It is almost two years since I wrote about the Final US Rules on Margin for Non-Cleared Swaps. How time flies and since then we have seen implementation of this rule in the US and equivalent rules and regulations in many other jurisdictions.

Today I will look at the Australian regulation recently made final by APRA as “Prudential Standard CPS 226 Margining and risk mitigation for non-centrally cleared derivatives”. This is effective from September 1, 2017 and follows a consultation period and a draft published in October 2016.

The final prudential standard document is available here, the full 27 pages; which I will summarise below.

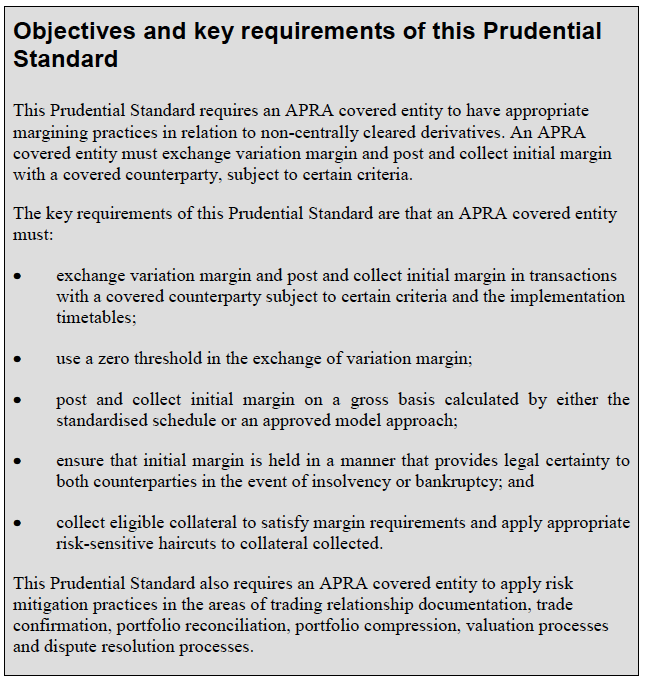

Objectives and Key Requirements

From the first page of the CPS 226 document:

Covered Entity

The requirements apply to APRA covered entities, which are:

- Authorised Deposit-taking Institutions (ADIs), aka Banks.

- General Insurers

- Life Companies

- Superannuation entities, aka Pension funds.

Variation Margin

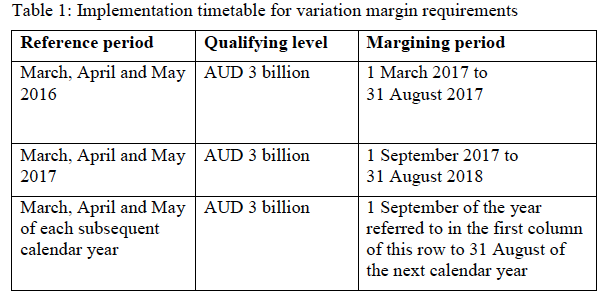

The qualifying level required to exchange variation margin is AUD 3 billion.

This is calculated as “the average of the total notional amount of outstanding non-centrally cleared derivative transactions as at the end of each month in the reference period (March, April, May). The total notional amount is the aggregate of all outstanding non-centrally cleared derivative transactions across all entities within the margining group.

Variation margin must be exchanged for all new trades in non-centrally cleared derivatives, with the exception of physically settled FX Forwards and Swaps entered into during the below margining period, where both the covered entity and the covered counterparty belong to a margining group that exceeds the qualifying level.

Many Australian firms have been complying since 1 March 2017 and others will follow by 1 September 2017.

Initial Margin

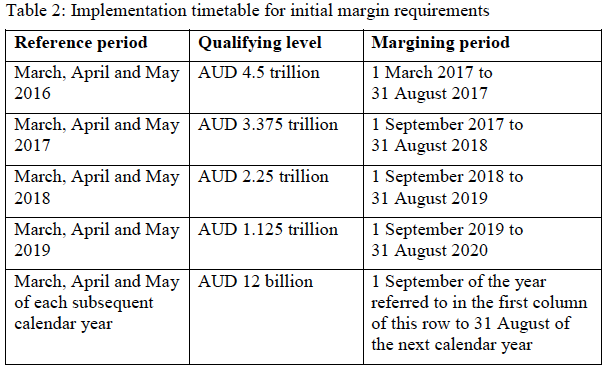

Initial Margin must be collected and posted for new trades based on the table below.

Only one Australian entity, Australia and New Zealand Banking Group Limited (ANZ) is above the qualifying level of AUD 3.375 trillion and will start to collect and post IM on 1 September 2017 with its covered counterparties; large US, EU, CH & JP banks.

The other three major Australian Banking groups should do so on 1 September 2018 and then I am not sure any firms will be captured by the AUD 1.125 trillion level, so September 2020 will be the next important date.

Calculation of Initial Margin

From the document.

The Standardised Schedule looks simplistic and expensive and I doubt this will be used between any firms until possibly September 2020 for small firms.

