Get ready to geek out on some short-end USD Rates background.

Fed Funds

Fed Funds (as I know it), or the more official sounding “Effective Federal Funds Rate (EFFR)”, is a key overnight interest rate for USD. It didn’t quite cut the mustard as the official Risk Free Rate though – that title goes to SOFR in the US.

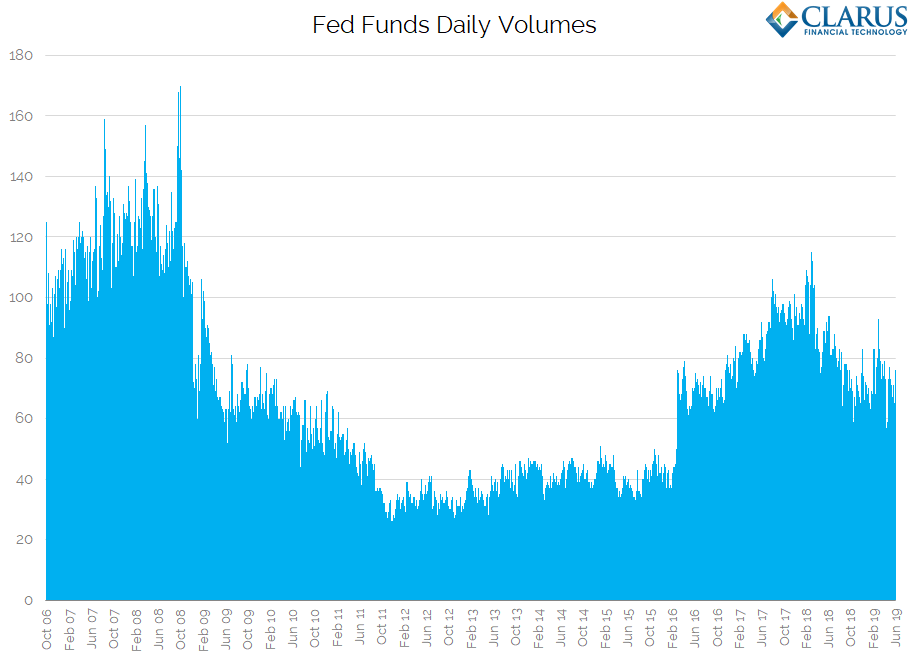

Fed Funds is a volume-weighted median average of unsecured overnight lending transactions taking place on-shore each day. It is administered by the New York Fed. Details and data are to be found here.

GSEs and Fed Funds

Government Sponsored Entities, or GSEs, dominate the Fed Funds market. They are typically the suppliers of liquidity – i.e. they lend cash at Fed Funds overnight to onshore US banks.

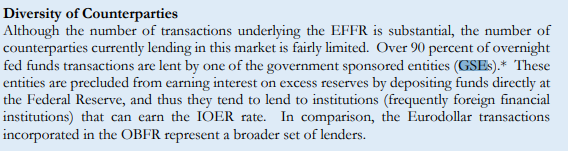

The ARRC interim report served to highlight just how dominant GSEs are in the Fed Funds market – over 90% of trades involve a GSE lending cash:

There is also a link to the source data, which is from a Simon Potter presentation back in 2016. This shows that the GSEs are consistently over 90% of the Fed Funds market every single day:

Further digging, and aided by some helpful readers, reveals that these GSEs are actually the Federal Home Loan Banks (FHLBs). Why are they so active in this market?

FHLBs

There is a great series from back in 2017 in FEDS Notes all about FHLBs, called “The Increased Role of the Federal Home Loan Bank System in Funding Markets”;

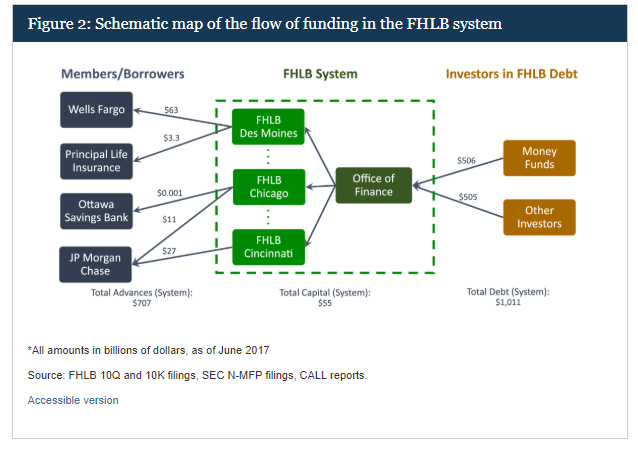

If, like me, you are coming at this fresh and don’t know much about the Federal Home Loan Banks, the diagram below is a great summary:

Showing;

- Banks (and insurance companies, credit unions) can borrow money from the FHLBs.

