US Election Live – What is Trading?

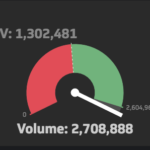

USD Swap curve steepens and volumes massively up, > 5X the average in some tenors. We will follow what is trading in Interest Rate Derivatives markets throughout the day Stay up-to-date by manually refreshing the page today 16:15 New York – Wrapping up for the Day While the Stock Market has been subdued today with […]

October 2016 Swaps Review

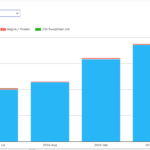

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in October 2016. First the highlights: On SEF USD IRS volume in October at >$1.6 trillion was 12% lower than September SEF Compression activity was $200 billion in USD IRS, same as prior month USD OIS volume at >$1.76 trillion was down from >$2.4 trillion But USD OIS […]

クリアード・スワップの証拠金に係るバッファーの見積もり

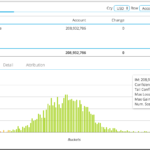

中央清算機関(CCP)とクリアリング・メンバー(メンバー)との間で行われる、或いはメンバーとクライアントで行われる、日々の変動証拠金(VM)のフローはかなり大きなものとなっている。例えば、LCHの公表しているCPMI-IOSCO Disclosuresは、メンバーからCCPに支払われる1日の変動証拠金の総額は160億ドル!となっている。

FRTB – The Default Risk Charge

Following on from my articles, Fundamental Review of the Trading Book and Internal Models or Standardised Approach, I wanted to take a look at a specific component of the Market Risk Capital, namely the Default Risk Charge as required under the Standardised Approach. Background In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum […]

Two Month Update: Uncleared Margin Rules & Swap Data

Over the past 2 months, my colleagues and I have occasionally studied swaps data for hints of impacts from the September 1 implementation of Uncleared Margin Rules (UMR) effecting behaviors. There have been a few general themes: Uptick in NDF Clearing Uptick in Inflation Swap Clearing No notable effect on Swaptions Now with 2 months […]

BRL NDF Market – 30% of Dealer to Dealer flow is now cleared

We look at the USDBRL market in the latest in a series of NDF blogs Clarus data covers over 66% of the market on a trade-by-trade basis For the Dealer-to-Dealer market alone, our coverage increases to 73% Our data shows that clearing has increased from 6% to 31% of dealer-to-dealer flows. Bringing Old Blogs Up To […]