trade. There have been no LIBOR swaps so far. The early SONIA trade is a short-dated 1 month swap, running May 7th to June 18th. These are the MPC dates for the meeting in May, which also sees the publication of the next Monetary Policy Report. That means it is penciled in as a likely date for a Rate change.

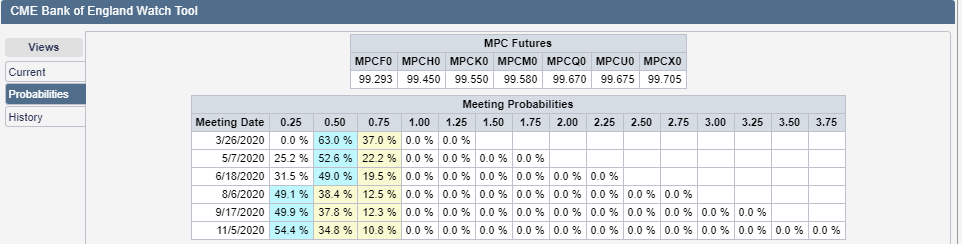

The swap traded at 0.405, compared to the current SONIA fixing of 0.71. That is pricing in more than one rate cut, but seems broadly in line with the CME Rate Watch Tool:

07:53am London

We have our first GBP SONIA trade of the day!

07:50am London

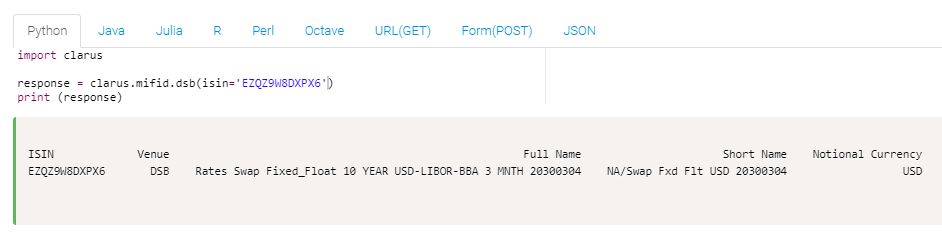

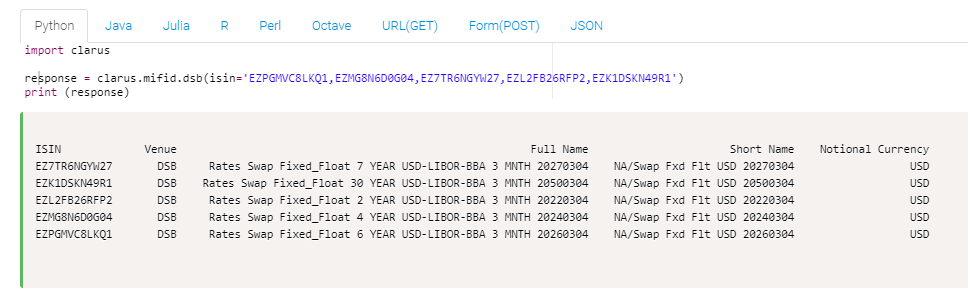

Ten minutes before we expect any trades in GBP markets, but I have at least found some usable pre-trade transparency, thanks again to Bloomberg. Why can’t all publication arrangements under MIFID II just copy what Bloomberg do? Please.

The pre-trade transparency on the Bloomberg MTF is available here. I spotted some 10Y USD IRS in the slice file I downloaded, with ISINs that I can actually consume and decipher. Well done (again) to Bloomberg for actually providing usable transparency under MIFID II.

07:20am London

When is it realistic to expect GBP trades to hit the US SDRs? Looking at Friday’s data, we had both SONIA and LIBOR swaps reported just after 8am London time.

07:15am London

Will there be any MIFID II data today for GBP swaps? I was hopeful that we might learn something from European transparency. However, aside from the vain hope of spotting a GBP ISIN for some pre-trade transparency at an APA or MTF, it looks like we won’t see any post-trade data for GBP swaps.

