Clearing broker data is out for Q1 2017, so I wanted to run the numbers and see if anything has changed.

Lets start with a view onto the number of registered FCMs.

This shows 64 firms registered (down 1 from Q4 2016), and 55 firms with any Client Requirements (down 2). On the bright side, there is a new entrant listed, Apex Clearing. Not yet showing activity, but good to see a new name pop up!

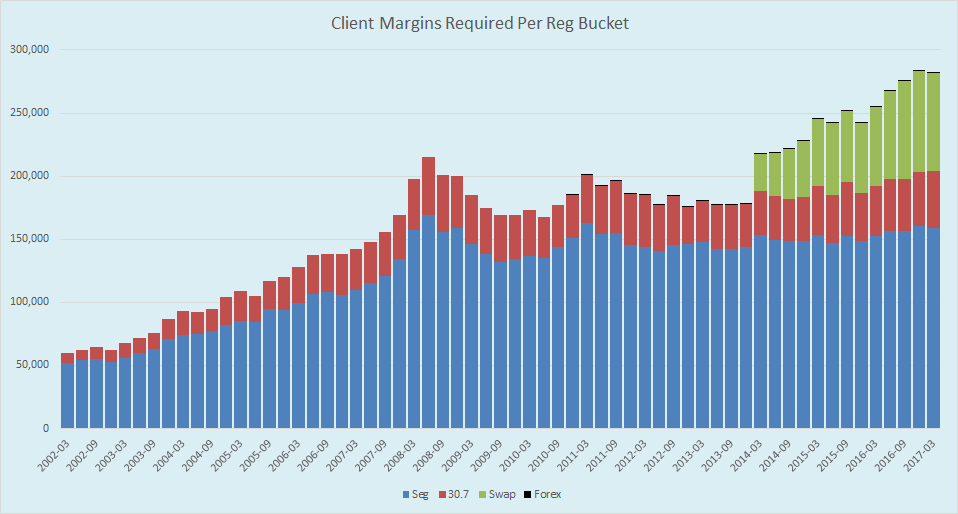

The other headline metric we like to monitor is total client required margins, which was slightly down for the quarter, primarily from a small drop in Swap requirements:

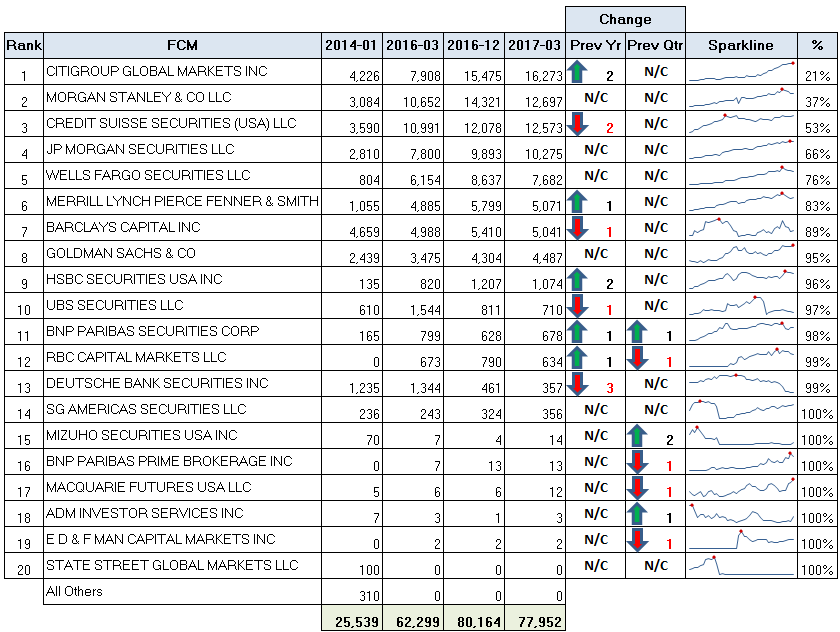

SWAP LEAGUE TABLE

Let’s jump right into the latest ranking of FCM’s for swaps:

Showing us:

- Citigroup more than doubles its client funds in past 12 months, securing #1 position

- Despite growing 15% over the past 12 months, Credit Suisse is down two spots

- No change in the top 10 over the past quarter

- If you look at the Sparklines, you can tell that lots of firms are now off of their recent peaks

For this quarter, we’ve added a “%” column on the right of the table, which shows us the cumulative market share. We’ll come onto market share & concentration later. But first, lets look at other league tables.

