Over the past 2 months, my colleagues and I have occasionally studied swaps data for hints of impacts from the September 1 implementation of Uncleared Margin Rules (UMR) effecting behaviors. There have been a few general themes:

- Uptick in NDF Clearing

- Uptick in Inflation Swap Clearing

- No notable effect on Swaptions

Now with 2 months under our belt, let’s take a refreshed look at the data and update our initial research done on Sep 14. I also want to add single name CDS into the mix.

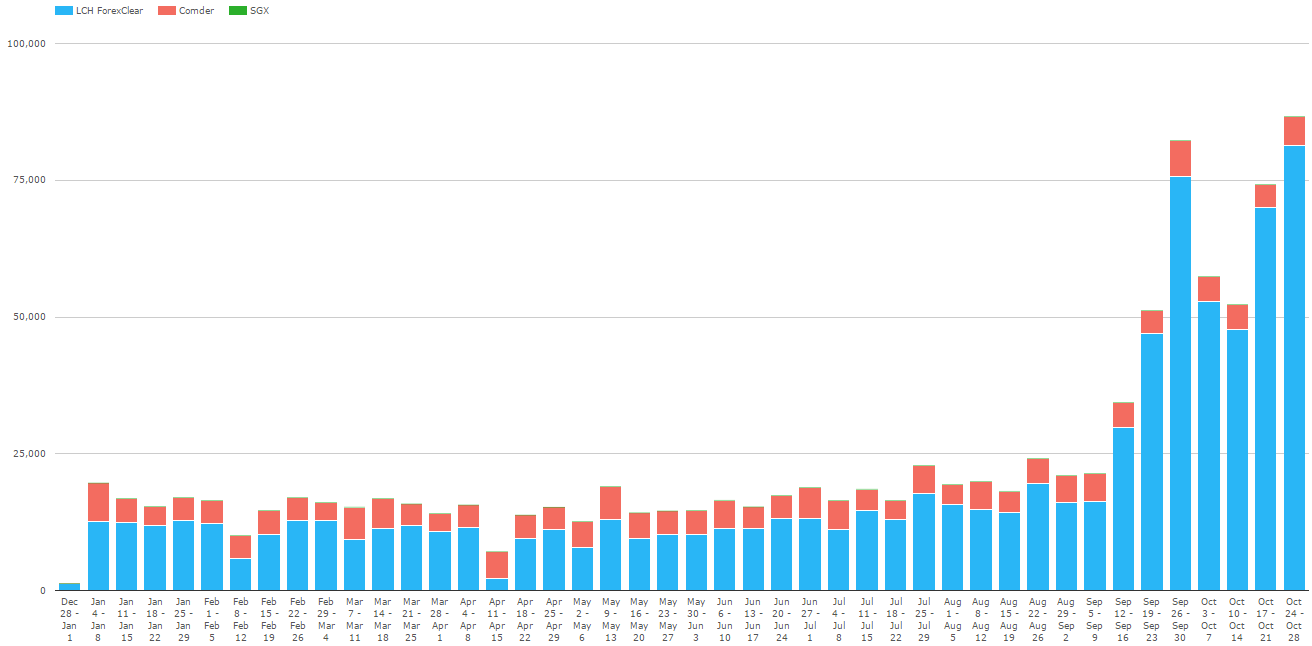

NDF

Let’s start with NDF, where we have given some good attention to over the past month.

