This blog looks at competition for trade volume in Q4 2025 and for the whole of 2025 between rates exchange-traded derivatives (ETD) exchanges and CCPs.

Key takeaways

In 2025, only EUR money-market (MM) futures, JPY MM futures, and USD MM futures show real competition now or potential for real competition in the future.

- Eurex reached 14.7 percent of EUR MM futures volumes in 2025 overall, gaining 3.0 percent from ICE and 0.4 percent from CME. For the first time, ICE had a majority share of the smaller but faster growing €STR futures subset.

- SGX, in its first full year of executing them, achieved 15.2 percent of JPY TONA futures volumes, gaining 1.6 percent from JPX and 8.3 percent from TFX. In Q4, JPX bounced back to its largest monthly market shares ever.

- Among other currency and product type combinations, only FMX (clearing at LCH) showed promise of soon exceeding a 1 percent market share of USD MM futures. FMX grew its monthly share of USD SOFR futures to 0.65 percent in December 2025.

Read on for more details.

Competition overview

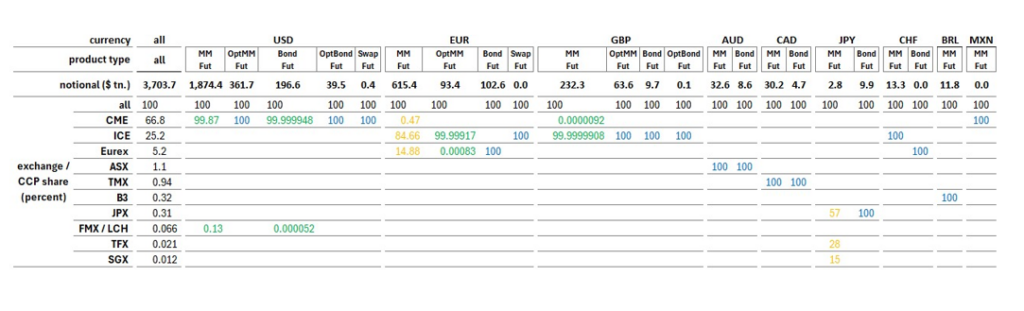

CCPView gives you exchange / CCP market shares across all currencies in a single query. I downloaded 2025 notional volumes and percentages to a spreadsheet to highlight the degree of competitiveness.

Table 1: Rates ETD 2025 trade volumes and CCP share by product type and currency (percentage of USD notional). Source: CCPView, author analysis

Each column in Table 1 shows 2025 USD notional volume and CCP shares for one combination of currency and product type. It shows that:

- Two combinations have “real competition now” with more than one material CCP market share: EUR MM futures and JPY MM futures (highlighted orange).

- Four combinations have “potential” competition with small non-zero shares at a second CCP: USD MM futures, USD bond futures, EUR options on MM futures (OptMMFut), and GBP MM futures (highlighted green).

- Each other product type in USD, EUR and JPY, and each remaining whole currency is only cleared by one CCP (highlighted blue).

For GBP MM futures, the small volume second CCP is CME. CME SONIA MM futures last traded on 02 May 2025 and traded on only five days in 2025. We exclude this from further analysis and focus on the “real” and “potential” competition cases in USD, EUR, and JPY.

We start with EUR.

