- Moving clearing of EUR-denominated contracts to the Eurozone is a complicated proposition.

- Bifurcating cleared portfolios will make bilateral markets more attractive than cleared markets.

- This raises questions over existing clearing mandates.

- It also conflicts with the G20 OTC market reforms intended to reduce systemic risk through the promotion of clearing.

- Enforcing a location policy for a given currency can cause the Initial Margin at a CCP to be 25% higher than bilateral markets.

LCH made a public statement last week

We are focusing on Xavier Rolet’s headline this week. For those of you who did not read his commentary, the CEO of LSEG said;

We support the commission’s proposal to enhance the supervisory regime due to Brexit. We also oppose its location policy — mandating all euro-denominated transactions to be cleared only within the eurozone.

Why is the article of interest for us? Mainly because LSEG provided us with an additional piece of information on the cleared swaps market that we haven’t previously enjoyed:

LCH, clears 90 per cent of global interest rate swaps, 28 per cent of which are denominated in euros. Euro swaps originating from EU-based entities comprise 7 per cent of LCH’s interest-rate swaps flows.

For a data-driven blog such as this, the “7%” figure above is something we can work with. So let’s combine with our public sources of data to see what this means in terms of EUR flows per day.

There are a lot of members of LCH SwapClear who are based in the Eurozone

With Clearing Mandates now active around the globe (US, EU, Japan, Mexico, Canada et al) a geographically diverse range of banks must be able to clear and/or offer clearing services to their clients. It is not that surprising that the largest clearing house in the world has many members across many countries – see the list here.

The geographic location of the LCH members does not give us any information about activity. For example, from CCPView, we know that 57% of LCH volumes in 2017 have been USD-denominated, compared with just 28% in EUR. You would not guess that by just looking at where the membership is based (only 27% of members are US-based).

To state the blindingly obvious, we cannot simply assume that Eurozone banks just trade Euros, US banks just trade USD and that market activity is split equitably between members. This is why the data that LSEG chose to share is important to us.

€125bn per day trades “onshore” in Europe

CCPView confirms that 28% of volumes cleared at LCH SwapClear in 2017 have been in EUR. Confident that we are looking at the same data as LSEG, we can look in detail at what is meant by “7% of the LCH interest rate swap flows”.

Crunching the numbers shows that this onshore EUR component equates to 25% of all LCH EUR swap activity, meaning:

- €10.5 trillion are cleared each month in EUR denominated swaps at LCH.

- €2.6trn (i.e. 25%) of this volume has at least one counterparty based within the Eurozone.

- In other words, there is a notional amount of €125bn traded each day in EUR swaps with a physical presence in the Eurozone.

So where are most counterparties based who trade EUR swaps?

EUR swap volumes have the following geographic split:

Showing;

- Total EUR swap volumes transacted each month, split by the location of the counterparties involved.

- Onshore EUR is derived from the 7% data point as above. When calibrated to EUR swap volumes, it works out as 25% of all EUR swap activity having at least one of the counterparties based in the EU.

- An old BoE staff working paper noted that 3% of EUR swap volumes were traded US-to-US after the introduction of the execution mandate in the US in 2013. We assume this has stayed pretty static.

- 72% of EUR swap trades are hence traded with the “Rest of the World”. From the BIS 2016 Triennial survey, we know that most of these “Rest of the World” trades involve at least one counterparty from the United Kingdom.

Dodd Frank shows that liquidity is the key concern

Current data shows that;

- 75% of volumes transacted in cleared EUR swaps do not involve an EU-based entity.

- The off-shore EUR market is nearly 3 times larger than the on-shore market across both Cleared and Uncleared EUR swaps.

- Most “off-shore” EUR swaps typically involve a UK-based entity.

Prior to Dodd Frank, US entities were far more involved in the EUR swap markets, accounting for up to 30% of volumes (see chart).

This 30% of the market moved overnight.

It was the smaller, US portion of the market that moved legal entities, in order to retain access to the greatest amount of liquidity possible.

A geographic mandate to clear conflicts with G20 market reforms

Consider the following:

- Do the same systemic concerns that bring EUR clearing on-shore also exclude any EU-based clearing house from clearing all other currencies?

- Uncleared margin rules have regulatory approval for multi-currency netting across all currencies, including Euros.