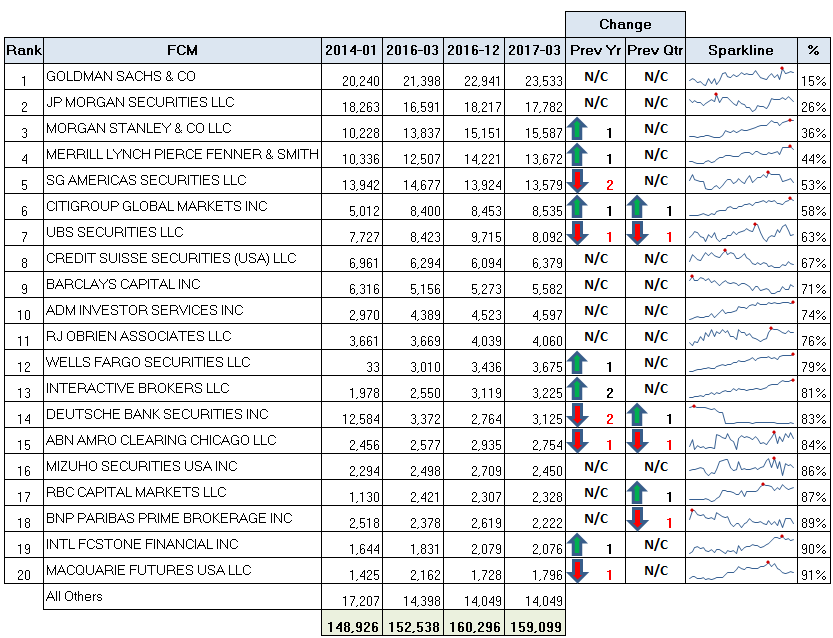

SEG LEAGUE TABLE

The Seg funds rankings:

Not much changed here in the past quarter. I am a big fan of the Sparklines, showing monthly history of seg funds in mini-chart form. I note the steady grind higher for firms like Morgan Stanley, Merrill Lynch, Citi and Wells.

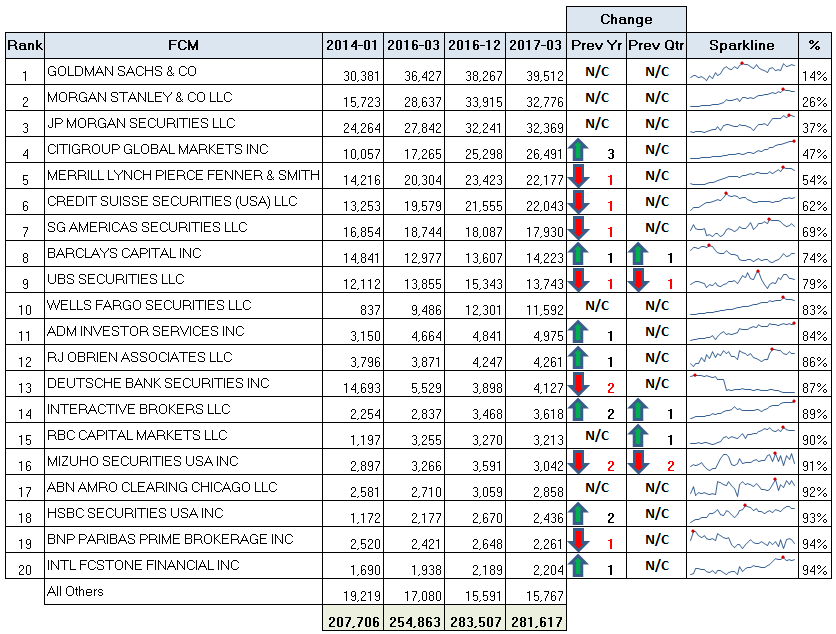

OVERALL LEAGUE TABLE

If we combine Swaps, Seg, and 30.7, we get the combined table:

Of course what jumps out here is Citigroup, up 3 spots in the past 12 months.

CONCENTRATION

I also produced concentration analysis for each of these – Swaps, Seg, and Combined. In case you missed it, in our last article, we discussed concentration of these markets, and we used a couple indicators to gauge the competitiveness:

- Four-Firm Concentration Ratio

- Herfindahl-Hirschman Index (HHI)

I might suggest going back to read the details of that article, but we gleaned that:

- Competitive markets have Four-Firm Ratios <50%, and HHI’s of <1,500

- Highly Concentrated markets have Four-Firm Ratios >80%, and HHI’s of >2,500

- Values between those (50-80%, and 1,500-2,500 respectively) are in the moderate zone.

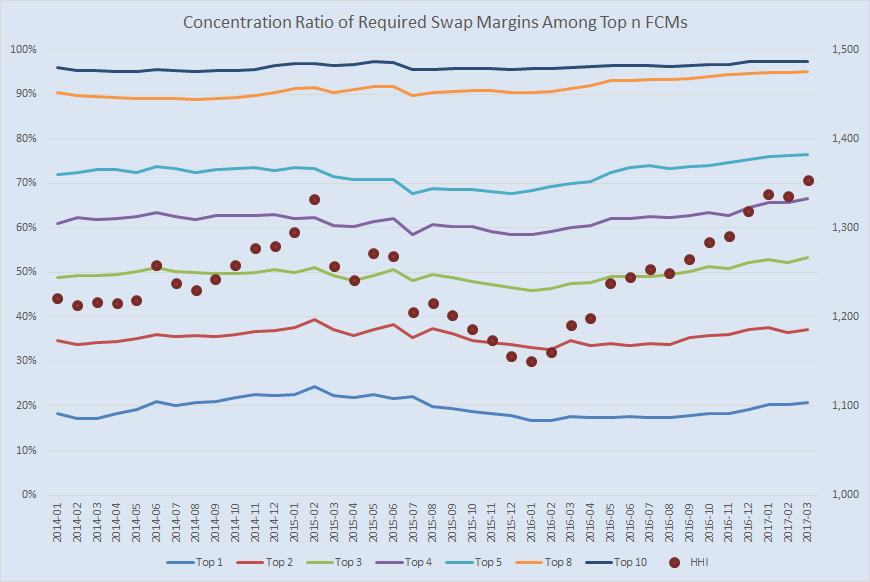

So lets look at concentration metrics for Swaps first:

HHI for Swaps now rests at 1,353, slightly higher than the previous high back in Feb 2015 of 1,332. The Four-Firm Ratio is 66%. This HHI is in the “normal” category, and the Four-Firm Ratio is in the “medium” category. But is it appropriate to conclude this?

