Clarus CCPView has daily volume and open interest data published by each CCP, which is filtered, normalised and aggregated to allow meaningful comparisons of volumes.

Today we look at 1Q23 Volume and market share in IRD for:

- USD Swaps (LIBOR, OIS, SOFR)

- EUR Swaps (EURIBOR, OIS, €STR)

- GBP Swaps (SONIA)

- JPY Swaps (TONA)

- AUD Swaps (BBSW, AONIA)

- CAD Swaps (IBOR, CORRA)

- EMEA Swaps

- AsiaPac Swaps

- LatAm Swaps

- Cross Currency Swaps

Onto the charts, data and details.

Volumes and Market Share

For major currencies and regions, vanilla swaps referencing IBORs and OIS Swaps referencing RFRs, using single-sided gross notional volume over a period; either a month, quarter or year.

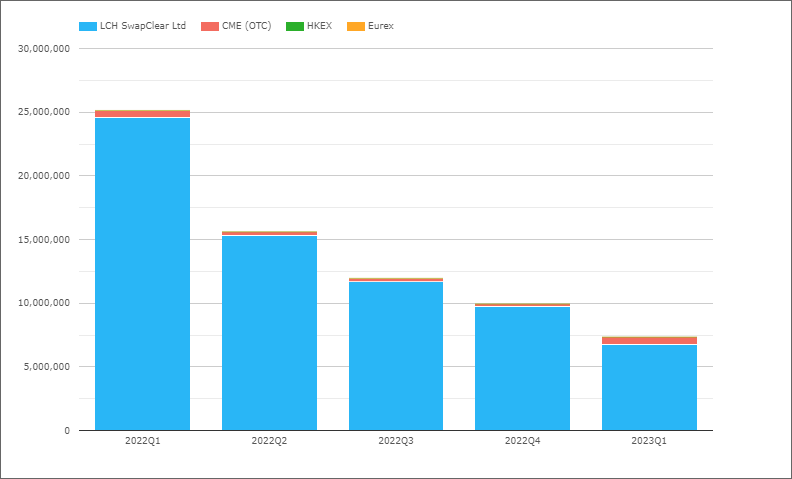

USD Swaps (Libor)

- The trend we would expect as USD Libor comes to an end in June 2023

- 2023Q1 with just $7.35 trillion compared to $25.1 trillion in 2022Q1

- And a chunk of this is $7 trillion islikely to be SPS (single-period swaps) used instead of FRAs for legacy portfolio rate reset management

- LCH SwapClear with $6.7 trillion in 2023Q1

- CME OTC with $616 billion in 2023Q1, with what looks like >$200 billion compression run volume on 24-March, which we have not yet adjusted for (as we usually do)

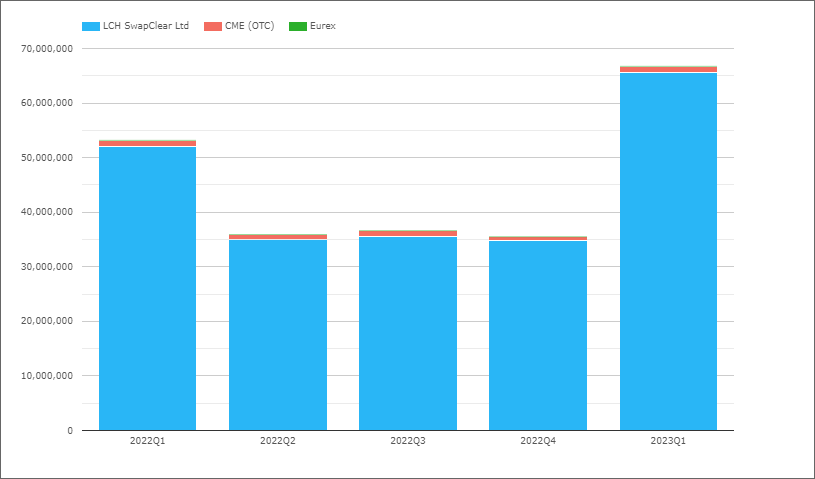

USD OIS (All)

Referencing Fed Funds and SOFR.