EUR MM futures and options

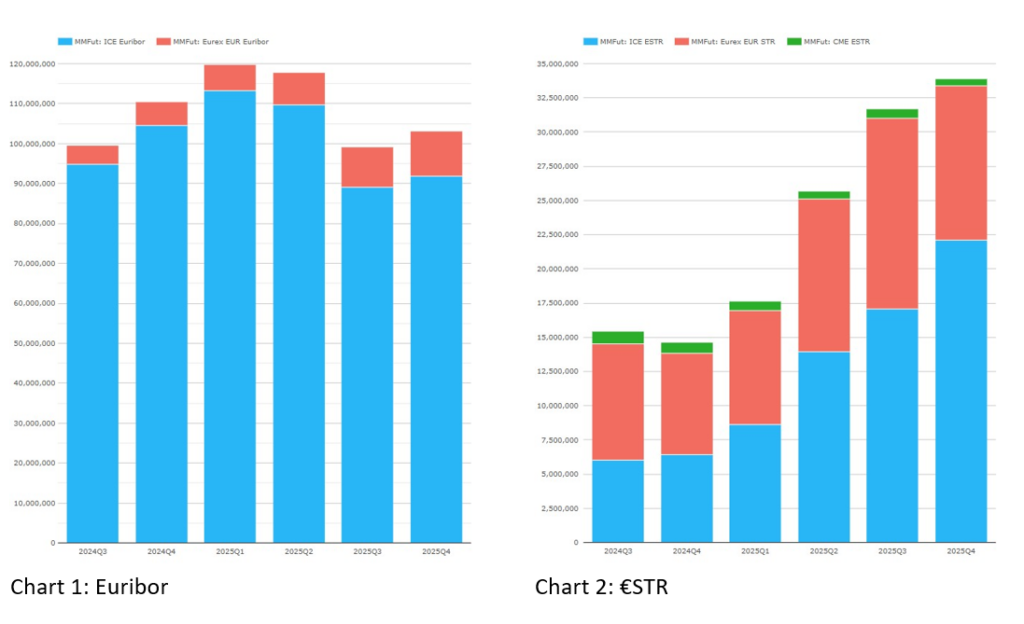

EUR MM futures is a market with RFR transition and is thus bifurcated into Euribor and ESTR futures. We can look at volumes in the two parts of the market separately.

EUR MM futures volumes split by underlying index (EUR notional). Source: CCPView

Charts 1 and 2 show the volume trend from the second half of 2024 to the end of 2025.

- Euribor futures volumes peaked at €119.7 trillion in Q1 2025 and ended the year with €103.2 trillion in Q4 — down YoY about €7.3 trillion.

- €STR futures (which only started trading in late 2022) set new volume records in each quarter of 2025 ending the year with €33.9 trillion in Q4 — up YoY about €19.2 trillion.

Will volumes of €STR futures one day overtake those of Euribor futures?

Now let us look at exchange/CCP shares.

