USD Swap Spreads Review Q1 2019

Swap Spreads, aka Spreadovers, have recently turned negative again in the US. They rebounded back into positive territory fairly quickly. This is against a background of all-time record volumes in USD swaps reported to US SDRs. Should Swap Spreads be at zero versus SOFR after LIBOR disappears? Negative Again In case you missed it, Swap […]

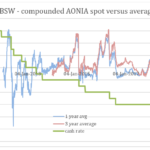

Libor Fallbacks – What will the AUD BBSW Spread be?

In his recent blog Chris looked at Libor Fallbacks and the GBP Spread, so I thought it would be interesting to look at the spread for AUD. As we know, the first amendments to the ISDA 2006 Definitions are expected in 3rd quarter of 2019 and include fallback changes for GBP, CHF, JPY and AUD. So it is timely to look at the potential spread implications for AUD BBSW, to add to the work done on the GBP Libor.