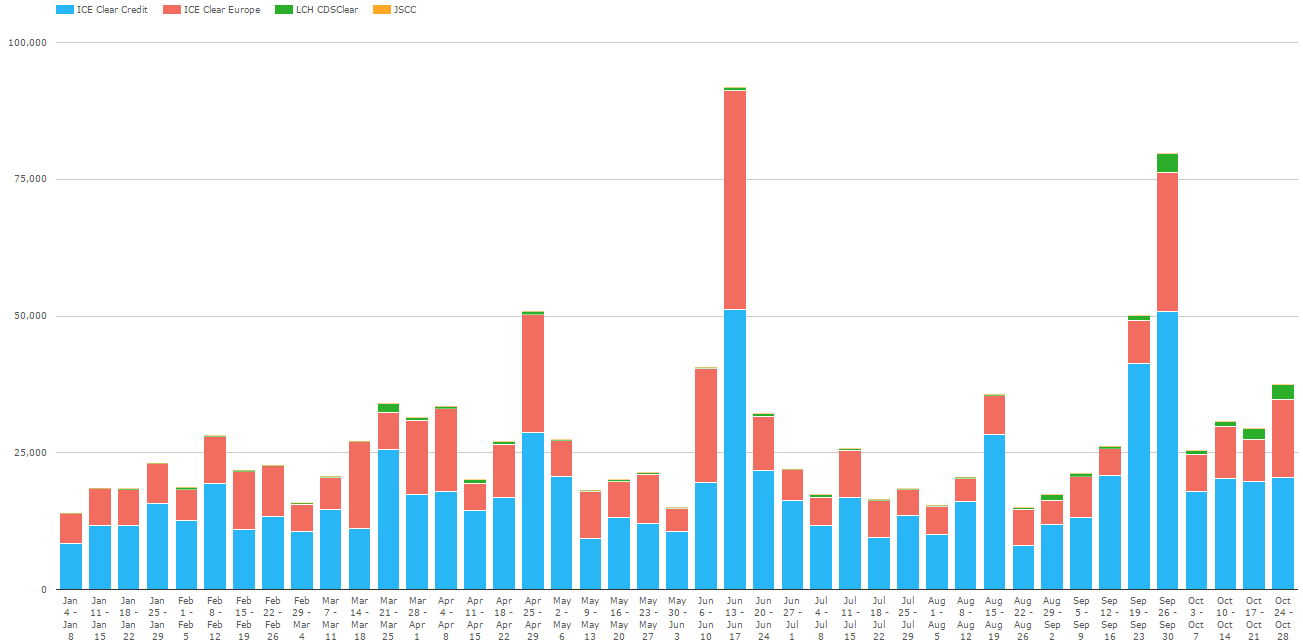

First, clearing activity by clearinghouse:

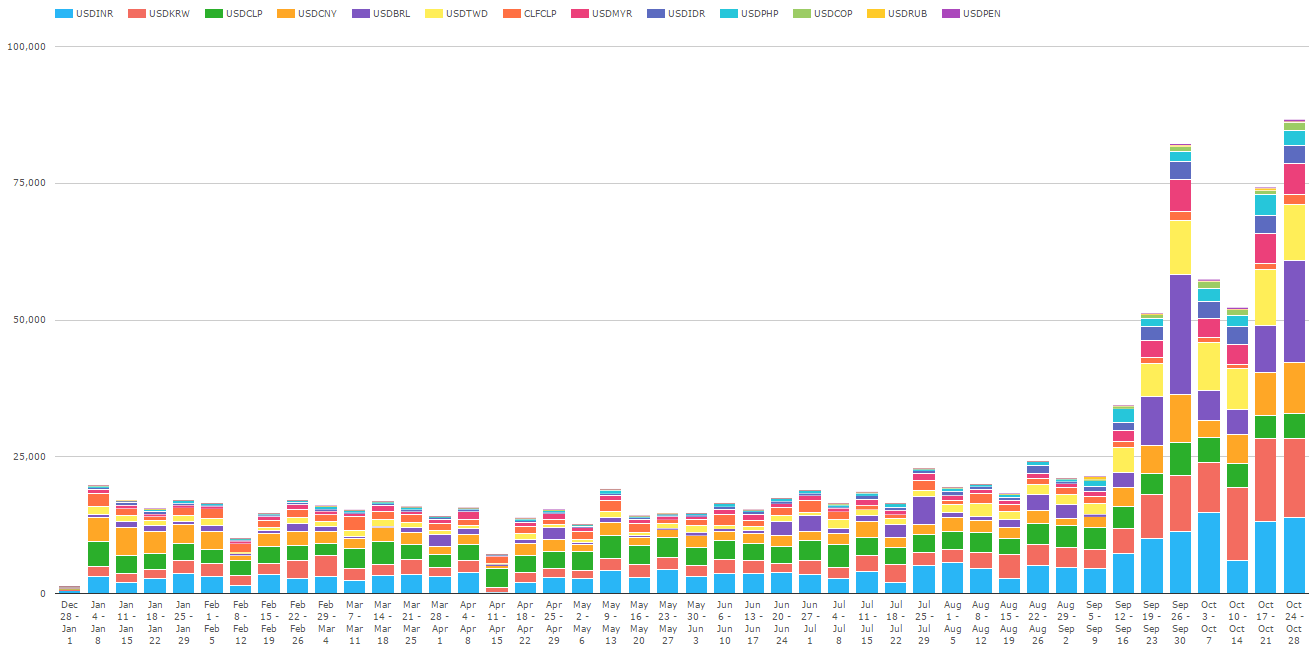

Then NDF volume by CcyPair:

Chris explored NDF’s in greater detail earlier in October in his blog, and singles out BRL in his blog today. This chart shows the trend continuing in earnest.

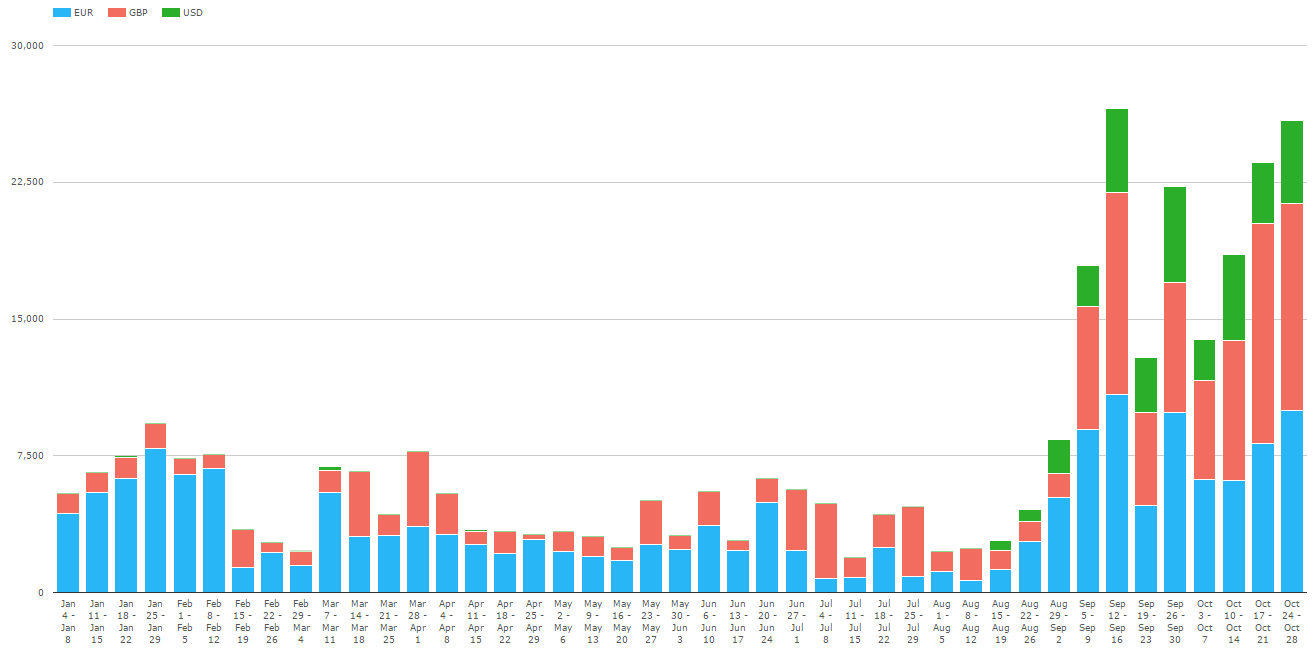

INFLATION

All cleared inflation swaps are LCH cleared at the moment, so I’ll skip the clearinghouse view and head straight to the currency view:

The uptick we saw a couple weeks into clearing has stuck around.

