- Australian Rates Clearing Mandate now only 6 months away.

- LCH is the current king of AUD$ Rates Clearing

- ASX goes strong on the Cleared AUD$ OIS product

- Regulators may delay mandate start on FRAs and OIS?

- Will a market share split see a CCP basis spread like for USD on LCH-CME?

I thought might be interesting to look at what we can gauge as the Australian market moves to mandatory clearing (still being advised as April 2016 by the regulators) from the data we have available. Will we see a shift in overall volume and product split across CCP’s for the Cleared AUD$ Rates market?

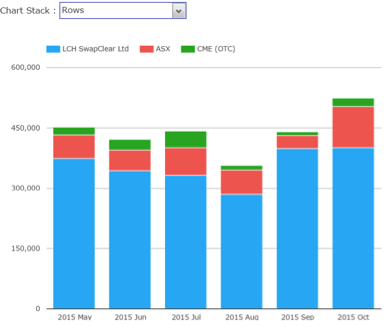

It’s probably still too early for any trends to be picked up, but we can take a look at the current state of Cleared AUD$ Rates Notional Volumes from CCPView for the last 6 months to see the CCP market share.

No surprise that LCH by far make up the bulk of the volume, but certainly interesting to see a large jump on the ASX for October which represented 19% of all AUD$ Clearing during that month. This is by far their biggest market share mth.

A reminder that (based on the Australian regulator draft rules issues in May 15) the following AUD $ product types were to be mandated (plus separately G4 currencies, but we will focus on AUD $ products here).

- Basis Swaps – 28 days to 30 years

- Fixed-to-Floating Swap – 28 days to 30 years

- Forward Rate Agreement – 3 days to 3 years

- Overnight Index Swap – 7 days to 2 years

The mandate is also limited in its application to capture firms with more than $100b in gross notional OTC derivative exposure that are Australian Financial Services License holders or where large foreign swap dealers are trading with those firms. You can read through all the fun draft rule detail here . Word has it that the final rules are ready and waiting the formal sign-off.

Back to CCP volumes and product breakdowns

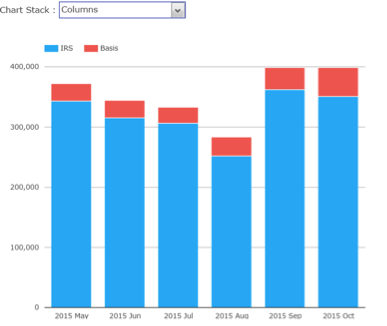

Only the LCH and CME provide the breakdown of volumes by product type. So starting with the LCH, we can see that they clear predominantly the IRS Fixed/Floating and Basis Swaps, with Fixed/Floating representing the majority of notional volume. They are yet to offer AUD$ FRA’s or OIS (the later expected to be available from early Dec 15).

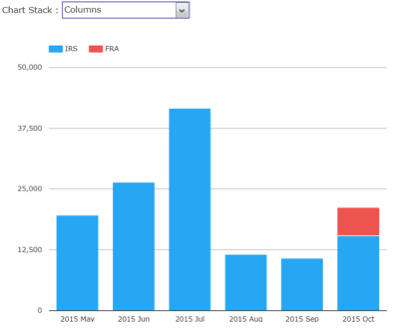

The CME while carrying the smaller overall cleared volume on average about 4-5%, are the only CCP currently clearing AUD $ FRAs. This has been captured in CCPView data from Oct 15.

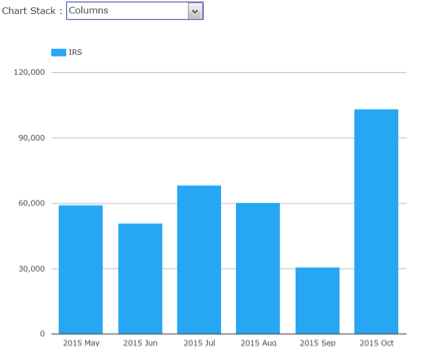

Unfortunately for the ASX we don’t have breakdowns by product. However, it’s fairly well understood that OIS represents a good amount of the ASX cleared volume relative to Basis and Fixed/Floating product types. So while the chart is a little boring in detail, we’ll take the view that their increase is primarily driven by OIS, as opposed to Fixed/Floating and Basis product types at this stage. We know ASX don’t clear FRAs as yet.

The large volume increase in October is interesting and one to watch. It’s a little early to suggest the market has chosen ASX to clear OIS in readiness for the coming mandate, as the main Australian banks trading OIS and likely to be the owner of the flow, have equal access to both the ASX and LCH when it comes to clearing. Remember other factors such as capital efficiencies, margin offsets and other CCP incentives also influence cleared versus non-cleared and CCP location decisions.

So what can we take from this currently?

- Expect a reasonable delay to FRAs within the final mandate rules with only CME currently clearing them and volumes low.

- A shorter length delay expected to occur across $AUD OIS with ASX the only CCP actively clearing, having limited dealer members, but LCH launching in Dec 15

- ASX may have the jump on clearing the AUD OIS volume ahead of a mandate (pending the above point).They will hope it’s a driver to bring across more of the other Cleared Swap $AUD product types

- LCH is the dominant CCP not just on AUD $ IRS but globally. They will launch AUD $ OIS in December with some slightly different settlement terms than that cleared on the ASX. We might expect them to rely on existing market share dominance to influence AUD $ OIS clearing destination of dealers.

- There is potential for a CCP liquidity split for $AUD Rates and especially in the OIS and maybe basis. That bring some basis spread between LCH-ASX on trades?

We’ll certainly watch this space over the coming months and realign some of the thoughts once the final Australian OTC Clearing Rules are signed off and released.

This article is authored by Neil Fletcher.