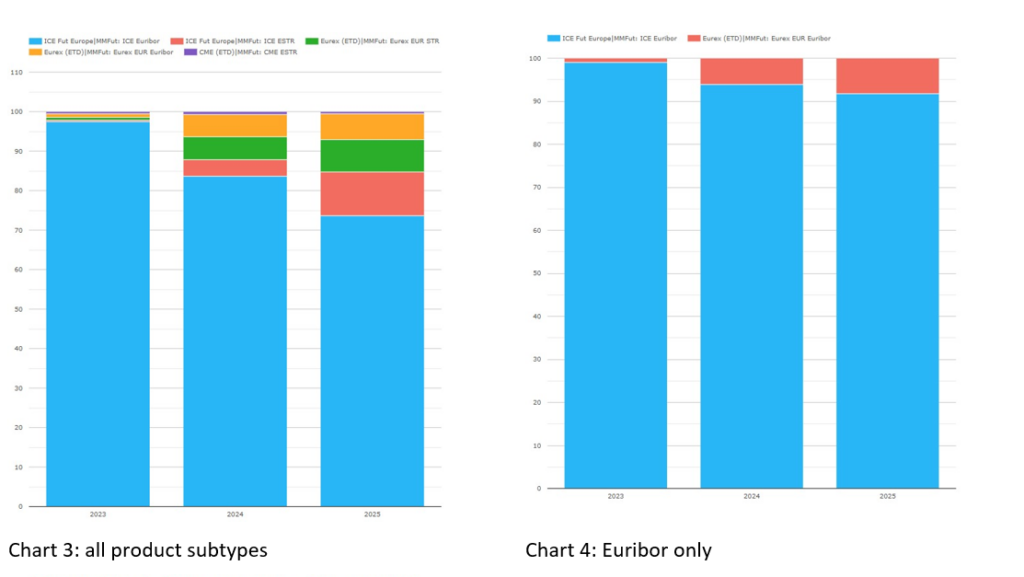

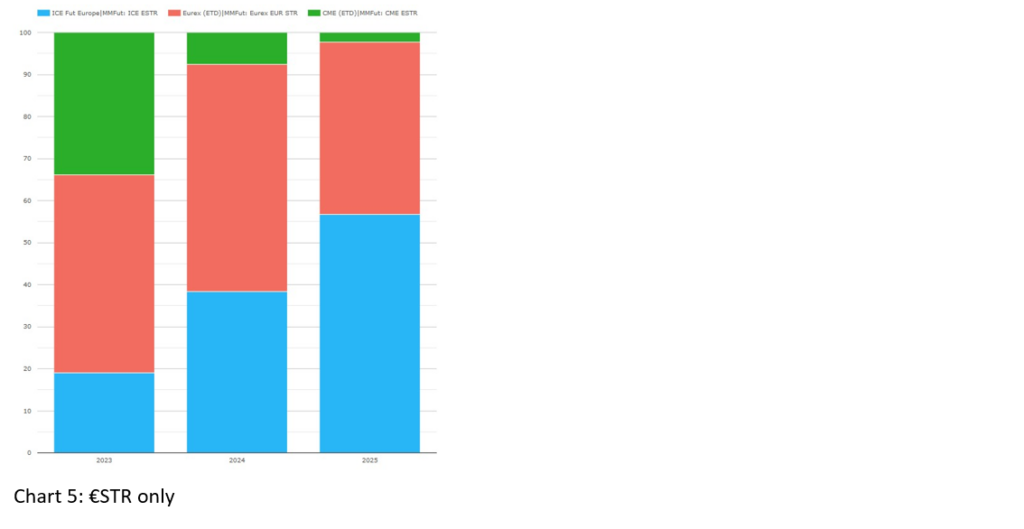

EUR MM futures volume share by CCP and product subtype (percentage of EUR notional). Source: CCPView

Charts 3, 4, and 5 show the year-on-year (YoY) dynamics overall and for Euribor and €STR individually.

- ICE had 84.8 percent of 2025 overall EUR MM futures volumes — down YoY from 87.8 percent (Chart 3). We can also see that ICE lost about 2 percent of Euribor (Chart 4) but gained about 18 percent of €STR (Chart 5), giving ICE a majority share of both markets.

- Eurex had 14.7 percent overall — up from 11.3 percent (Chart 3). We can also see that Eurex gained about 2 percent of Euribor (Chart 4) but lost about 13 percent of €STR (Chart 5).

- CME had 0.47 percent — down from 0.82 percent. We can also see that CME lost about 5 percent of €STR (Chart 5).

Overall, Eurex took 3.4 percent of EUR MM futures volumes from ICE and CME, while ICE for the first time in 2025 holds a majority of both Euribor and €STR futures.

Now we briefly cover EUR options on MM futures.

