Earlier this month, I predicted that just like the CDS market moved to standardized contracts a few years ago, the day would come when the interest rate market would move to a standardized world, namely in the form of Market Agreed Coupon contracts (MAC). The logic being:

- Managing line items in a cleared world is easier because they naturally compress ala futures

- Additional swap line items of swaps are a Basel III no-no

- Standardization promotes liquidity; and liquidity promotes more liquidity

- Firms looking to take a view on 5YR risk want to have luxury of getting in today and getting out tomorrow without any residual basis risk

- Firms looking to hedge specific dates may determine that the cost savings and liquidity in MAC contracts outweighs the associate basis risk

Over the past couple months, Amir Khwaja has written a couple articles here and here where he observes the size of the MAC market as well as the roll activity on a couple SEFs. I wanted to take a larger look at the activity over the past year to see if we can make out any real growth.

Brief History

First a brief history lesson on MAC contracts:

- April 2013: MAC contracts developed and launched by SIFMA and ISDA

- November 2013: Bloomberg announces they are the first SEF to execute a MAC contract

- December 2013: ISDA announces CUSIPs are available for MAC contracts to aid in communication between participants

- February 2014: TW’s MAT submission goes into effect, explicitly making USD MAC contracts made-available-to-trade (next 2 IMM dated MACs)

- April 2014: ISDA announces the publication of a MAC confirmation with standard terms

MAC contracts are really pretty easy to get your head around:

- Standard coupons. Just see SIFMA website for fixed rates (eg the 5YR USD MAC is currently 2.25%)

- Standard IMM start dates

- Standard tenors

- They have CME and LCH CUSIPs (and ISINs) just like a security

The only possible confusion is the quoting convention, which seems to be either in bond price format, decimal variation thereof, or a classic PV. To convert between them:

- Given a Decimal Price of say 100.9375

- Bond Price: Convert 0.9375 into 32nds by dividing by .03125, hence bond price = 100-30

- PV: (Price – 100) * Notional/100

The notional in the PV calc is positive for receiver swap, negative for a payer. Pretty easy.

The Past Year

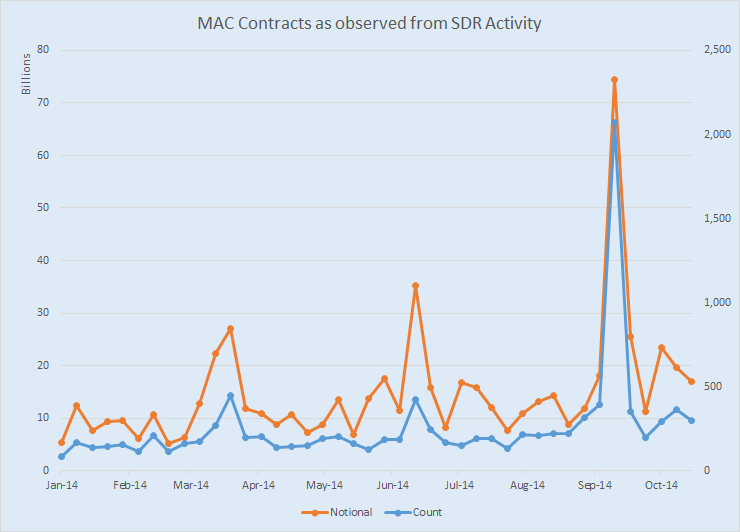

So to begin, lets take a look at the activity of all MAC transactions since the start of 2014. Each point representing that week’s activity both on and off SEF. The orange line is the notional traded, and the blue line the number of trades in that week.