- 2023Q1 with $66.8 trillion compared to $53 trillion in 2022Q1

- LCH SwapClear with $65.6 trillion in 2023Q1 and $52 trillion in 2022Q1

- CME OTC with $1.15 trillion in 2023Q1 and $1.1 trillion in 2022Q1

- 2023Q1 Share is LCH 98.3% and CME 1.7%, compared to 97.9% v 2.1% in 2022Q1

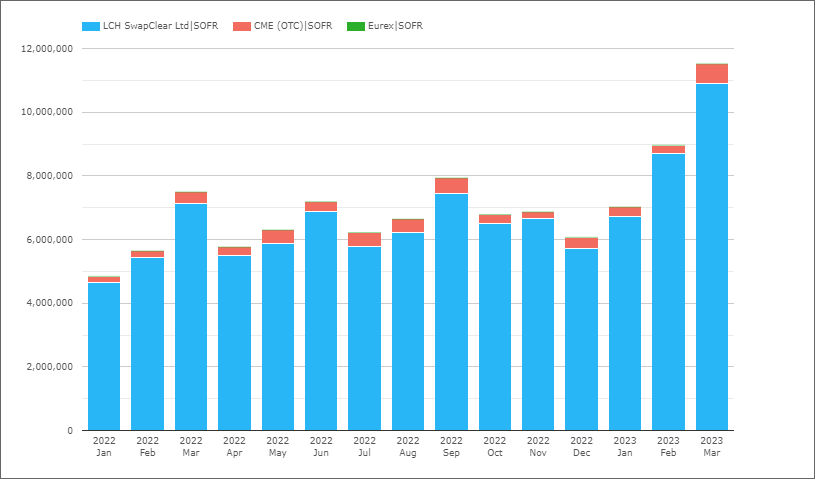

USD Swaps (SOFR)

Next isolating Swaps that reference SOFR, either OIS or Basis, volumes by month.

- Mar 2023 with $11.5 trillion is the highest ever month

- (Prior highs were Feb 2023, Sep 2022 and Mar 2022)

- 2023Q1 with $27.5 trillion, is up from $19.7 trillion in the prior quarter

- Strong increasing volume trends in SOFR volumes

- SOFR volume is 42% of the total OIS volume in the latest quarter, implying a big quarter for Fedfund Swap as in 2022Q3 the same ratio was 56%

- 2023Q1 Share is LCH 95.6% and CME 4.4%, the same share as in 2022Q1

That’s all for USD for today.