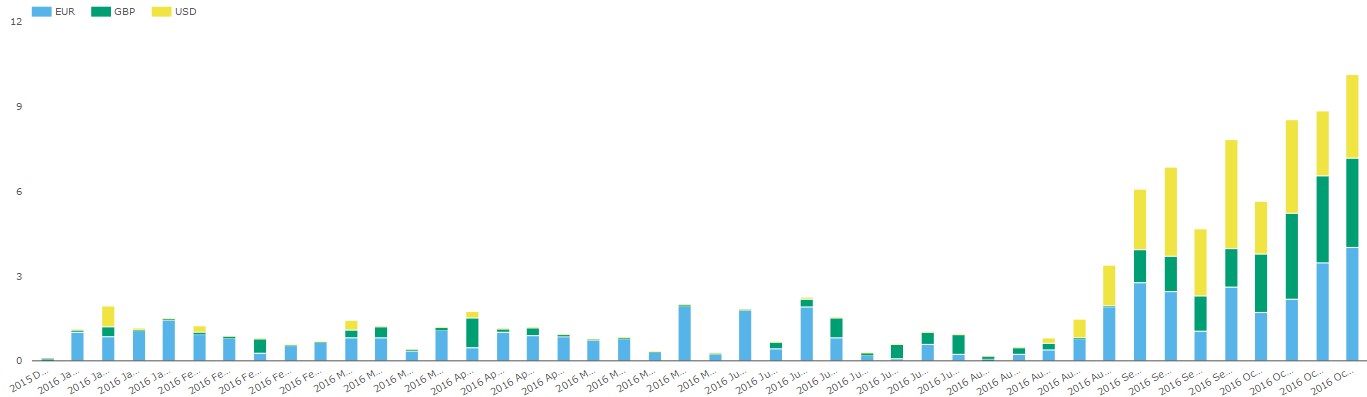

I was interested to see how much of this cleared activity is from US-business. So I turned to SDR data. Here is what we see on SDRView for EUR, GBP and USD cleared activity:

This tells us that US-named business accounts for roughly 1/3 of LCH’s cleared activity. Note that SDRView uses a different scale (billions of USD) vs CCPView (millions of USD).

And how much of the market is cleared now? By looking at just USD inflation swaps on US SDR, and including uncleared, corroborates the notion we raised last time that the majority of the inflation market is now cleared.

SWAPTIONS

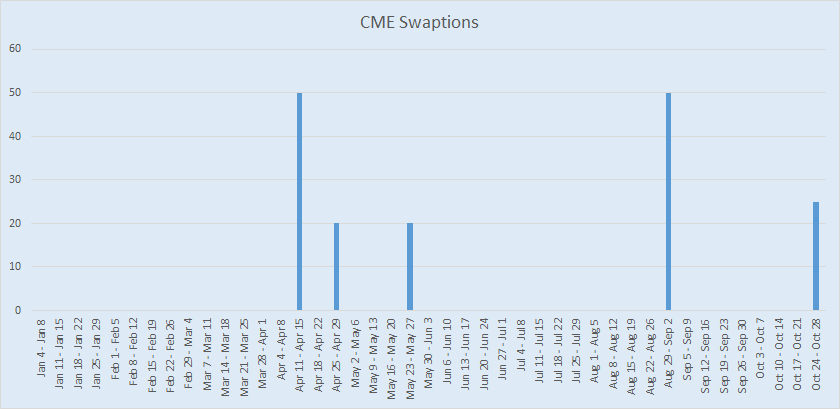

Swaptions clearing is slightly more nascent. There really has only been a smattering of activity in cleared activity since their launch earlier in the year. The Volume chart is just barely non-zero:

So swaptions still have not joined the party. However there has been recent news of more firms onboarding to swaption clearing, so it appears to still be in the infrastructure buildout phase within the industry.