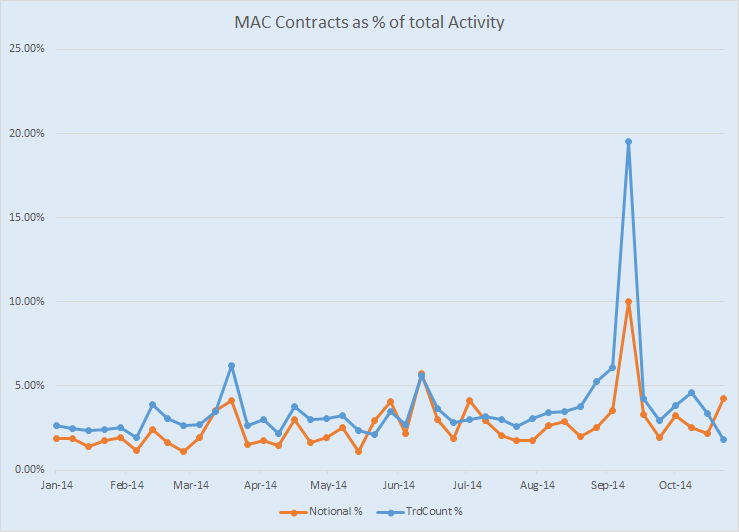

This seems to tell us there has been only a slight adoption of MAC contracts over the course of the year, starting with a couple hundred per week earlier in the year, maybe up to a “few” hundred in October. The large spikes reflect the quarterly roll activity. Of course if you are like most people, you have no idea what 10 billion dollars of fixed/float swaps means. So below, I chart these notional and trade counts as a % of the overall.

Not so much in it. Less than 5% all year long. And notably not much growth.

How About On SEF

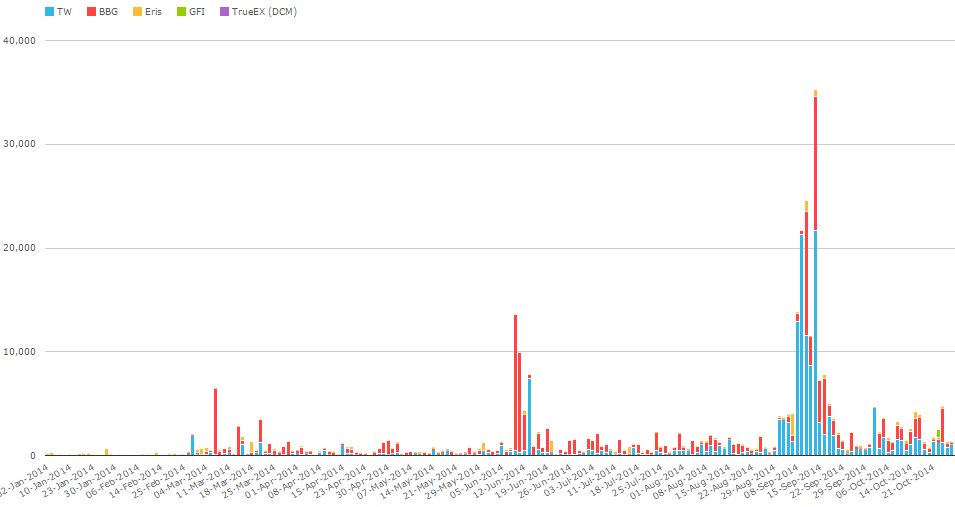

Lets now look at SEFView and hence monitor just the On-SEF activity. Here, we can more notably see a trend. Once again the quarterly rolls are pronounced, but we can more readily make out some degree of growth of MAC trading.

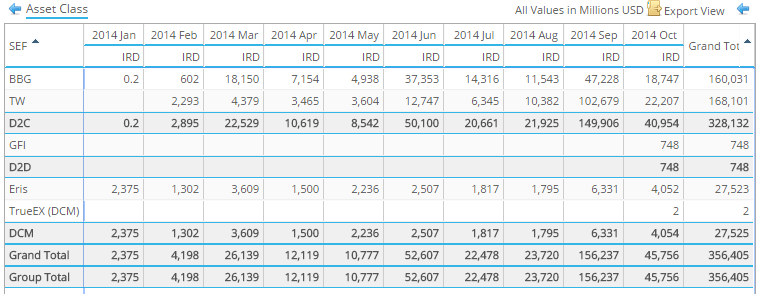

So where is the MAC activity on SEF? You can quite clearly make out the Tradeweb (blue) and Bloomberg (Red) bars above, and I’ve also included the Eris Standard swap futures (yellow) in this picture as a reference. However in the table below, you can also see that both GFI and TrueEx have just begun putting through numbers in October.

Rumor has it that GFI and Javelin will have their order book for MAC contracts up and running sometime in November. Other rumors have more MAC order books within the IDBs popping up shortly thereafter. Which begs the question, with what can be seen as fairly subdued overall growth in MAC, why is everyone betting there will be a demand for a MAC order book? I think it goes back to the points that I listed out to begin the article; it just makes sense that these products will gain traction soon.