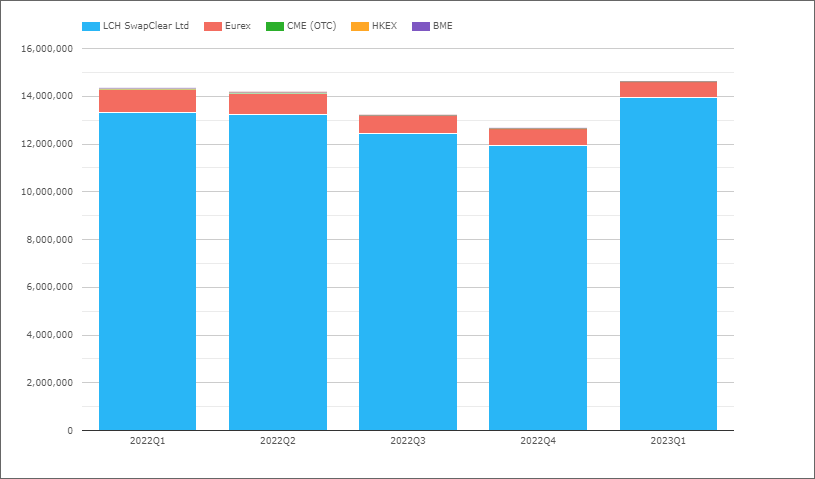

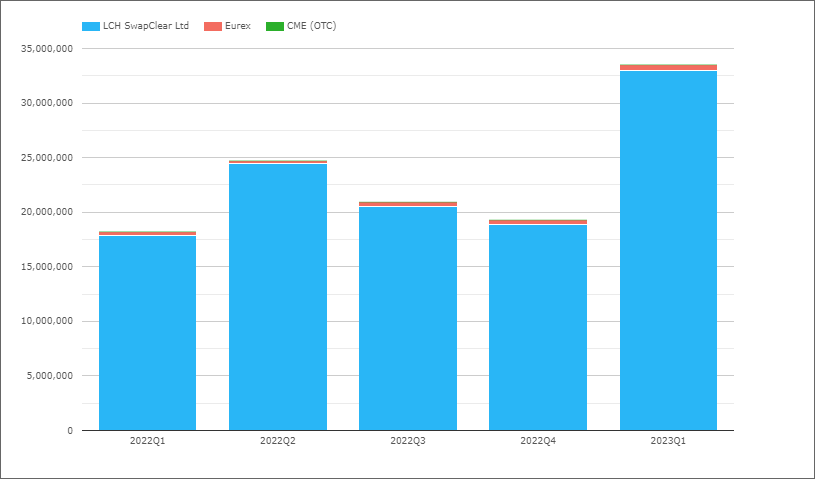

EUR Swaps (Euribor)

- 2023Q1 with €14.6 trillion compared to €14.3 trillion in 2022Q1

- LCH SwapClear with €14 trillion in 2023Q1 and €13.3 trillion in 2022Q1

- Eurex with €0.66 trillion in 2023Q1 and €0.96 trillion in 2022Q1

- 2023Q1 market share is LCH 95.4%, Eurex 4.5%

- While 2022Q1 share was 93.3% and 6.7% respectively

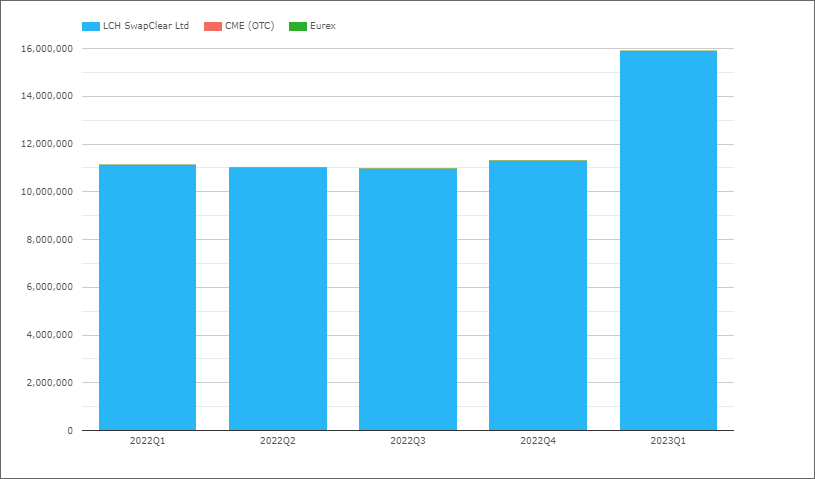

EUR OIS (All)

Referencing either EONIA or €STR, though in recent quarters all should be €STR.

- 2023Q1 with €33.5 trillion compared to €18.2 trillion in 2022Q1, an 85% increase

