History in the making…..

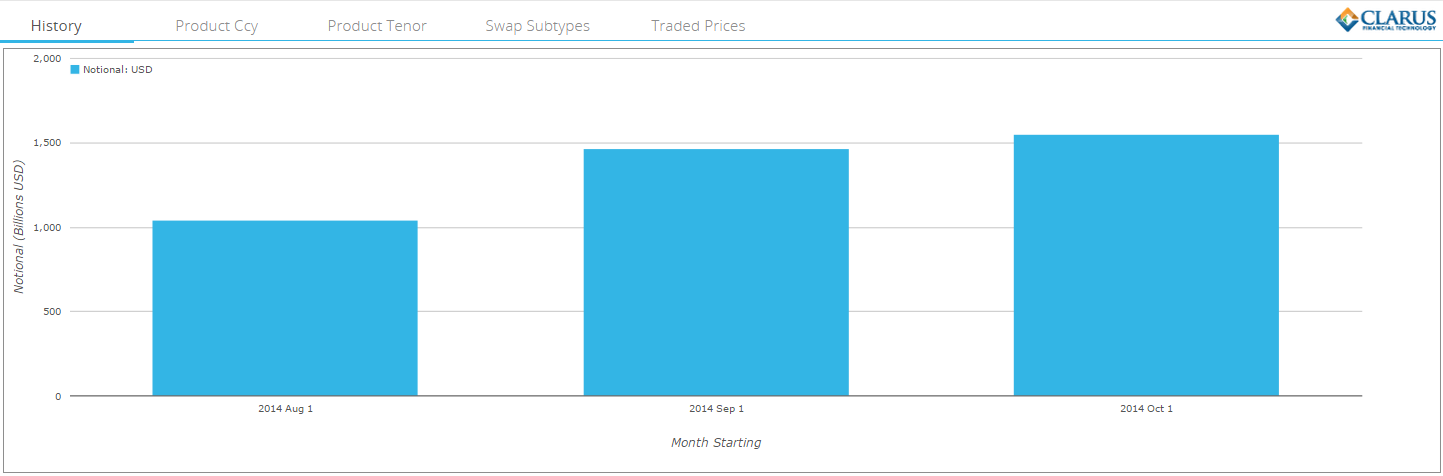

October 2014 was another record month for volumes traded on-SEF. Following on from Amir’s blog, we can see that October on-SEF USD IRS volumes hit a record, breaking $1.5trn for the first time:

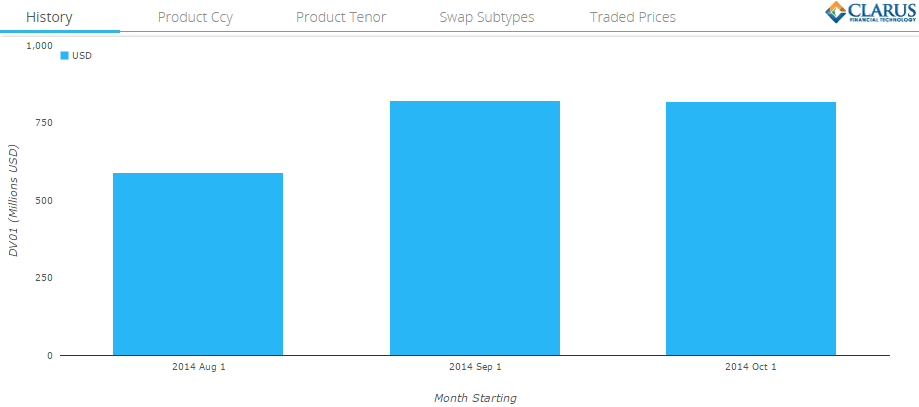

DV01!

Using a new version of SDRView Researcher for USD Swaps, we can also run these numbers in DV01 terms (Amir beat me to this announcement!). Here, we can see that September just pipped October to being the record month for the amount of risk traded on-SEF:

Given these two metrics, it is likely that:

Given these two metrics, it is likely that:

- Just as CME saw record volumes in their Eurodollar contracts, more of the activity in October was short-dated. This is evidenced by FRA volumes, which were greater in October than September.

- September was an IMM month, therefore some of the volumes will have been down to IMM roll activity, as Amir highlighted. This makes the October volumes look even more impressive.

Who caused the volume spike?

Clearly, one of the big causes of increased volumes in October has been the extreme volatility we saw – large enough to be included in CME’s tail-scenarios for Initial Margin. With these types of stressed markets, it is therefore important to understand where the increased volumes are coming from. For example, during September 2008, it is a fair bet that the extreme deleveraging we saw ignited a spike in dealer-to-dealer volumes that will not necessarily have been mirrored by client flows. Is the same thing true in current markets?

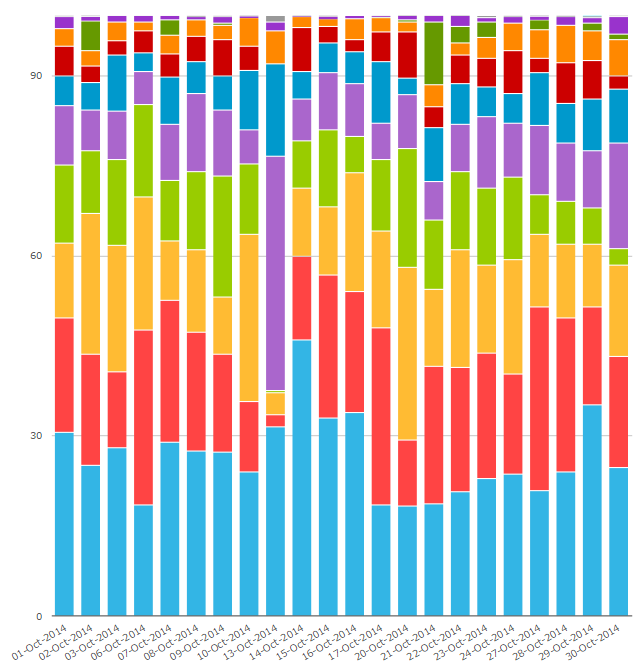

What does market share tell us?

