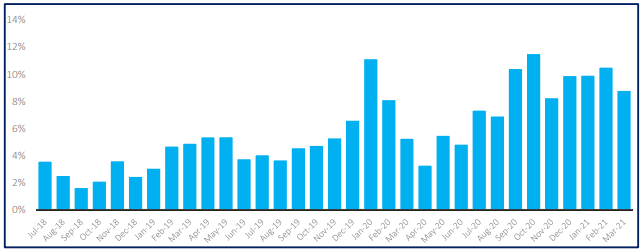

- March 2021 saw 8.8% of all derivatives risk traded versus an RFR.

- This reduced from the previous levels around 10%.

- The pre-cessation announcements last month do not appear to have accelerated RFR Adoption.

- There was an increase in the amount of IBOR-related activity last month.

- Overall for Q1 2021, the total amount of RFR activity was about the same as Q1 2020.

- We also take a look at CCP conversion plans, Open Interest and Client activity.

The latest ISDA-Clarus RFR Adoption Indicator has just been published for March 2021. It saw a decrease to 8.8%, somewhat lower than the ~10% level that it has hovered around for the past 3 months.

- The overall Adoption Indicator was at 8.8%, lower than the 10.0-10.6% readings of the prior three months.

- There were declines in the adoption of RFRs in each of the six currencies that we monitor.

- USD SOFR trading declined to 4.7% from 5.1% of the total.

- GBP SONIA trading declined from 45.8% to 44.9%. At least this has remained at relatively high levels.

- CHF and JPY (SARON and TONA RFRs) saw just 6.4% and 2.4% of overall Rates risk traded as RFRs.

LIBOR Risk Traded

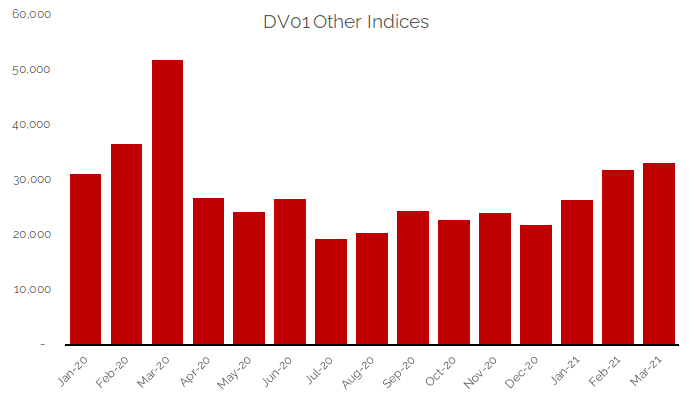

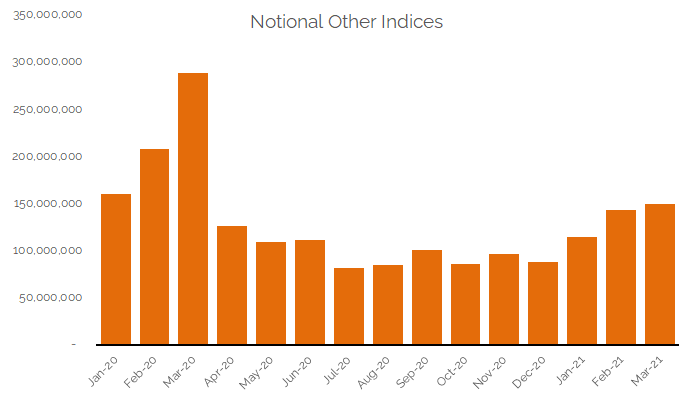

With the pre-cessation announcement last month, this blog expected a speeding-up of RFR Adoption to show in the data. Instead, we saw an increase in LIBOR and other indices traded. March 2021 saw the largest DV01 and largest notional traded in ‘IBOR type products since last March:

DV01 of IBOR-linked products:

And notional of IBOR-linked products:

It is worth noting that March 2021 is an IMM month, therefore associated with the rolling of contracts from March to June (or further out). When we look at other IMM months in our time-series, we do not typically associate these with an increase in the amount of IBOR-linked activity (despite the roll) or with a decrease in RFR activity.