- LCH SwapClear with €33 trillion in 2023Q1 and €17.9 trillion in 2022Q1

- Eurex with €0.56 trillion in 2023Q1 and €0.34 trillion in 2022Q1

- 2023Q1 market share is LCH 98.3%, Eurex 1.7%

- While 2022Q1 share was 98.2% and 1.8% respectively

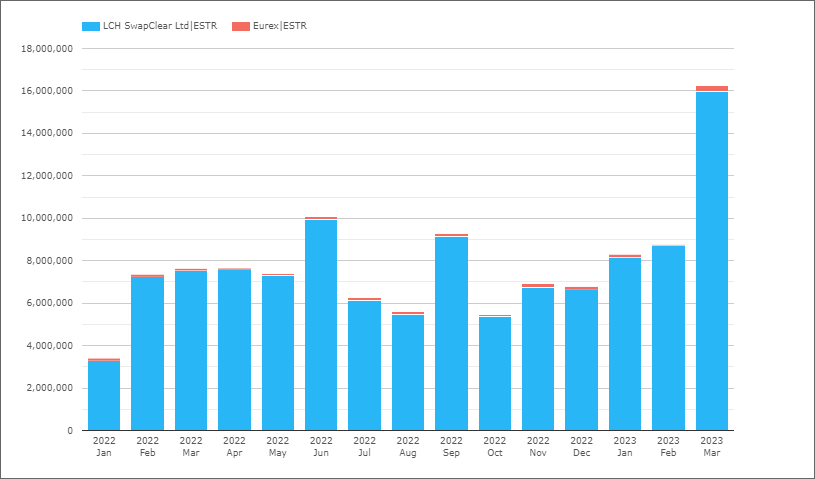

EUR Swaps (€STR)

Next isolating Swaps that reference €STR, either OIS or Basis.

- Mar 2023 volume of €16.2 trillion is a record month (prior high was €10.1 trillion in Jun 2022)

- Volumes from Jan 2023 onwards > €8 trillion each month

- 2023Q1 with €33.3 trillion, up from €18.4 trillion in 2022Q1

- 2023Q1 Share is LCH 98% and Eurex 2%, similar to 2022Q1

GBP OIS (SONIA)

- 2023Q1 with £15.9 trillion, the highest quarter since 2020Q1 (not shown) with £18 trillion

- Prior quarters in 2022, each close to £11 trillion, so a 64% increase in 2023Q1

- LCH SwapClear with 99.9% share

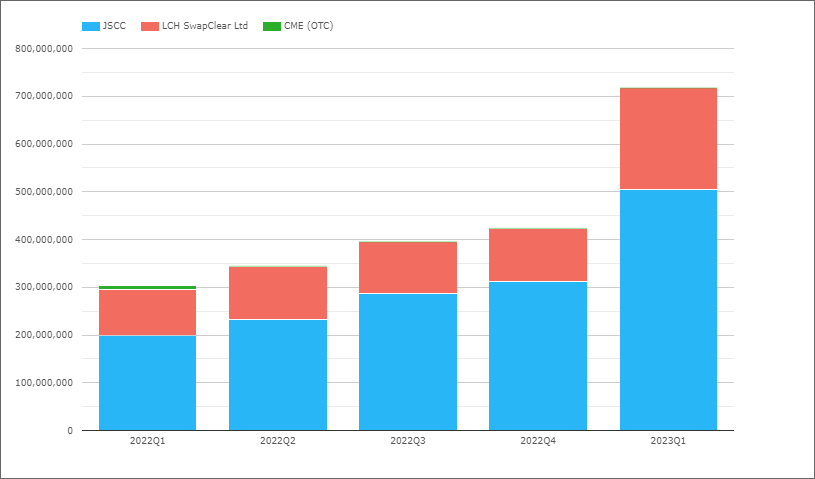

JPY OIS (TONA)