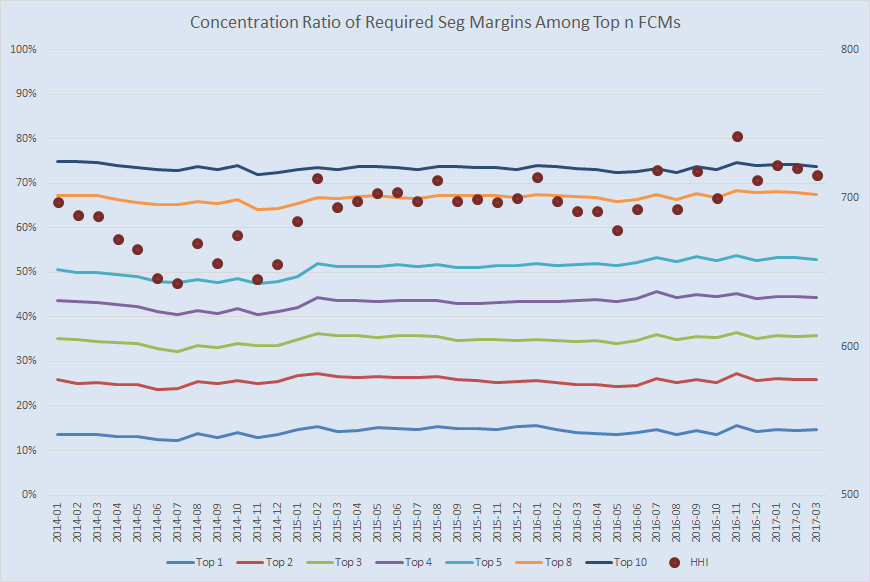

Moving to Seg analysis:

The HHI reading stands at 715. Has been as high as 741. So less concentrated than swaps. And Four-Firm Ratio sits at 44%. Both of these in the “competitive” zone.

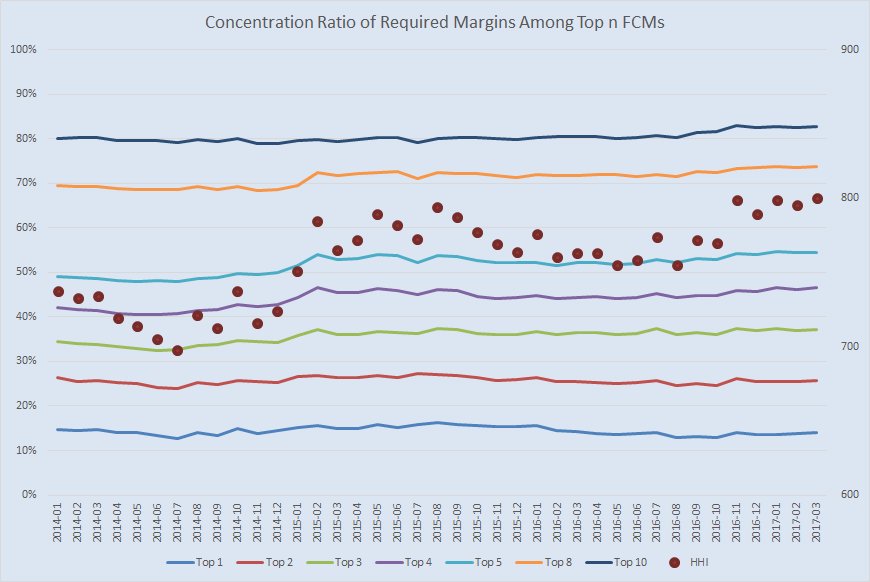

And finally the combined/overall Swap+Seg+30.7:

Where the HHI is touching a reading of 800, and the Four-Firm Ratio is 47%. Again, both “competitive”.

WRAPUP

We see the league tables largely unchanged this quarter, with notable overall progress by Citigroup in the past 12 months.

The story of concentration remains debatable. Since my last post on the topic, the feedback has generally fallen into a few categories:

- It’s competitive. Just look at the HRI readings.

- You cant use HRI as a metric on an industry that is prone to systemic risk. (If 20% market share blows up in a financial market, its much worse than 20% of phone companies going bust).

- When it comes to swaps, there are really only a handful of viable FCM’s, so the analysis is not applicable.

- When it comes to seg balances, you have to look at institutional business separate from individual investor (eg Goldman Sachs in separate analysis to TradeStation)

I think these commenters have a point.

We’ll be keeping an eye on it. Let us know, or leave a comment, if you have a particular point of view on the subject.