This is because all GBP swaps are reported with a “FWAF” deferral. We get some information on the Tuesday morning, but full volumes are not reported until 4 weeks after the trade. FOUR WEEKS!

Maybe I should write a “Not quite live blog” for SONIA day on the 30th March?

07:05am London

We are still one hour away from the Gilt future opening in London, and it’s pretty unusual to see any activity in GBP swaps before then. So not much surprise to be seeing empty screens at the moment.

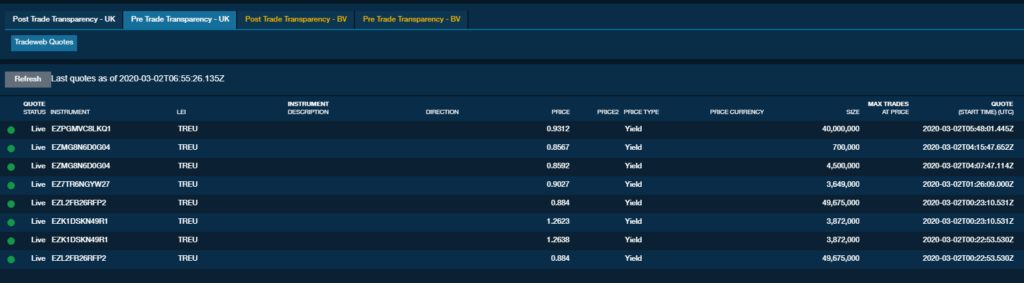

It does give me a chance to delve once again into the mess of MIFID II data out there. Tradeweb (who still don’t make the data usable in any way – I cannot copy or consume these ISINs) are showing some pre-trade transparency on their APA already:

But because it’s all quiet here, I do at least have time to manually type in those ISINs to find out what has been quoted so far. They are all USD swaps. No GBP yet:

Just to be clear. Yes, I had to manually type in all of those ISINs to decipher what the information published by an APA actually means. So much for meaningful transparency Europe! And Tradeweb, just enable copy/paste on your website. At least for SONIA day!!