- 2023Q1 with Y718 trillion compared to Y303 trillion in 2022Q1, a 137% increase

- A spectacular increase and higher than the 85% we saw in EUR OIS above

- JSCC with Y504 trillion in 2023Q1, compared to Y200 trillion in 2022Q1

- LCH SwapClear with Y213 trillion in 2023Q1, compared to Y96 trillion in 2022Q1

- CME OTC with Y85 billion in 2023Q1

- 2023Q1 Share is JSCC 70.3%, LCH 29.7%, compared to 66% and 31.8% in 2022Q1

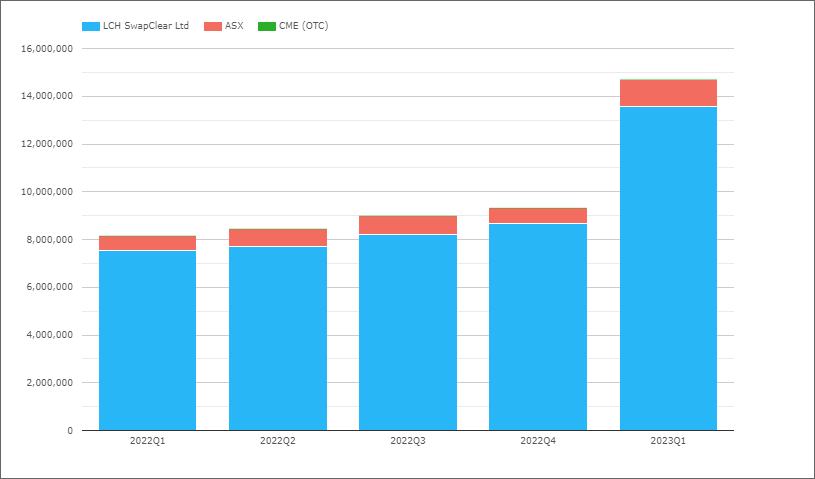

AUD Swaps

As Australia is a multi-rate jurisdiction with both AONIA and BBSW, we will chart both OIS and IRS products together.

- 2023Q1 with A$14.7 trillion, compared to A$8.2 trillion in 2022Q1

- LCH SwapClear with A$13.6 trillion in 2023Q1 and A$7.5 trillion in 2022Q1

- ASX with A$1.1 trillion in 2023Q1 and A$0.63 trillion in 2022Q1

- 2023Q1 Share is LCH 92.3% and ASX 7.7%, the same as in 2022Q1

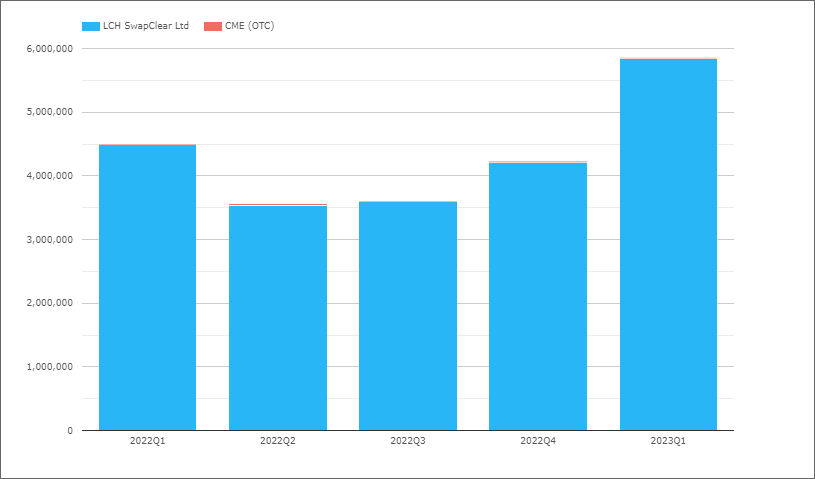

CAD Swaps (IBOR)

Canada is also a multi-rate jurisdiction with both CORRA and CDOR, so we will chart both OIS and IRS products together.

- 2023Q1 with C$5.85 trillion, compared to C$4.5 trillion in 2022Q1

- LCH SwapClear with 99.9% of the volume in the recent quarter

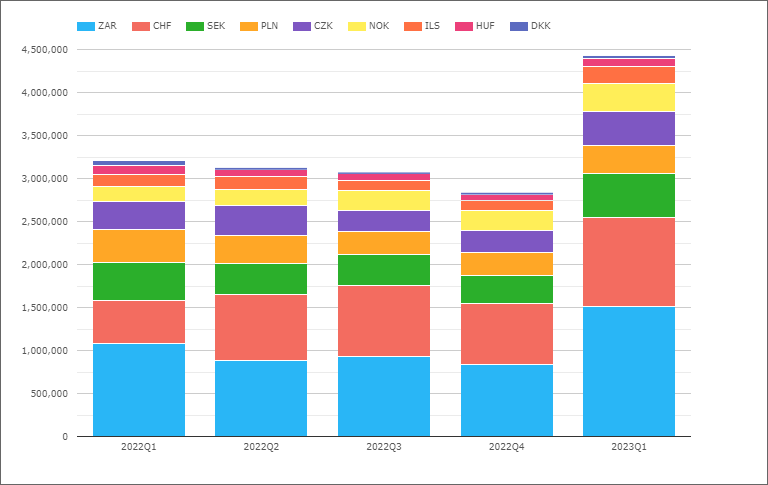

EMEA Swaps

Now let’s switch to EMEA Swaps (all types) and volumes by currency.