If a clearing house only clears a single currency, they will probably be at a disadvantage compared to the uncleared margin rules. It doesn’t matter why a clearing house only clears one currency.

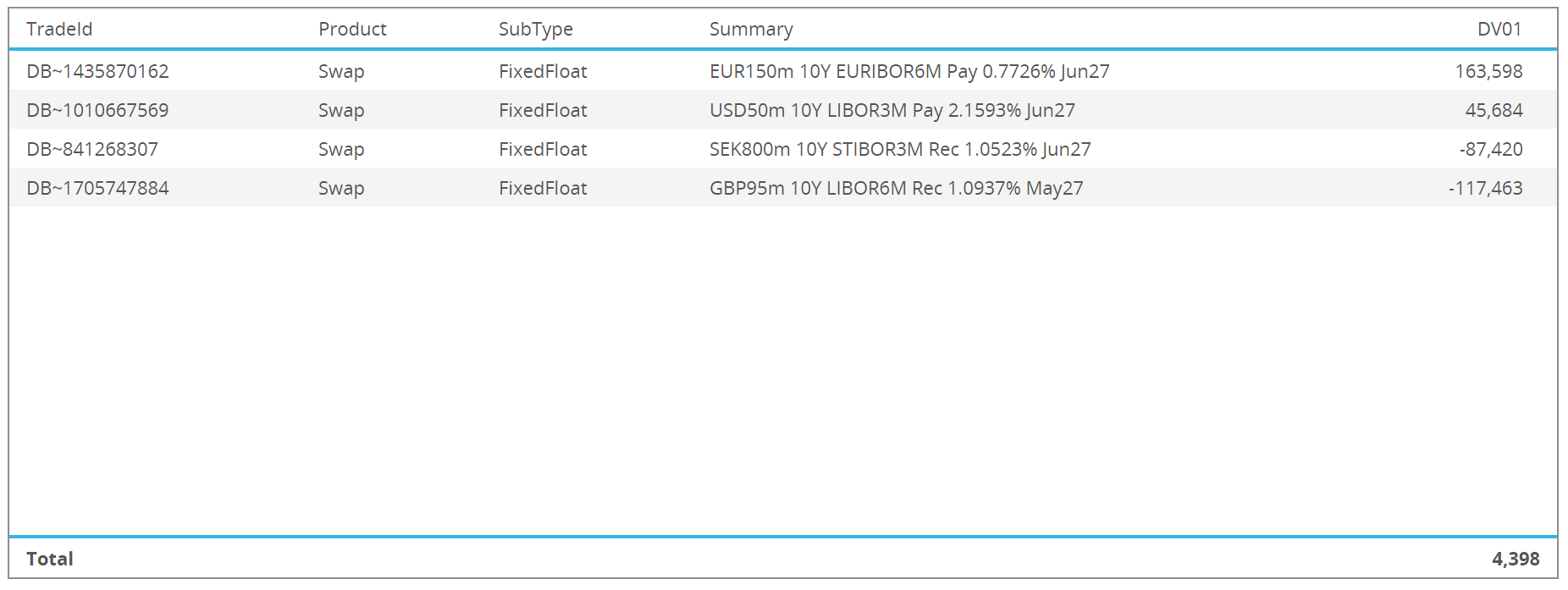

I wanted to prove this to myself. Using CHARM we model a typical European Rates trading portfolio. Consider a Scandinavian asset manager for example. They might have a small balanced portfolio in clearing of just 4 trades:

Showing;

- A EUR vs GBP position,

- A EUR vs SEK position

- A USD vs SEK position.