Monday 2nd March 06:50am London

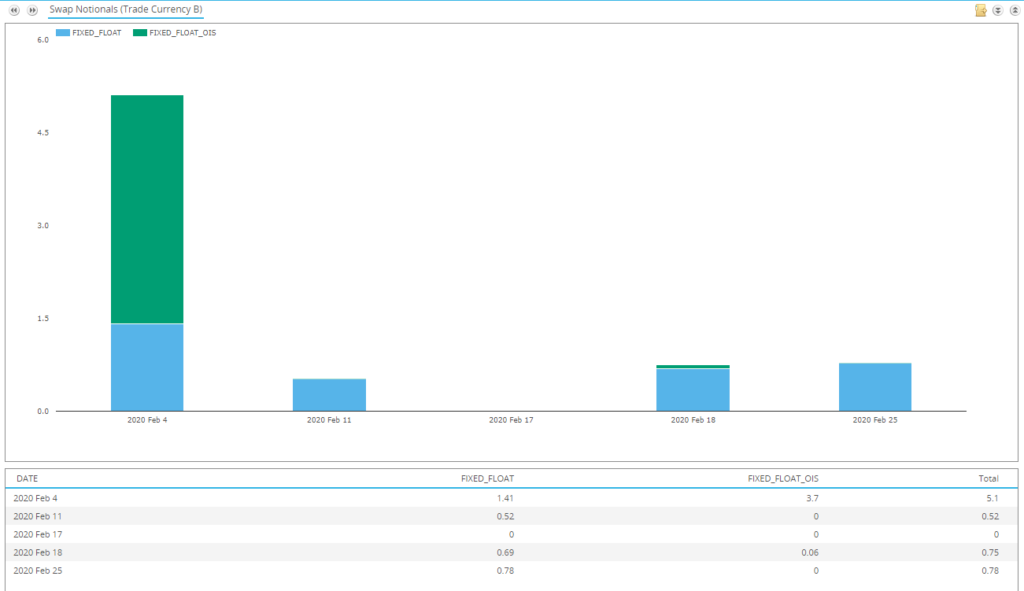

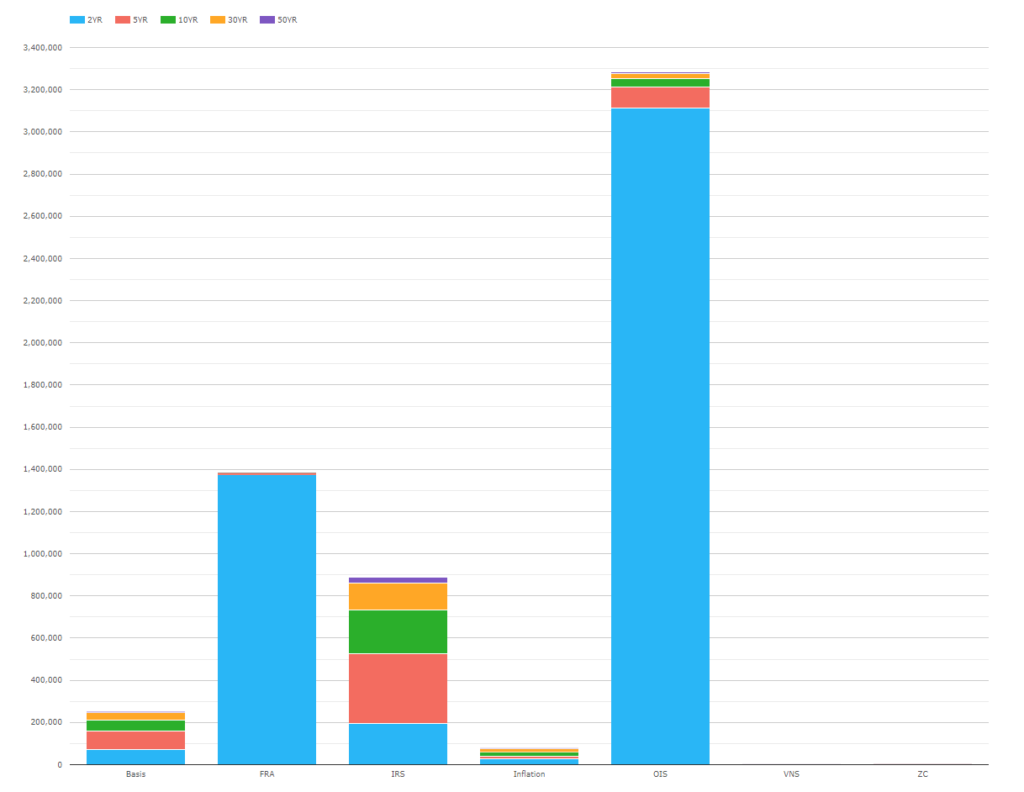

As we wait for the first trades to tick into MIFIDView and SDRView, it’s worth taking a look at CCPView to see what traded in February. Up to the 21st of the month, SONIA-based GBP derivatives were far outstripping their LIBOR-brethren:

With most FRAs executed as part of volume matching runs on a single day (looks like those happen on a Tuesday for GBP FRAs) we will be concentrating on that near-$1trn of IRS activity in the chart above. These were traded as LIBOR swaps during February 2020. Will this activity move into the OIS sector?

Significantly, will we see many more long-dated SONIA trades executed today?

Monday 2nd March 06:30am London

Today we’ll be monitoring both SDR and MIFID data to look at GBP swaps trading. Will there be vanilla LIBOR swaps transacted? Will the market switch all meaningful liquidity into SONIA? What about Cross Currency swaps and Swaptions?

Right now I am looking at empty screens, waiting for the first trades of the day:

Hello Chris,

Thank you for the live blog day, it was very interesting.

I was wondering, do you plan any updates on this specific subject? Like end of month, to see if there is any progressive change of market convention?

Best regards

Many thanks, glad it was useful! Yes, we’ll be following this up with a regular look at SONIA volumes relative to LIBOR, probably starting next week.