- These borrowings are collateralised by mortgages and “mortgage type assets”.

- It is up to the FHLBs what interest rate, what haircut they take on the collateral, and what terms they offer to their members.

- However, all FHLBs enjoy a “front of the line” priority if a borrower defaults – a so-called “super lien”.

- Essentially, therefore, FHLBs are able to offer maturity transformation to their institutional members whilst enjoying relatively low funding costs in the market as a whole.

- FHLBs enjoy low funding costs for three main reasons – 1) over-collateralisation coupled with the super lien 2) an implicit government guarantee and 3) if one FHLB cannot meet its’ obligations, they are transferred to the other 10.

Overall, whilst FHLBs are highly leveraged – they have just 5% capital versus their assets – they are considered relatively “safe” intermediaries, providing important maturity transformation for the private sector.

The Role of FHLBs

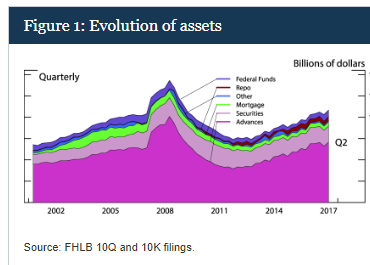

In Part 2 of the FEDS series, I discovered that FHLBs were able to substantially increase the amounts of money they were lending to their members during the financial crisis.

I find this interesting because:

- That means markets were still happy to lend to FHLBs, even though they appear to be thinly capitalised.

- The lending contracted very quickly and has only recently surpassed pre-crisis levels:

So why has borrowing increased again? The article clearly points out the regulatory drivers behind it. Banks are able to transform illiquid mortgages into liquid advances from an FHLB and go out and buy High Quality Liquid Assets (aka USTs) with it. That makes the balance sheet look a whole lot healthier and helps with the Liquidity Coverage Ratio (I’m going to have to write a blog on LCR, I can see….).

Fortunately, the FHLBs are able to expand their balance sheets to meet these requirements from members thanks to more and more money market funds buying up their debt.

There’s an interesting interplay between two completely different sets of regulation for you (LCR vs money market fund reform!).

Maturity Transformation

I don’t want to dwell about the potential Financial Stability implications of the increased role of FHLBs – that is sufficiently covered in Part 3 of the FEDS notes. One thing I would note is that their activity seems to be very transparent, which has to be a positive for the system as a whole.

But we can also see why they are so active in the Fed Funds market. They lend funds overnight to the tune of about 7.5% of their total assets. This is

“to meet regulatory required contingent liquidity buffer.”

And Back to Fed Funds

My main motivation for writing this blog was to plug one of many gaps in my knowledge.

I honestly didn’t really understand why we needed SOFR in the USD market. Changing bilateral CSAs from Fed Funds to SOFR and the upcoming PAI changes at CCPs just seemed pointless. Let’s all just stay on Fed Funds?

However, with a bit of digging, I can now see that Fed Funds is a very peculiar market in itself. It doesn’t really seem healthy to have such a large derivatives market based on a rate that is 90% ruled by the FHLBs.

SOFR must have a more diverse range of participants.

Finally

With all of this data on Fed Funds and FHLB activity in the public domain, it would be highly beneficial to see the same for SOFR.

Can transaction level data for the SOFR fixings ever be released?

If it were to be classified by counterparty type, I think it would be very helpful for all market participants. We cannot all be repo market experts, but the more transparency there is, the more we can learn about the market.

In particular, we can examine a little more about why the spikes are occurring and maybe even why the rate was set by survey one day in May.

Chris,

Your article and the history of the FHLB’s in the Money Markets makes perfect sense to any ST Rates trader and others like myself that came from the IDB side. Good job.

Fatastic post Chris. Been a FHLB member forever and this info is remarkably clear and helpful.