Bloomberg are #1 for SEF liquidity in Q1 2015 whilst Tradeweb saw the highest overall volumes. We saw record USD Swap volumes reported to the SDRs in March 2015, with our review highlighting increasing compression activity. The great month for the industry was rounded-out with over 60% of volumes traded across a SEF.

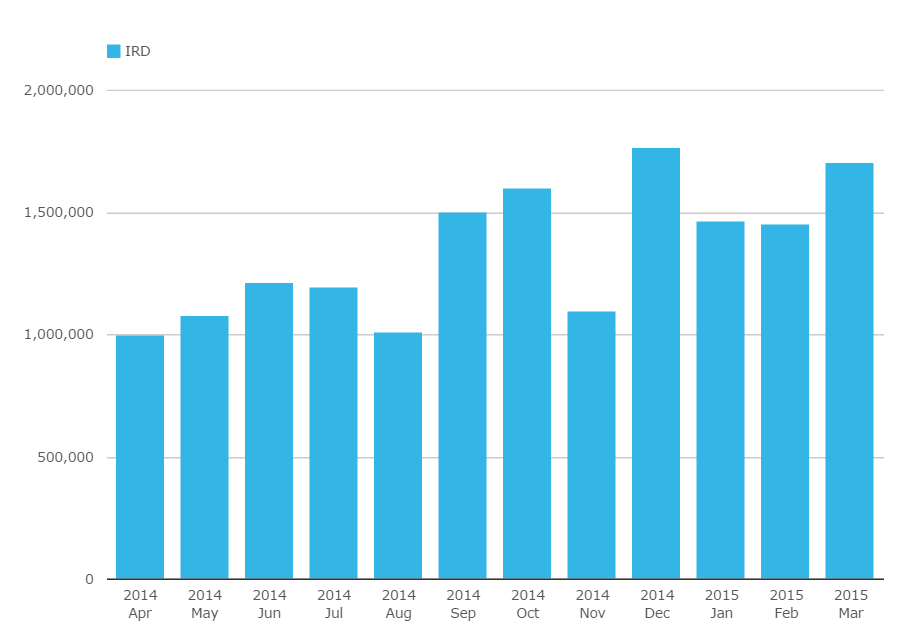

USD IRS On-SEF

$1.56trn in notional traded across SEFs during March 2015. This is the highest ever on-SEF monthly volume as measured through the SDRs. This makes a nice headline (is there such a thing as click-bait when talking about Swaps?), but it’s not 100% accurate when looking at all of the available data.

When we use SEFView to look at these same volumes, we see March was not quite a record month. This is because the SEFs report their volumes in-aggregate, without applying the block thresholds to individual trade amounts. SEFView therefore paints the truest picture of total volumes, and we see that March 2015 just fell short of breaking the December all-time record:

Nevertheless, it’s fair to say that March 2015 was a pretty healthy month, and that the industry as a whole has had a strong Q1.