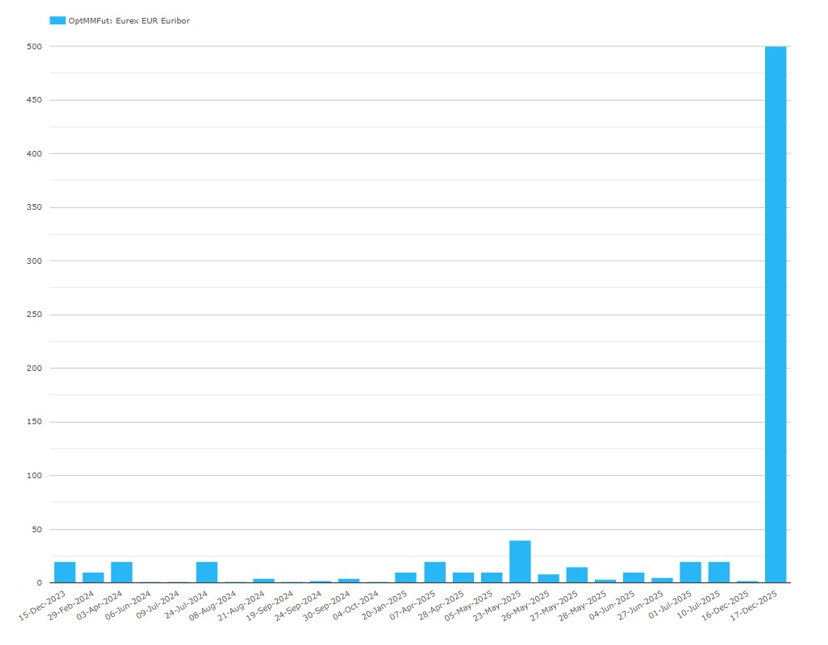

Chart 6: volumes of Eurex options on Euribor futures to the end of 2025 (EUR notional millions). Source: CCPView.

Chart 6 excludes ICE EUR MM options which dominate volumes in that product type. Thus, we see only the 26 days with non-zero Eurex EUR Euribor options activity in 2023, 2024, and 2025. In 2025, the 0.00083 percent share shown in Table 1 comprised €500 million on 17 December and €173 million on the other 13 days with activity.

Speaking of sporadic volumes, along with ICE’s large volume of Euribor options, there was a single day of €200 million ICE €STR options in 2024 but nothing in 2025.

We wonder whether €STR options or Euribor options or both will eventually become established markets.

JPY MM futures

We start with a little history.

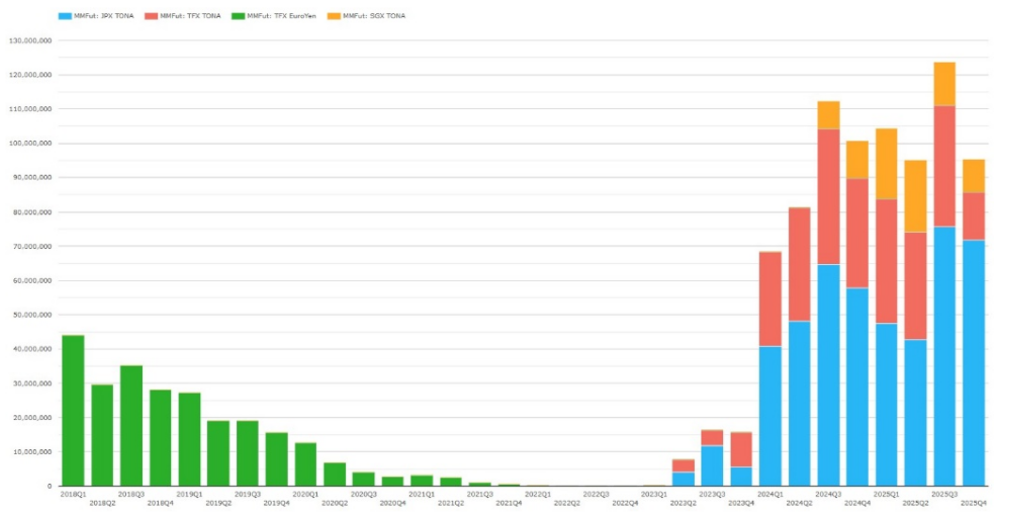

Chart 7: JPY MM futures volume share by CCP and product subtype (percentage of JPY notional). Source: CCPView

Chart 7 shows the slow decline of TFX Euroyen futures up to the cessation of JPY LIBOR at the end of 2021, then a year of no material JPY MM futures volume in 2022. This was followed by an explosion in TONA futures volume after they were introduced by TFX in March 2023, JPX in May 2023, and SGX in July 2024.