CDS

This one is tricky. A few folks have asked me to look into Single Name CDS clearing activity since UMR went into effect. Let’s begin with my first instinct – observing Single name CDS (Corp and Sovereign) on CCPView:

Conclude from that what you will.

Ideally I would next go to public SDR trade data to look at clearing rates for single name CDS. Unfortunately, this does not exist yet! The SEC are making progress on SBSDR, but without that data, there is not much we can do.

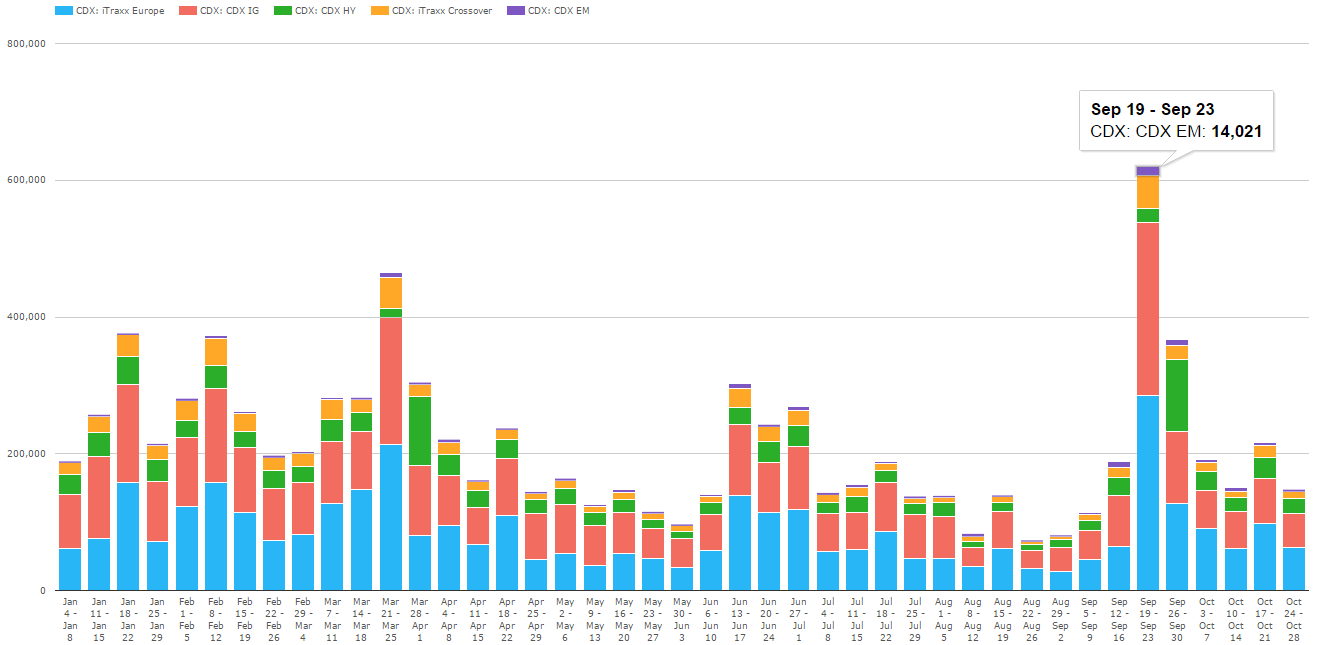

But what about non-mandatory CDS Index? Does that even still exist? It actually made me go back and check what Index products are clearing mandated. I believe it is this:

- CDX NA IG 3, 5, 7 & 10 Year Indices

- CDX NA HY 5 year Indices

- iTraxx Europe 5 & 10 year indices

- iTraxx Europe Crossover and HiVol 5 year Indices

Which frankly does not leave much else. Emerging Markets Index anyone? Here is CCPView by Index:

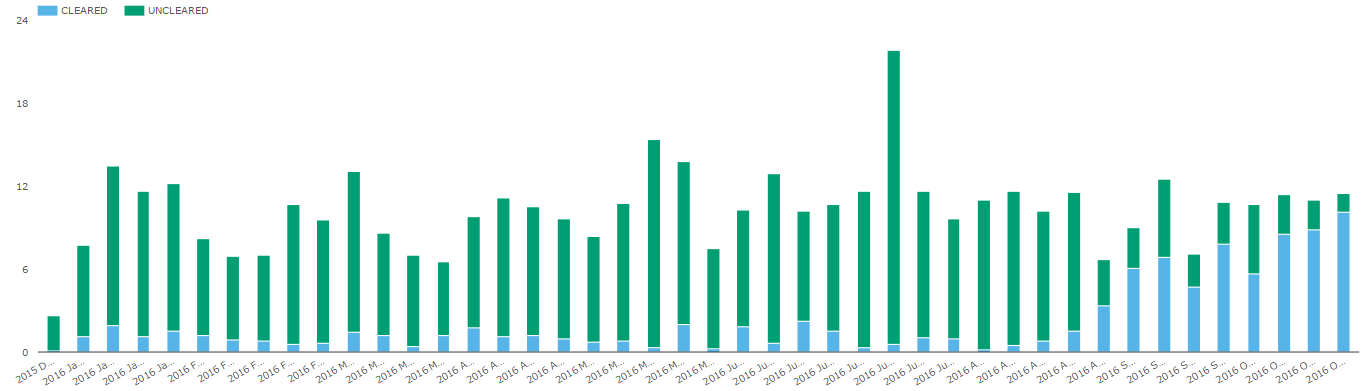

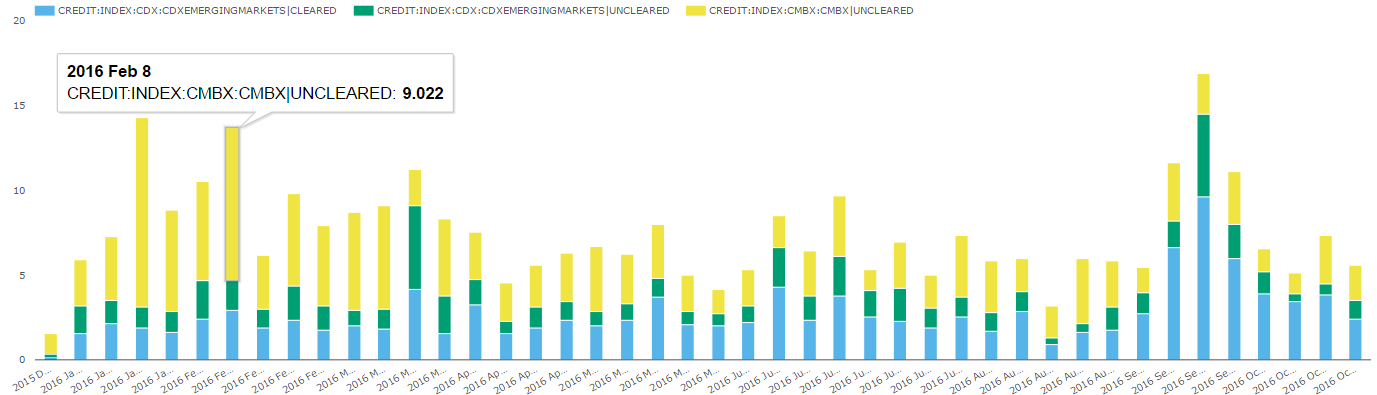

And of course SDRView has CDS Index, so lets have a look at activity in the more esoteric EM and CMBX market, split by Index and Cleared/Uncleared:

Can’t say that tells me much, except that I now understand why CME have been discussing CMBX clearing, but not a heck of a lot, maybe a few billion a week.

I feel like a CNN political fact-checker here, but if I were to deem CDS clearing being significantly impacted by Uncleared Margin Rules, I would call that FALSE!

SUMMARY

All of the trends we noted over the past couple months appear consistent:

- NDF Clearing has maintained progress

- Inflation Swap clearing has done so as well, with notable activity in USD

- Swaption clearing must be in infrastructure buildout mode, with very little to report

- CDS Clearing is tricky, but nothing obvious is happening in the products that are clearable but not mandatory cleared.