IMM Roll

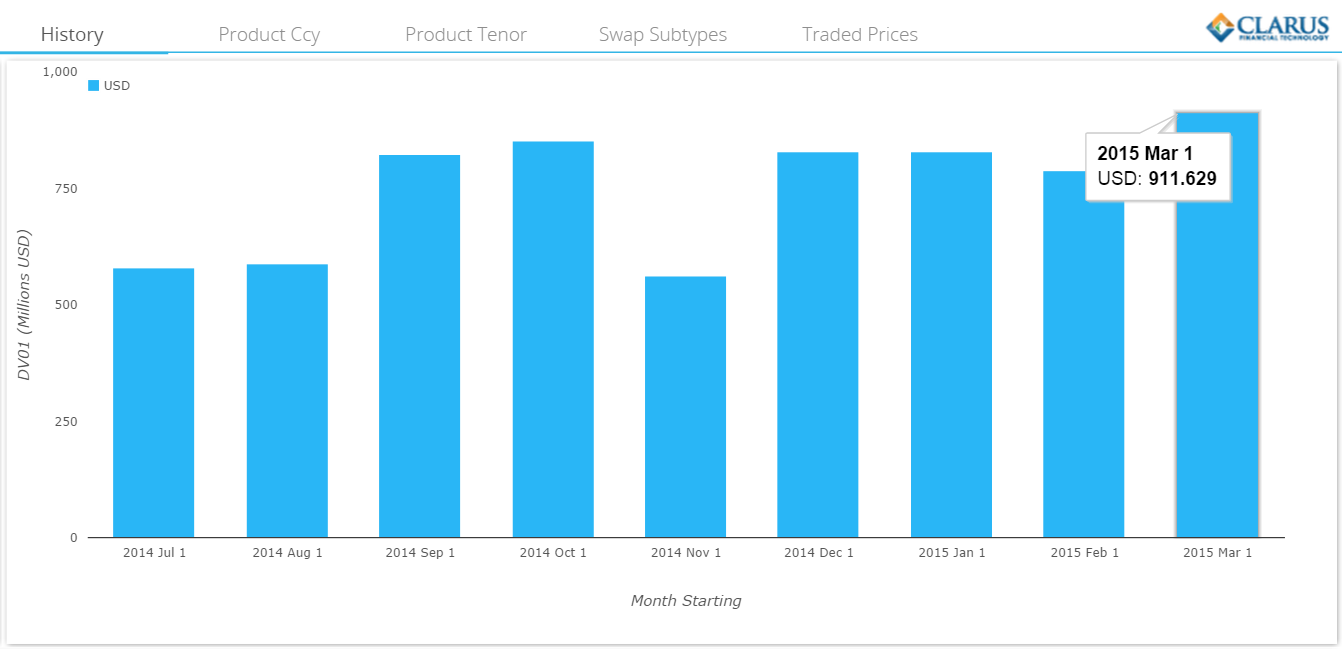

For those that missed it, March of course included an IMM Roll. To paint a fairer picture of volumes relative to previous months in 2015, we should therefore remove these largely portfolio-maintenance related volumes. Fortunately, that’s exactly the type of thing we like to do here at Clarus. In true Blue Peter fashion – here is one I prepared earlier, which finds that $39.9m of DV01 was traded as part of the March IMM roll. Doing some extra analysis now, I find that $33.9m of this risk was traded on-SEF.

Therefore, let’s look at the SEF volumes in DV01 terms from the SDR in March, showing a total of over $911m. When we correct for the $33.9m related to IMM rolls, this leaves us with a total of $878m in DV01 traded during March 2015. Therefore, even with this correction in place, March saw the largest amount of risk ever reported to SDRs – and was well above February’s $789m total:

Volumes and Volatility

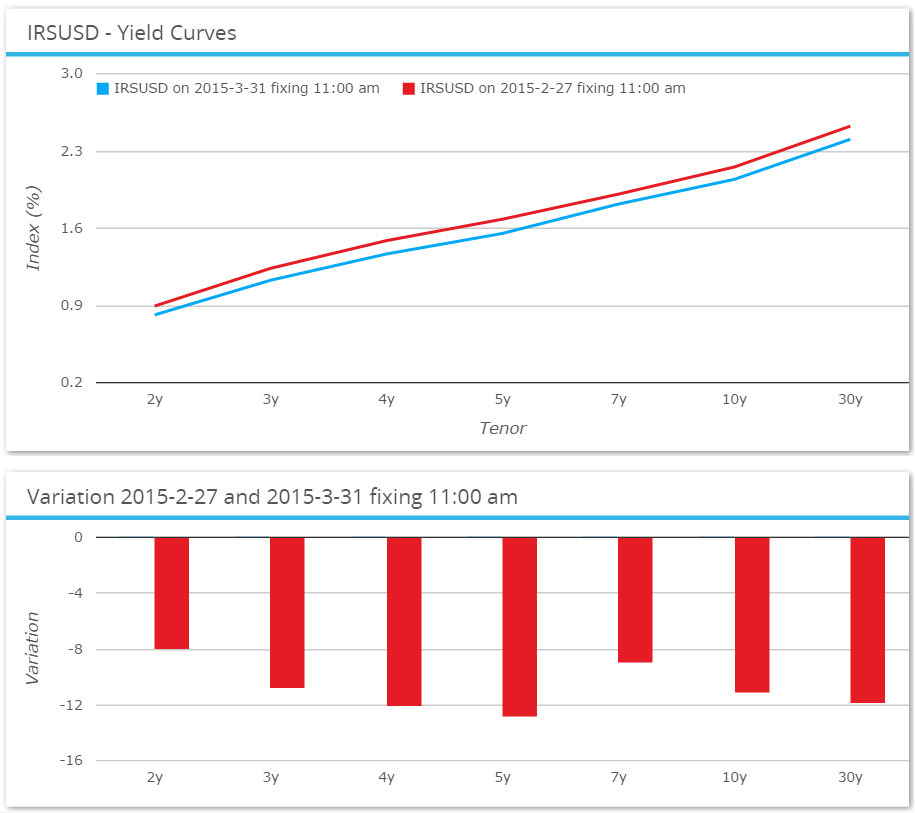

Unsurprisingly, volatility has begun to drop off slightly as we progress through 2015. Using SDRFix, we can see that about one-third of February’s heady move higher in Rates has been reversed in March:

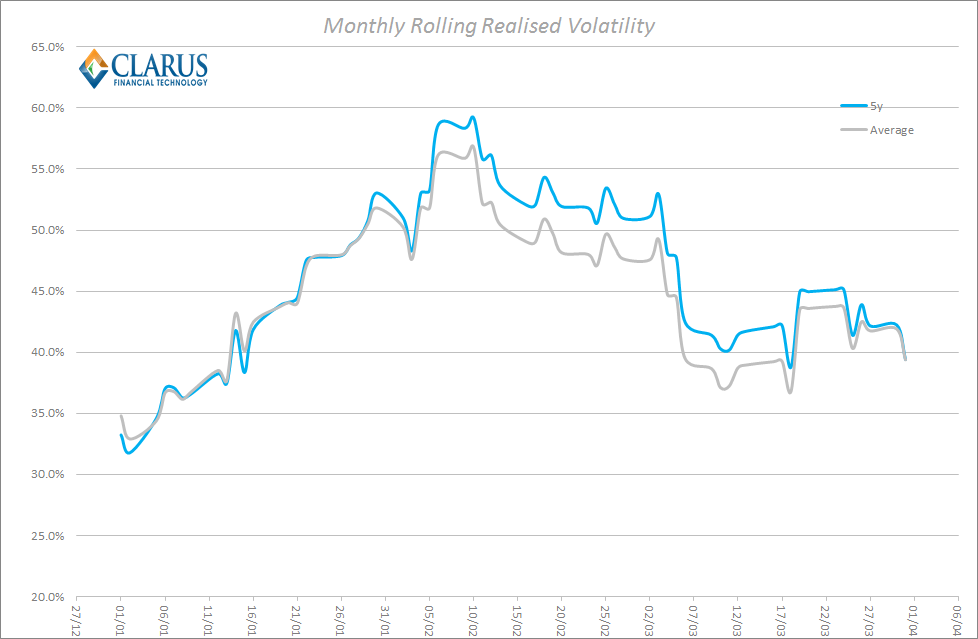

Whilst the absolute move in Rates has not been huge, it is worth having a look at the realised volatility throughout the month. As we can see, during March the monthly annualised volatility stabilised above 40%:

This is way above some of the lows we saw back in 2014 of just 25%, so helps explain (and justify?) the elevated volumes we continue to see.