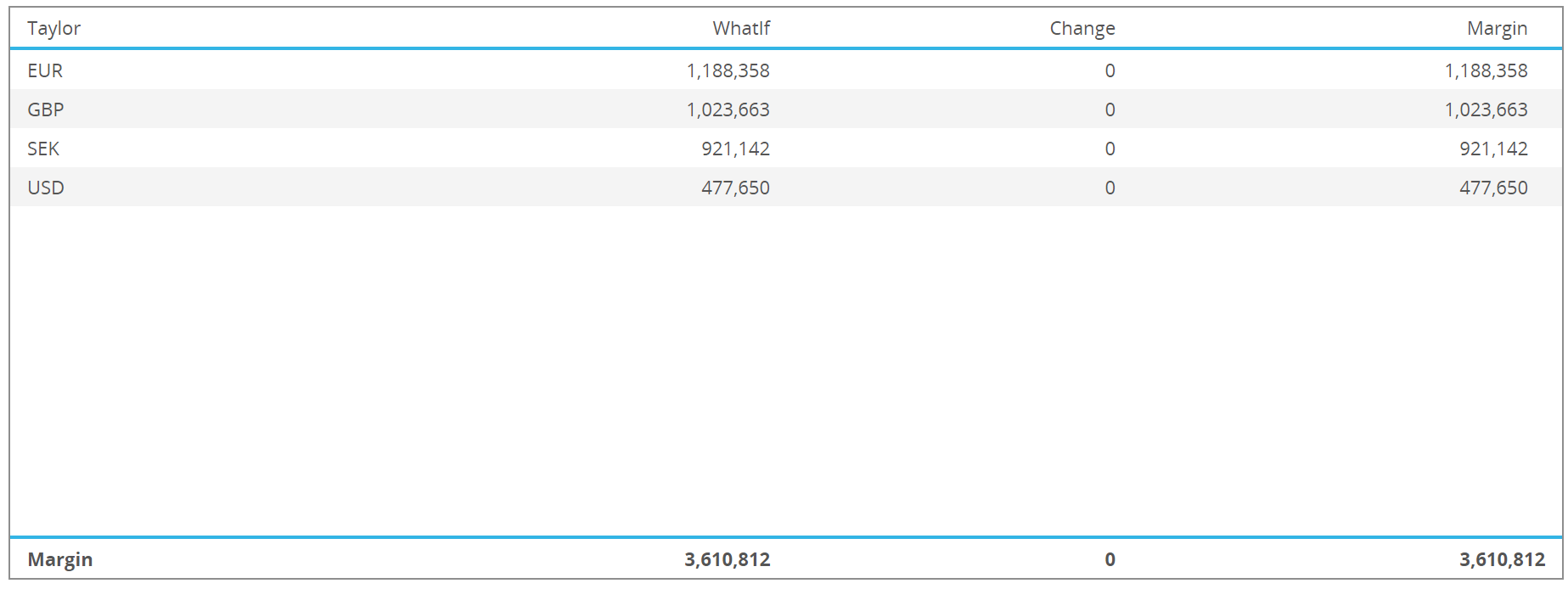

What is the IM requirement if this is all cleared at a single clearing house? Our currency-weighted Taylor expansion shows an IM requirement of about $3.6m at LCH:

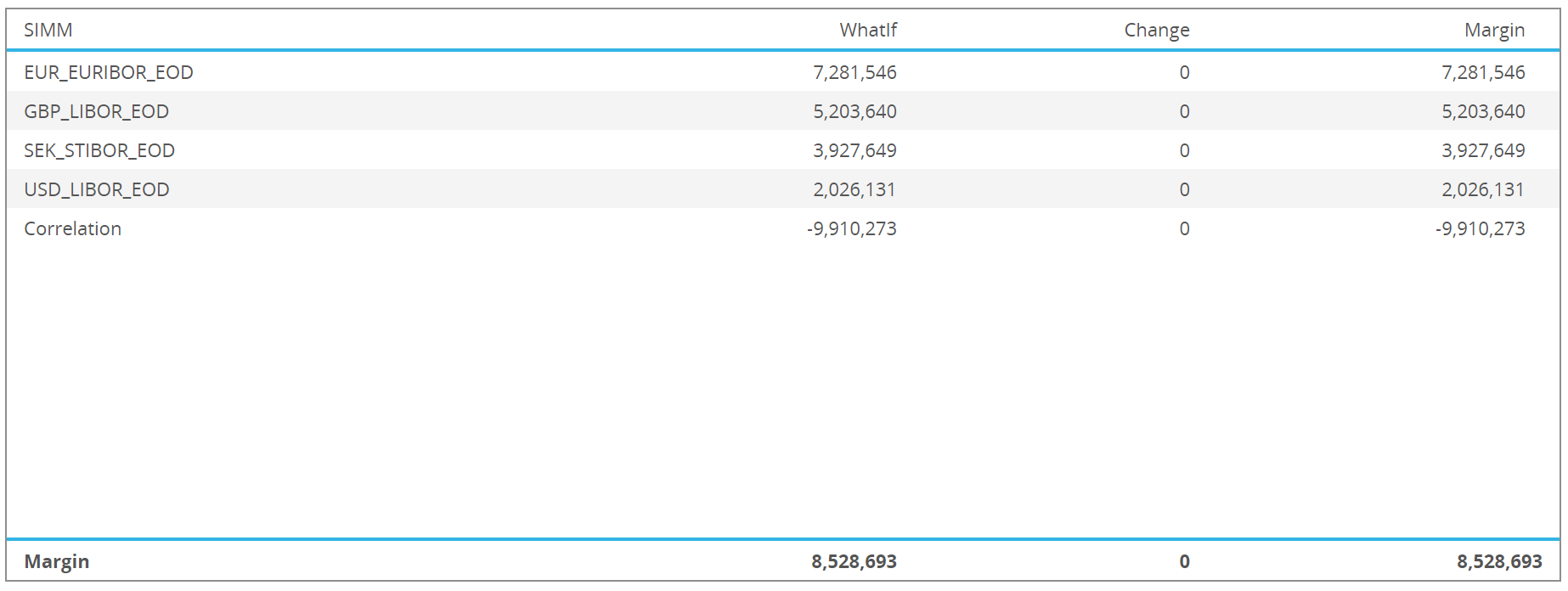

What if this portfolio were bilateral (i.e. uncleared)? Uncleared Margin Rules mean that IM would have to be posted. Under SIMM, the IM required is $8.5m – much higher than within clearing. This is consistent with regulatory reforms intended to promote clearing to reduce systemic risk in OTC markets.

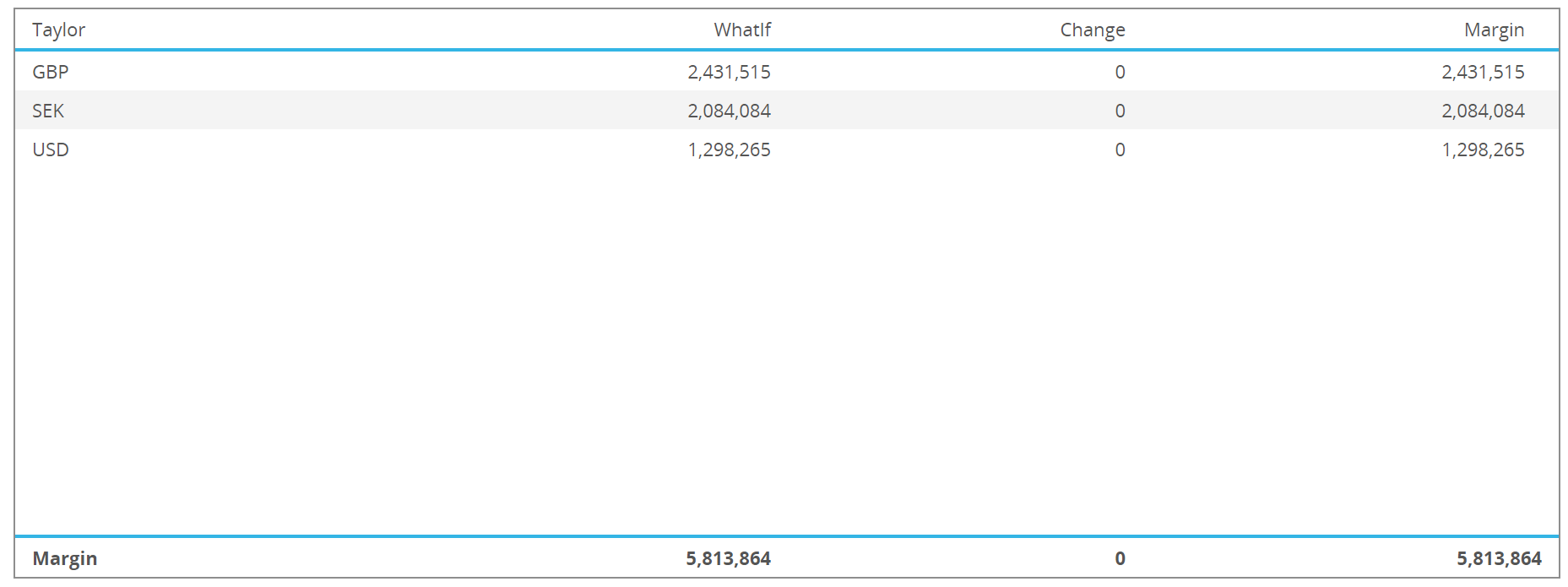

What happens if we have to move the EUR portion of the cleared portfolio to a clearing house based in the Eurozone? First, my IM at LCH for these cleared trades increases – to $5.8m. This is because I lose all diversification benefits from the EUR portion of my Rates portfolio.