RFR Risk Traded

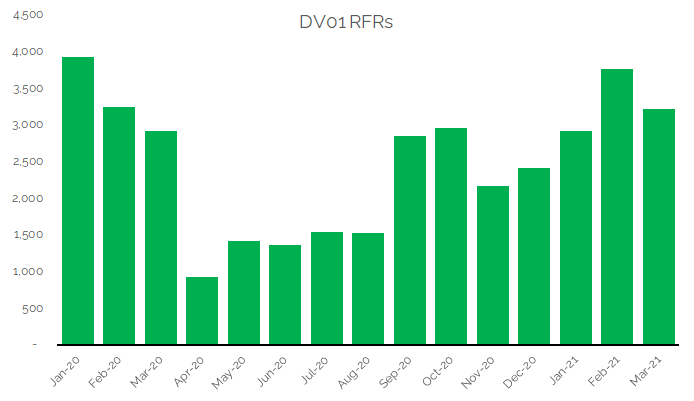

All of this increase in IBOR products was set against a decrease in DV01 traded of RFR-linked products last month:

At least the total amount of RFR risk in Q1 2021 was almost the same as Q1 2020 (within 2%).

For RFR-specific markets, we saw:

- A near-record amount of SOFR DV01 transacted at $954m. This was up by 6% compared to last month and only bettered by the “big bang” month of October 2020.

- A record amount of futures (ETD) RFR risk traded. It was over $1bn DV01 for the second month running (across all currencies).

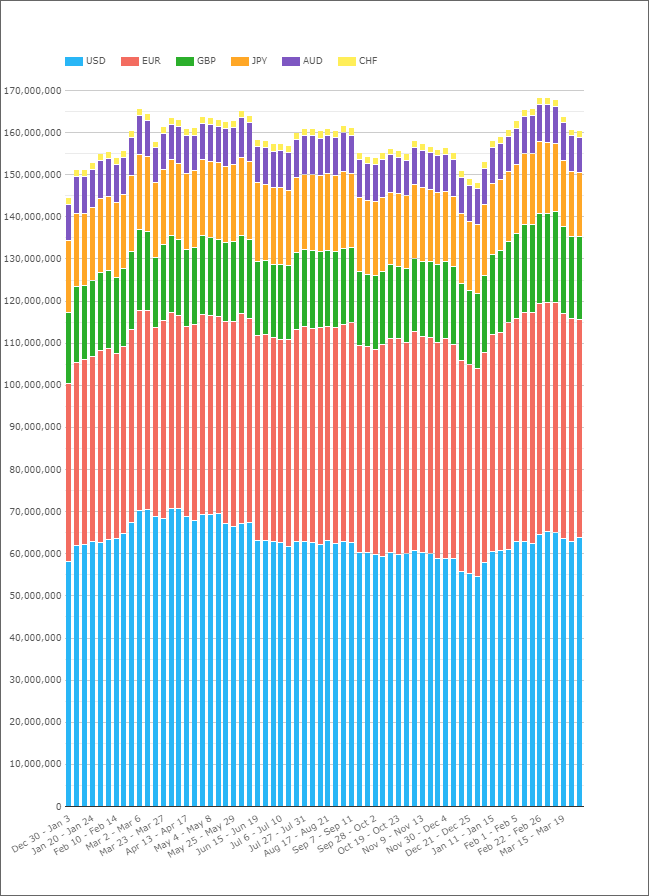

LIBOR Open Interest

Recall that the RFR Adoption Indicator monitors new trading activity in the month. You can read about the full Indicator construction in the white paper here. Therefore it is worth checking how open interest at CCPs has developed recently in IBOR-linked products. With a quarter-end included, we are used to seeing a reduction in notional outstanding:

Showing;

- Oh dear, notional outstanding of IBOR-linked products now stands at roughly $160 TRILLION.