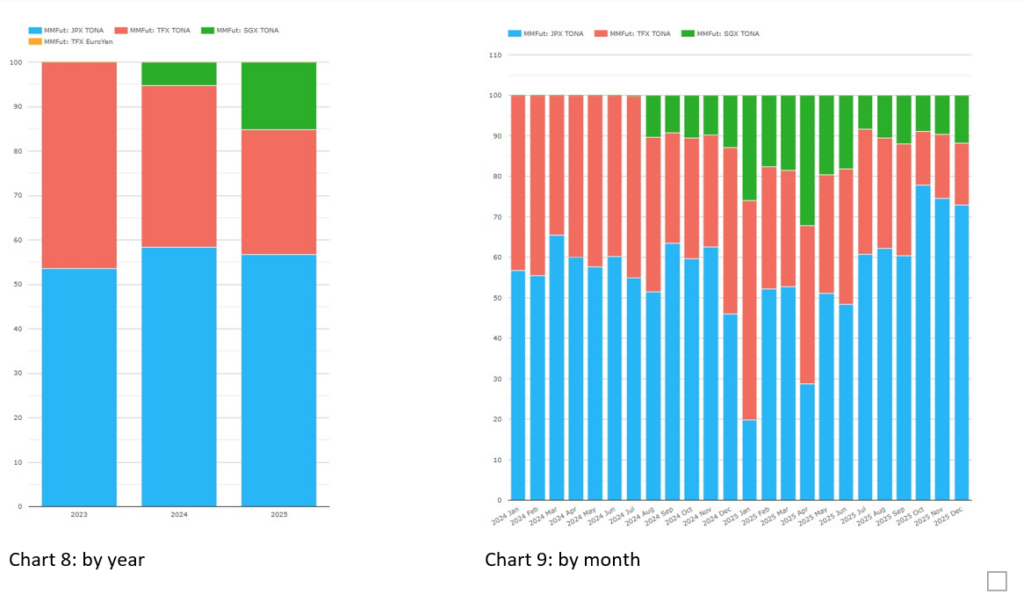

JPY MM futures volume share by CCP and product subtype (percentage of JPY notional). Source: CCPView.

Charts 8 and 9 show the ongoing competitive dynamic between JFX, TFX, and SGX for JPY TONA futures activity.

- JPX took 56.7 percent of 2025 TONA futures — down from 58.4 percent in 2024. Within the year, after losing share in Q1 and Q2 and dropping below 20 percent in January and below 30 percent in April, JPX’s monthly share exceeded 72 percent in each of the last three months of 2025, peaking at 77.8 percent in October — their highest share ever.

- TFX took 28.0 percent of 2025 TONA futures — down from 36.4 percent in 2024. Within the year, after peaking at 54 percent in January, TFX’s monthly share spent the rest of Q1 to Q3 in the 20s and 30s, before spending Q4 between 13 and 16 percent — down on Q4 2024.

- SGX took 15.2 percent of 2025 TONA futures — up from 5.3 percent in 2024, during which it was only active in the last six months. Within the year, after peaking in January at 26.0 percent and in April at 32.2 percent, SGX’s monthly share spent Q4 between 8 and 12 percent — similar levels to Q4 2024.

Given its smaller domestic SGD-based markets, SGX is naturally focused on international markets. It offers Asian, European, and American international investors the ability to trade ETD on multiple Asian markets in a single exchange with a single “margin pot”. This may avoid setup costs for the local exchange of each country and lower initial margin (IM) costs via SGX’s SPAN margin model, with its cross-currency or cross-asset class risk offsets. For example, TONA MM futures may obtain cross-margining efficiencies against JGB futures, USD JPY FX futures, and Nikkei index futures.

SGX took 15 percent of TONA futures in 2025 its first full year of trading. However, Q4 showed signs of a healthy JPX comeback.

USD MM and bond futures

We look at the progress of FMX and LCH in their attempt to take a slice of USD MM futures from CME.