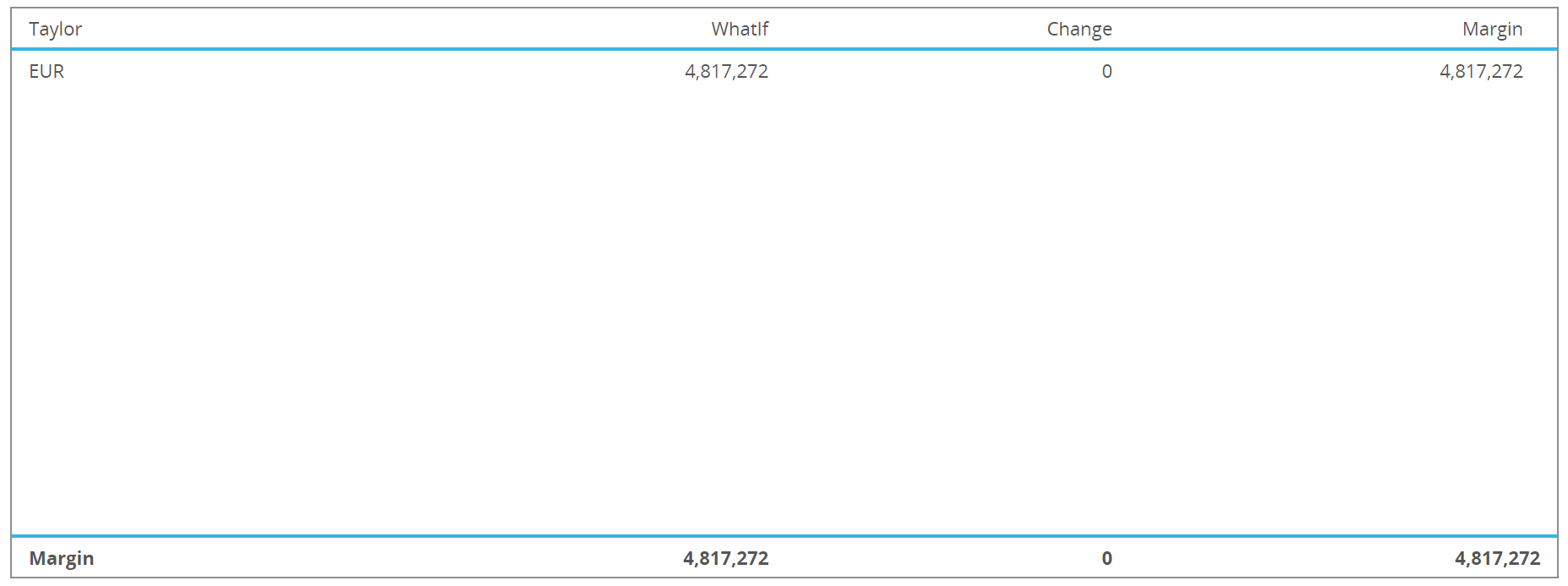

And I will now have to post IM against my EUR position in the Eurozone. This is a very directional position and would require a further $4.8m…

Uh-oh. My total Cleared IM requirement now sits at $10.6m. If all of these trades were uncleared, it would be only $8.5m.

European market participants may therefore find it economically beneficial to leave a multi-currency swaps portfolio uncleared. In this case, it offers a 25% saving. Crazy…..

This appears to be in direct conflict with the intentions of the G20 OTC market reforms.

Enhanced Supervision is the right path forward

Every way I look at this, enhanced supervision from the ECB of offshore markets is the best way to go.

I think Mario Draghi echoed the sensible position of LSEG this week:

“[It is] crucial that [the ECB] can at least preserve the current level of involvement over systemically important euro-denominated clearing activities, regardless of the framework adopted by the EU legislator and of the terms of the future EU-U.K. relation.”