- This is higher than year end 2020, and roughly the same as the $161-163Trn we saw in the same weeks last year.

There was part of me that hoped the increase in IBOR-linked activity we saw last month was due to risk-offsetting trades in LIBOR, that would result in reduced open interest once compression had taken effect.

Unfortunately, the data does not back this up. It looks like much of the IBOR activity was new trade activity, not risk-reducing activity related to legacy positions.

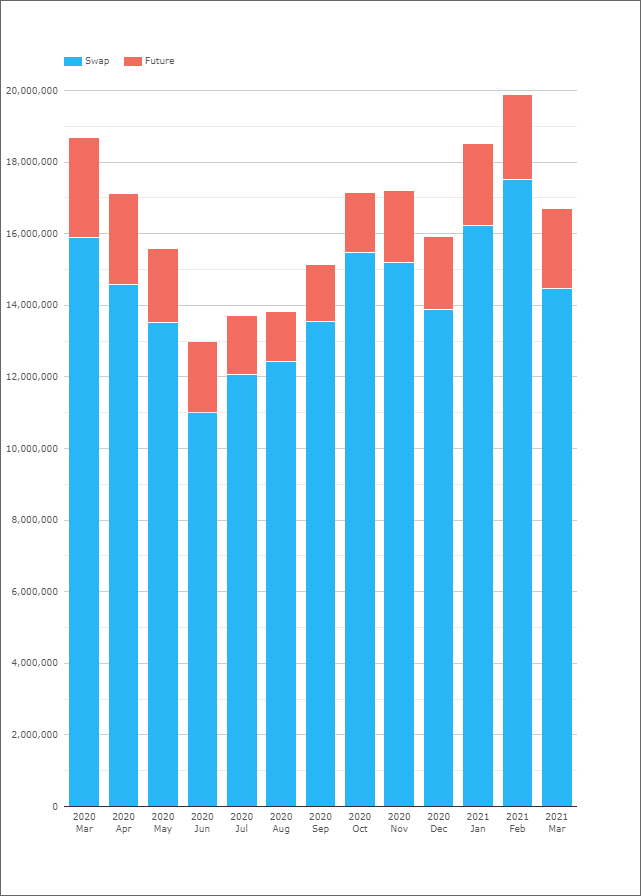

Where is the Client RFR risk?

Looking at the Open Interest in OIS we have seen a reduction in Client-related open interest in OIS across the six currencies:

And across all of the RFRs, there has been a reduction in Open Interest in Swaps whilst Open Interest in Futures has stayed constant:

CCP Conversion Plans

LCH has recently announced that any outstanding LIBOR trades (excluding USD) will be converted later this year to vanilla RFR trades (plus historic spreads as calibrated by ISDA). This means that the trades will not use the ISDA Fallbacks.

From their most recent circular, the applicable dates for RFR conversion of existing LIBOR trades are:

- 3rd December for CHF and JPY.

- 17th December for GBP.

Interestingly;

- Conversion will not be free. I assume to encourage market participants to voluntarily convert ahead of time, there will be a fee applied. The fees have not yet been made public.

- From 30th September, there will also be a monthly fee of £5 per contract applied to all outstanding CHF, GBP and JPY LIBOR contracts.

Full details are here. CME have also just published a proposal today, that includes the very same dates.

I do not know how significant the fees will be at LCH or whether other CCPs will also charge.

However, given the data for March, is there an argument to be made that bilateral LIBOR risk will find its way into clearing to access these conversion services? A back-to-back LIBOR in bilateral space versus LIBOR in clearing would at least move the LIBOR conversion into vanilla RFR products. However, we will also see changes in IM etc associated with this.

One to keep an eye on in the data…..