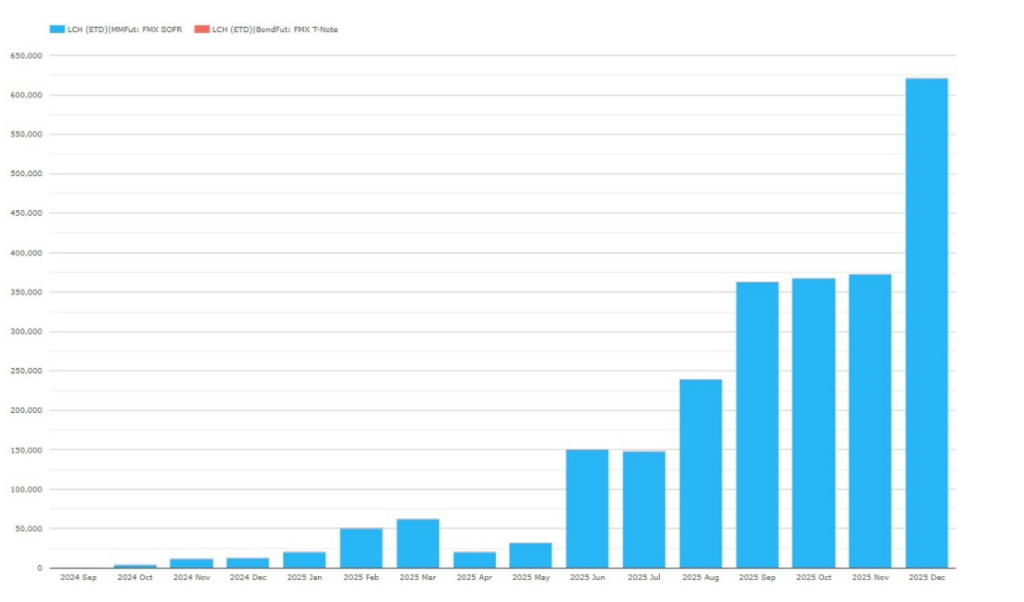

Chart 10: FMX/LCH USD MM futures volumes by product subtype (USD notional). Source: CCPView

Chart 10 shows that FXM continues to grow volume, reaching $621 billion in December 2025 – up YoY from $13 billion.

- Materially, all the FMX volume is in SOFR futures, which trade every day.

- FMX T-Note futures (included but not visible) also started trading in 2025, peaking at $54.6 million in August 2025 — trading about one day in three. This is the 0.000052 percent of USD bond futures shown in Table 1.

The 0.13 percent full-year 2025 FMX/LCH market share of USD MM futures shown in Table 1 earlier for is for all MM futures products. Let’s focus on SOFR futures alone as FMX is not currently listing FedFunds futures, which are about one third of total MM futures volumes. Also, let’s look at month-by-month market share growth.

Table 2: SOFR futures volumes share by exchange/CCP (percentage of USD notional). Source: CCPView

Table 2 shows that FMX had 0.20 percent of 2025 SOFR futures (higher than the 0.13 percent of all USD MM futures due to the exclusion of FedFunds futures, which FMX is not yet listing), while monthly shares reached 0.65 percent in December.

With such exponential growth, each new quarter brings real news, so it is hard to speculate where or when market shares will settle down. Nonetheless, it looks like FMX will get above 1 percent of SOFR futures soon.

That’s it

Flip back to the top to recap the takeaways.

The volumes in CCPView cover many more cleared instruments, metrics, and analysis parameters.

- Cleared instruments also include interest rate swaps, other asset class futures and options, and cash US Treasuries.

- Volume metrics also include new trade count / DV01 / average daily volume (ADV), open interest (OI), OI change, and notional unwound/matured.

- Analysis parameters also include date / week / month / year, exchange, product subtype, tenor, and activity type (D2C or D2D trade).

For more details, please contact us for a CCPView demonstration.