Using SEFView, we can look at the market share by SEF per day during October for vanilla Swaps:

The blue bars at the bottom of the chart are the Bloomberg Market Share. We can therefore see that even on the most stressed days in the markets (October 14th,15th,16th), BSEF did not suffer from any loss of market share. In fact, as measured by notionals, its’ market share actually increased. This suggests that clients were just as active as dealers during the turmoil.

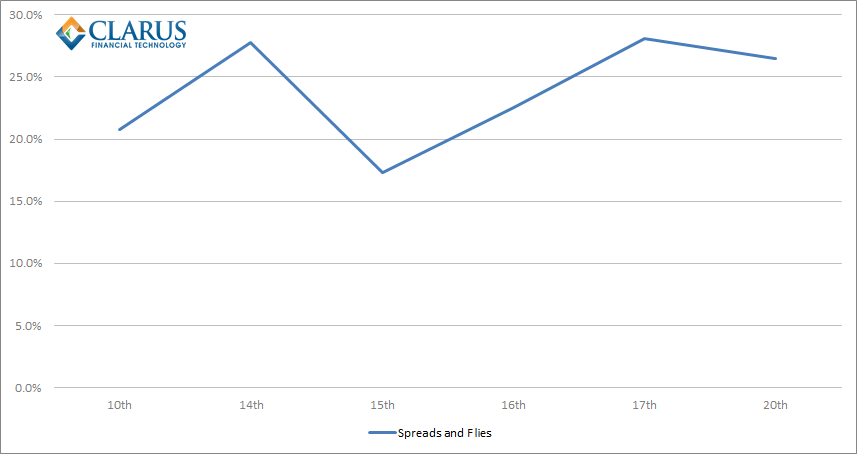

Spreads and Flies

Using all of the Clarus tools available to us, we can drill-down even further and look at a specific subset of the swaps market – package transactions. I have used the SDRView API to extract trade-by-trade data to again identify package trades in USD Swaps – specifically Maturity Spreads and Butterflies. For the most volatile day in USD swaps, October 15th, we can see a reduction in the number of trades transacted that were either a maturity spread or butterfly:

To clarify, the above chart shows the percentage of the market that was transacted as part of a package trade – by DV01. On average it was around 25%, but on the 15th, when Bloomberg saw a notable increase in overall market share, this dropped to 17%.

Bloomberg

When I drilled down into the numbers, it was notable that Bloomberg was able to transact a similar notional amount of Spreads and Flies across all days in the sample period. What this meant was that Bloomberg’s market share went through the roof on October 15th – to nearly 75%!

From the above we can see that:

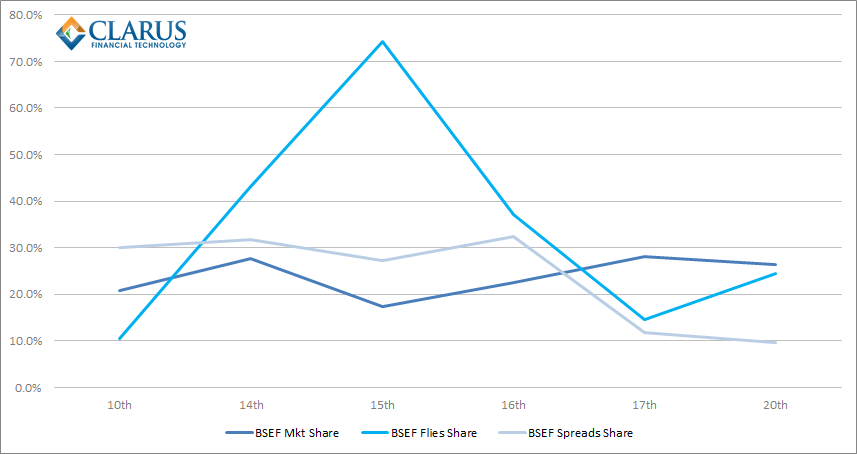

- On a DV01 basis, the BSEF share of the whole market is fairly consistent – around 20-30%. BSEF actually saw a small dip on the 15th October, in contrast to the amounts reported purely on a notional basis.

- The variability in market share for BSEF in the butterfly market is striking in its’ variation. BSEF saw a maximum market share of nearly 75%, and a minimum share of just 10%.

- On average, BSEF saw a market share of all butterflies traded of 34% – certainly above it’s typical market share in the outright or spreads market.

Disintermediation?

At the start of this analysis, I asked whether it was dealer-to-dealer flows or dealer-to-client flows that ignited the spike in activity during those volatile few days in October. From the data, it is clear that BSEF maintained a fairly consistent overall market share on a DV01 basis, therefore suggesting that client flows increased at a similar rate to dealer flows. However, BSEF was also able to register a 75% market share in some trading strategies – such as butterflies. It is therefore unlikely that BSEF is now purely a dealer-to-client market – they must have captured a decent chunk of the dealer-to-dealer butterfly market on October 15th as well. That should be music to the ears of firms wishing for more disintermediation in swaps trading.

Future analysis

I’ve concentrated on USD Swaps here, but we can easily repeat the analysis for any currency – as the October data shows, BSEF is currently a market leader in EUR and GBP SEF trading as well. Given my background, I prefer to blog about the Rates market. However, we can repeat these analyses for Credit, and to a lesser extent, FX markets as well.

I’ll leave it to Clarus users’ to see whether there were similar spikes in market share across the asset classes.