The only model that I am aware of that has been approved by regulators is ISDA SIMM and I am surprised that the document makes no explicit reference to this. ISDA SIMM is consistent with the APRA Model requirements as described in the following section.

Model Approach

There Model approach summary:

- An Entity must apply to APRA for approval to use a model

- IM must be sufficiently conservative even during periods of low market volatility

- At least a one-tailed 99% confidence level over a 10-day time horizon

- Based on historical data that includes a period of financial stress and does not exceed 5 years

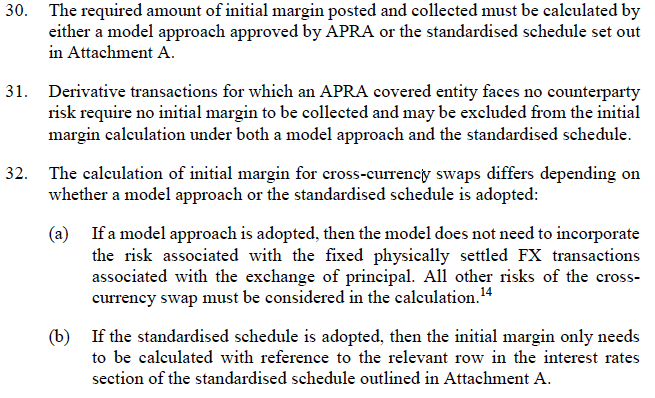

- Diversification is allowed within an asset class but not between asset classes

- Model must be subject to an independent internal governance process that:

- continuously monitors and assesses the value of the model’s risk assessments

- tests the model against realised data and experience

- validates the applicability of the model to the derivatives it is used for

- regularly reviews the model in line with developments in global industry standards for initial margin models

- accounts for the complexity of the products covered

- A covered entity must ensure that an independent review of the initial margin model and risk measurement system is carried out initially (i.e. at the time when model approval is sought) and then regularly as part of the internal audit process. This review must be conducted by functionally independent, appropriately trained and competent personnel, and must take place at least once every three years or when a material change is made to the model or the risk measurement system.

- APRA may vary, revoke or suspend a model approval for the calculation of initial margin, or impose additional conditions on a model approval and may require an entity to revert to the standardised schedule.

- Prior notification is required to APRA for material changes to model or risk measurement system.

Phew, quite a bit to digest there and a lot of work for firms to do before and after model approval, but all sound risk management practices.

Risk Mitigation Requirements

There are other sections in the CPS 226 document covering Eligible Collateral, Collateral haircuts, Inter-group transactions and Cross-border application, however I will leave those of you interested to read yourself here, while I move onto Risk Mitigation requirements.

These require:

- Trading relationship documentation, to promote legal certainty

- Trade confirmation, as soon as practically possible, in writing or non-erasable electronic means

- Portfolio reconciliation, with a scope and frequency to reflect materiality, global standards and industry practice

- Portfolio compression, to replace economically equivalent transactions with less trades and notional, with a scope and frequency to reflect materiality, global standards and industry practice

- Valuation processes to be agreed and documented by the parties

- Dispute resolution policies and procedures including notifying APRA for material in value or time outstanding

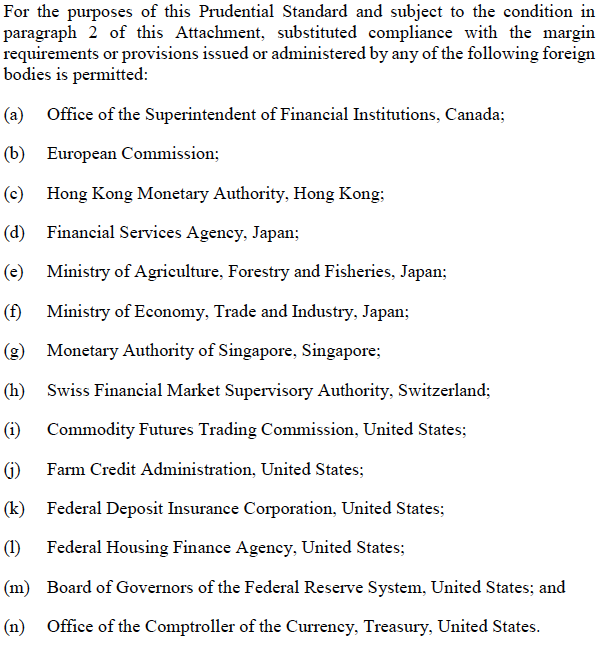

Substituted Compliance

Interestingly the document provides a table of foreign bodies that are comparable in outcomes with the BCBS-IOSCO framework and the CPS 226 prudential standard, for the purposes of substituted compliance, so an APRA covered entity may use those when transacting with a counterparty.

Six US regulatory bodies and three Japanese ones!

Which puts the achievement of the EU, with a single EU Commission for 27 countries into perspective.

The End

Thats it.

Thank you for reading to the end.