It seems sensible that the ECB should have a supervisory role in the regulation of EUR clearing wherever it takes place.

In Summary

Market participants such as European banks and asset managers need to be aware of the risks to their business due to policy changes. To do this, they need to understand and be able to optimise both cleared and uncleared margin requirements.

Please reach out to us to find out how CHARM does this for you.

Summarising our blog today:

- A geographic mandate to clear could bifurcate market liquidity.

- Recent experience with Dodd Frank reform suggests that all trading could move offshore into eurozone-remote legal entities.

- European regulators hence risk losing even their existing oversight in the event of a location-based policy.

- Initial Margin will be lower in bilateral markets versus bifurcated clearing.

- Existing clearing mandates will therefore result in an economic penalty for Europeans required to clear.

- Enhanced supervision from the ECB of offshore markets is sensible.

While not _entirely_ a trivial risk the focus on EUR denominated clearing as driver for clearing relocation is probably somewhat misguided. From an EU-regulatory perspective the primary angle of attack is likely to be recognition of a clearing regime as EMIR compliant. Or not. From that the OTC Clearing relocation impetus will be client business driven (presuming lack of EMIR recognition for UK based CCPs post Brexit). That generally would seem politically more elegant and avoid outright regulatory clashes with US-regulators as well.

Hi Nikolai – thanks for the comment. It’s an interesting discussion about how it could be achieved from a regulatory perspective. If LCH is not deemed as EMIR-compliant, then aren’t we basically saying a european client can trade a swap there, but they will be penalised from a capital perspective? In which case, why bother clearing it? For some currencies, the mandate will say I have to (e.g. EUR and USD). But what about MXN, CAD, AUD? All of the liquidity is in cleared swaps at LCH, and I might struggle to find uncleared prices. I might have to pay a “liquidity premium” or “ccp basis” to transact my mandated currencies on-shore, and yet some currencies I am forced to clear offshore. What then? My portfolio is naturally bifurcated and I will have more IM requirements. I might just be better off leaving everything bilateral….or moving everything out of Europe!

My money would be on LCH relocating it’s SwapClear offering to LCH SA and therefore making it EMIR compliant . But that’s pretty speculative.

I agree with Xavier Rolet statement and this must be the way forward.

However, I understand that the EU (the ECB, to be more precise) has two main concerns: crisis management and the emergency liquidity assistance in EUR to an offshore CCP; centrally cleared repo. However, is it even feasible to introduce the location policy for repo only?

I guess if the policy is enacted via EMIR compliance and hence capital disincentives, then it would be very difficult to restrict to a single product type.

Hi Chris,

Sorry for the probably trivial question. Right after the image with the 4 trades, I read:

“Showing;

A EUR vs GBP position,

A EUR vs SEK position

A USD vs SEK position.”

How do I have to interpret the above piece of text? From what I could see in the image the trades are single currency Fixed to Float swaps and no XCcy swaps.

Thank you,

Chris

It is my fault if something isn’t clear, so thank you for asking! There are no xccy swaps in the portfolio, only IRS. But I think of the positions in terms of the Rates position in each currency. So in the example, we have a portion of the portfolio that is paid in EUR rates vs receiving in GBP rates (my so-called EUR vs GBP). The balance of the paid EUR rates position is offset against (some of) the SEK received position etc.

Why no one remembers that Eurex has OTC clearing and it is already sitting in European territory… ?

Very interesting post. Thank you Chris.

Two questions popped up:

– if everything is held uncleared than the 50mln threshold would in your example already cause bilateral to be a lot cheaper right (as in, 0 exchange of IM)?

– if it concerns a party (in the future) to which IM requirements apply (so above 50mln and more than 8bn notional) would it not also be interesting to see what would happen in terms of pricing/mva? Longer directional portfolio’s would probably get priced by the sell side for having to fund the margin towards the CCP or other party (to hedge the position).

Thanks in advance for a response

Thanks for the comments. We didn’t really consider a threshold – but you are quite right. In terms of MVA, you make a very good point, that the more directional the portfolio is, the more likely that an MVA charge will be significant. This is yet another factor we could try to model – great idea!

So BME CLEARING in Spain does. Since November 2015 I guess