- A jump to $4.4 trillion in 2023Q1 from the $3 trillon level in prior quarters, so up 50%

- ZAR the largest in 2023Q1 with $1.5 trillion, up from $1.1 trillion in 2022Q1

- CHF next with $1 trillion, up from $490 billion in 2022Q1

- SEK with $505 billion, up from $440 billion a year earlier

- CZK with $400 billion, up from $325 billion

- PLN with $330 billion, down from $385 billion

- NOK with $325 billion, up from $175 billion

- ILS with $200 billion, up from $136 billion

- HUF with $98 billion, down from $109 billion

- DKK with $29 billion, down from $53 billion

Volumes up significantly in the majority of currencies from a year earlier.

Not shown in the chart is market share by CCP, where LCH has >98% share for the whole period in every currency except for:

- PLN, LCH with 95%, KDPW 2.9%, CME 2.1%

- SEK, LCH with 96.8%, Nasdaq OMX with 3.2%

- HUF, LCH with 97%, CME with 3%

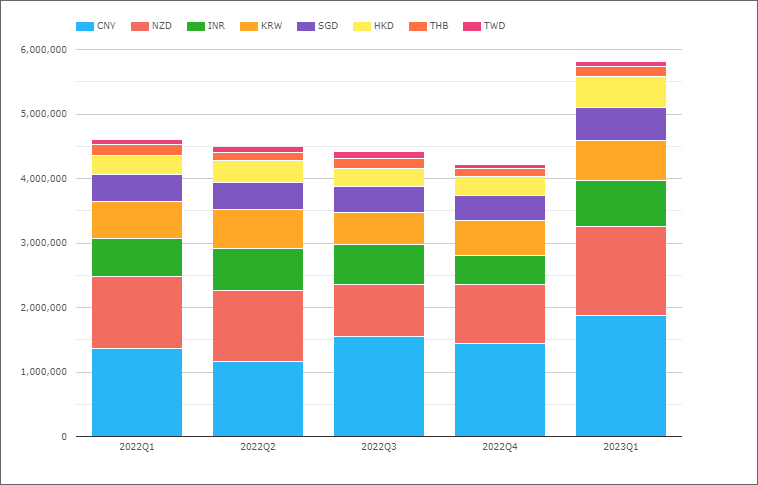

AsiaPac Swaps

Now let’s switch to AsiaPac Swaps (all types) and volumes by currency.

- A jump to $5.8 trillion in 2023Q1 from the $4.5 trillon level in prior quarters

- So materially larger than the $4.4 trillion for EMEA

- CNY the largest in 2023Q1 with $1.9 trillion, up from $1.4 trillion in 2022Q1

- NZD next with $1.38 trillion, up from $1.1 trillion

- INR with $715 billion, up from $590 billion

- KRW with $615 billion, up from $565 billion

- SGD with $520 billion, up from $425 billion

- HKD with $470 billion, up from $285 billion

- THB with $160 billion, similar to $165 billion a year earlier

- TWD with $85 billion, the same as a year earlier

Not shown in the chart is market share by CCP, where LCH has 100% share for the whole period in every currency except for:

- CNY, Shanghai with 56.8%, LCH with 43%, HKEX 0.2%

- INR, LCH with 62.6%, CCIL with 37.4%

- HKD, LCH with 97.9%, HKEX with 1.6%, CME with 0.5%

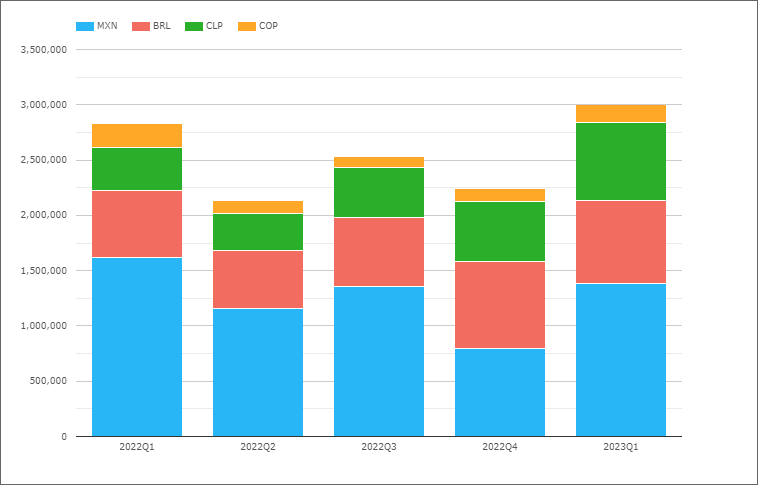

LatAm Swaps

Next lets look at LatAm Swaps.

- 2023Q1 with $3 trillion, up from prior quarters, while 2022Q1 was $2.8 trillion

- So lower than both EMEA or LatAm

- But then only 4 countries represented compared to 9 and 8

- MXN the largest in 2023Q1 with $1.38 trillion, down from $1.6 trillion in 2022Q1

- BRL next with $750 billion, up from $605 billion

- CLP with $710 billion, up from $390 billion

- COP with $165 billion, down from $210 billion

Not shown in the chart is market share by CCP, where for the whole period the share is:

- MXN, CME with 89.2%, Asigna/Mexder 8.9%, LCH 1.9%

- BRL, CME 98.9%, LCH 1.1%

- CLP, CME 98.7%, LCH 1.3%

- COP, CME 98.5%, LCH 1.5%

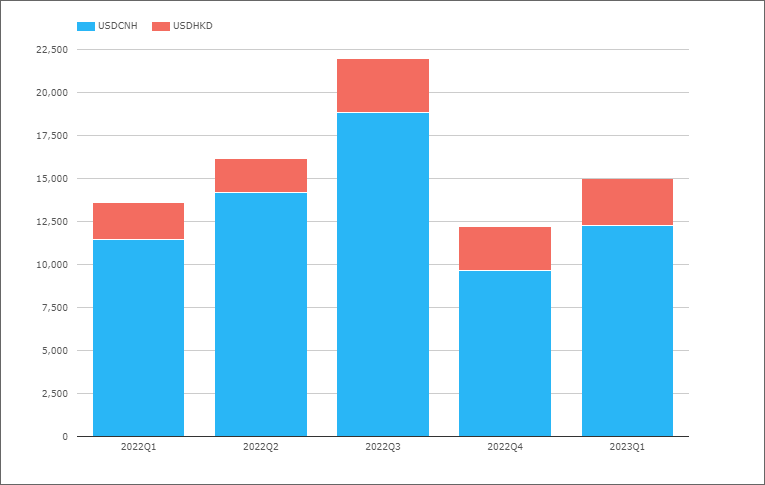

Cross Currency Swaps

HKEX the only CCP with cleared Cross Currency Swap volumes.

- 2023Q1 with $15 billion, similar to the $14 billion in 2022Q1

- Most volume in USDCNH and some in USDHKD

LCH SwapAgent does not clear XCCY Swaps, but offers processing, margining and settlement of bi-lateral for these. Volumes are not available regularily, but we know from a recent LCH press release that SwapAgent registered record volumes in of $2.7 trillion (double-sided) notional in 2022.

That’s It

14 Charts for an overview.

Still a lot more data to look at

Volume, DV01 and Open Interest by currency.

IR Futures in all the major currencies and US Treasury volumes.

Credit Derivatives and FX Derivatives.

For more details, please contact us for a CCPView demonstration.