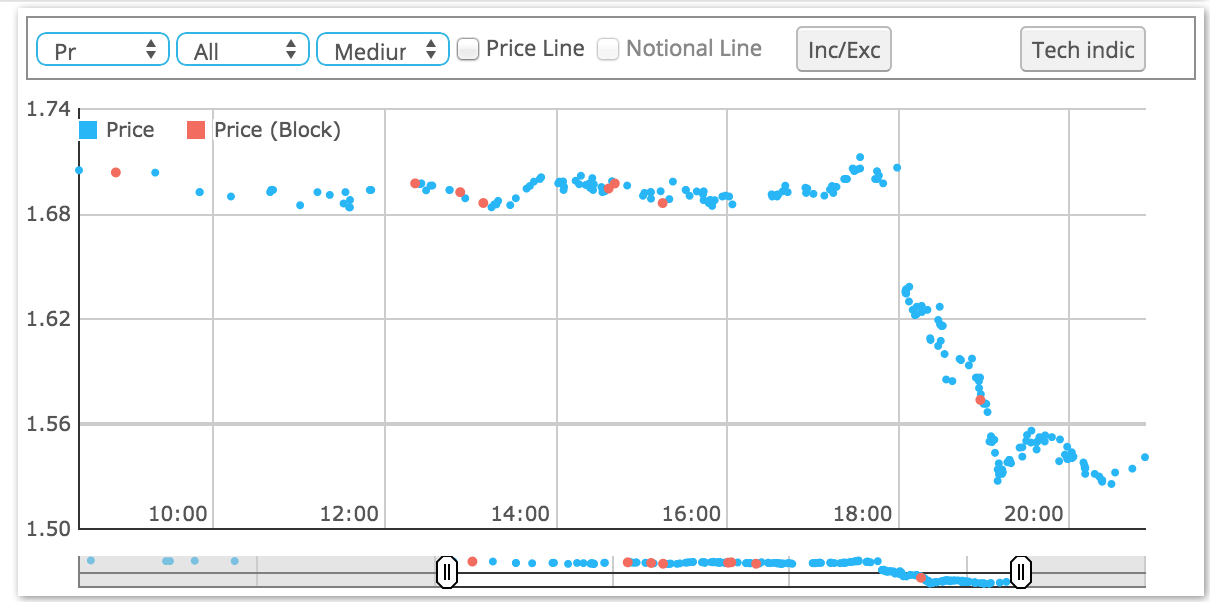

Of course, looking at these numbers as a time series can hide certain events during the month – such as the FOMC meeting on March 18th. This was a particularly volatile day as the intraday chart of 5 year prices shows (below), with a heady 16bp decrease in Rates following the dovish tone. This was undoubtedly the biggest driver of prices during the month, with this one event accounting for much of the monthly decrease in rates.

CCPView

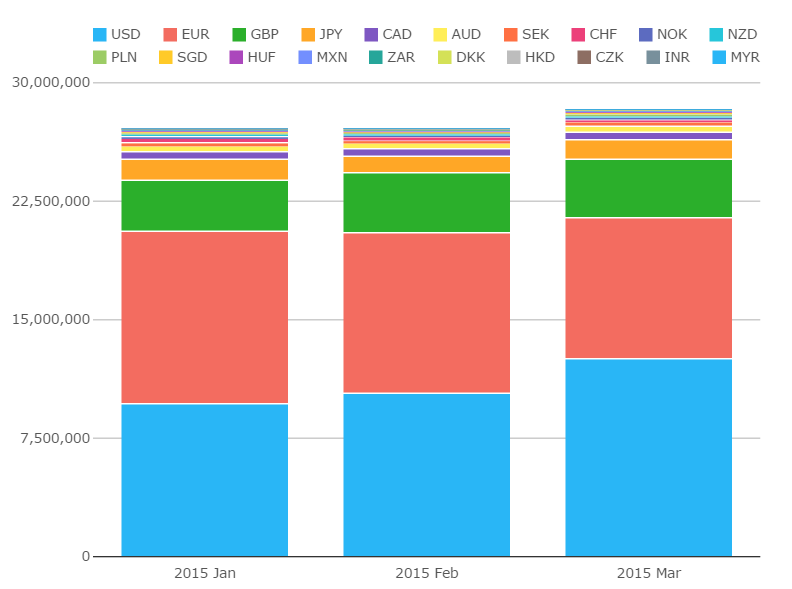

Taking a bit of a step back, we take an even higher level view. CCPView allows us to capture the broadest spread of cleared markets by looking at everything that the CCPs reported throughout the month of March. We can see yet more month-on-month increases in volumes across most currencies:

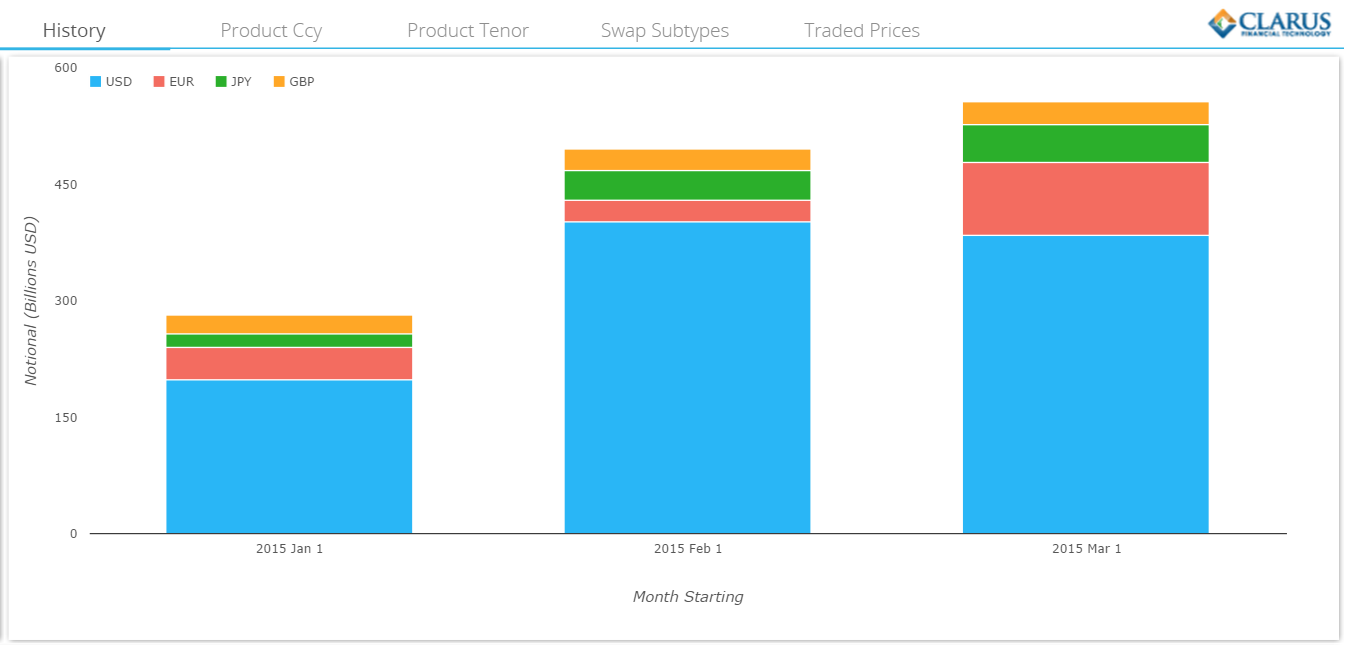

And we are pleased to see that industry efforts on Compression continue unabated. This means that whilst the volumes going through clearing houses are increasing, we are not seeing an explosion in “Open Interest”. SDRView Researcher shows that we saw the highest volumes of compression so far reported to the SDRs in March:

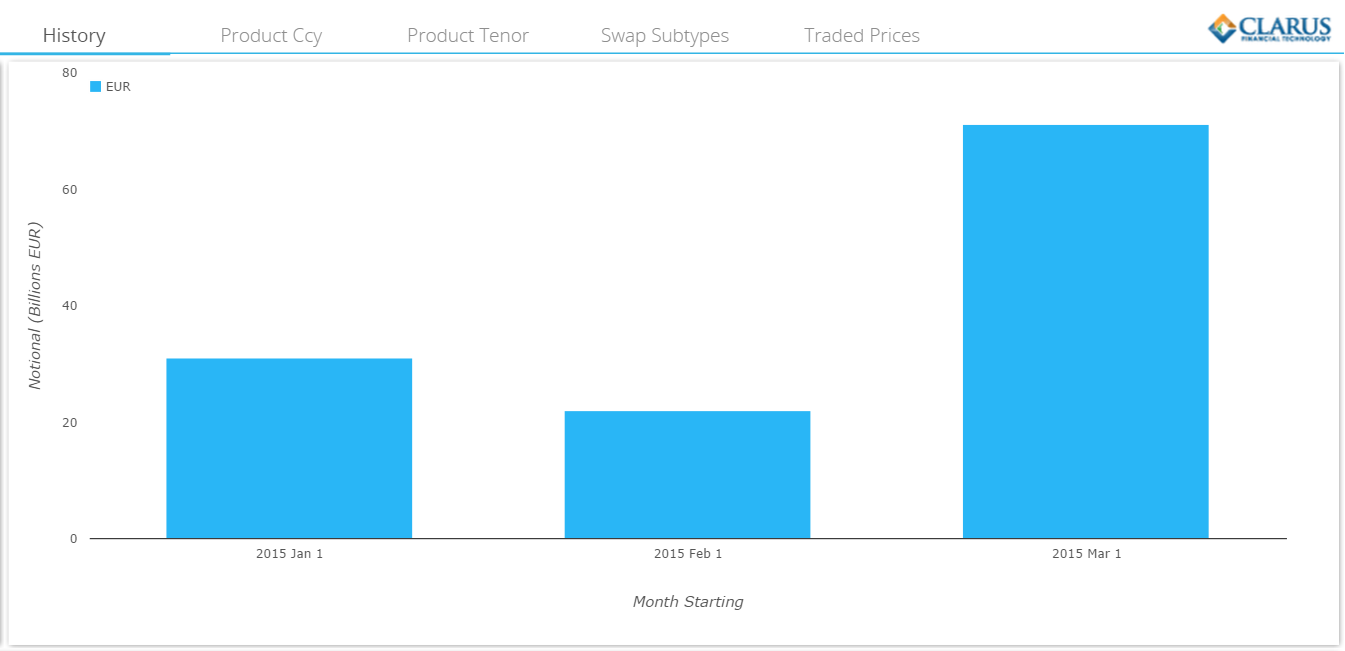

And if we drill down on EUR, we see that over 3 times as many compression trades were identified during March than previous months:

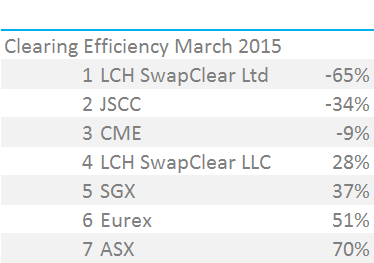

These Compression volumes have helped improve our favoured Clearing Efficiency metrics as well. This month LCH, CME and JSCC have all managed to see a drop in Open Interest whilst still recording healthy new volumes – see table to the right.

These Compression volumes have helped improve our favoured Clearing Efficiency metrics as well. This month LCH, CME and JSCC have all managed to see a drop in Open Interest whilst still recording healthy new volumes – see table to the right.

Whether a result of maturing trades, FX moves or actual compression (very likely in the case of the top three) we see very healthy ratios this month, staying well below 100%.

To recap, what this means is that for every new unit of cleared trade, we are seeing less than 1 unit added to the residual stock-pile of trades. This is great news for customers as it means they are, overall, reducing line-item and maintenance charges associated with legacy portfolios whilst continuing to be able to move risk through OTC markets.

The large drop in LCH Open Interest relative to their healthy volumes is probably due to further weakness in the EUR (our data is USD denominated), plus further compression in their EUR portfolio. Whilst we will see some of this activity through the SDRs (such as the large compression volumes in EUR we looked at above), it is likely that there are far more conducted by non-US persons as well.

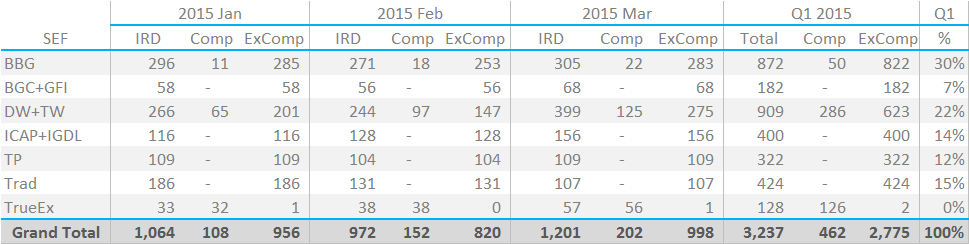

SEF Market Share Ex Compression Trading

With a record month in March topping off a record quarter for volumes, it’s been a great start to 2015 for the industry. However, as Amir looked at, not all volumes are born equal. Therefore, let’s remember that Compression List trading is here to stay but that it can also artificially inflate the picture of “real” liquidity out there. Whilst these modes of trading remain highly useful, they are more akin to portfolio maintenance than true liquidity provision. Therefore, this month let’s look at SEF Market Share excluding Compression List Trading volumes. We also therefore exclude all FRA volumes as the vast majority of these are also transacted as portfolio maintenance.

Taking USD, EUR and GBP and looking at volumes in DV01 terms, we see the following for Q1 2015 in SEFView:

With a little data manipulation, we can subtract the known Compression volumes from these totals. Amir explains how in his Compression blog. In brief, we know that for BBG the real (uncapped) compression volumes are double what is reported to the SDRs, and we apply this same ratio to TrueEx volumes. We then assume that TradeWeb’s are 1.75 times. This gives us the following adjusted table:

Showing:

Showing:

- Bloomberg have a huge 30% market share of vanilla trading across USD, EUR and GBP markets.

- Tradeweb grab second place at 22%, despite over 31% of their volumes being compression related. As you can see from the above table, Tradeweb are actually in first place when Compression is included.

- Ex-Compression, Trads are in third place at 15% – conversely, thanks to their lack of presence in portfolio maintenance trading!

- The exclusion of portfolio-maintenance FRA matching systems sharply reduces ICAP’s market share from 23% to 14%.

- And unsurprisingly TrueEx are down to a 0% market share.

Overall, during Q1 2015 we found that over 14% of SEF Volumes were related to Compression List trading. This was on an upwards trajectory throughout the quarter, increasing from 10% to nearly 17% in March. Much of this additional volume has been captured both through changes in the workflow process and by new platforms (TrueEx) challenging the incumbents with innovative solutions. It therefore sometimes pays to take stock and look at which venues have the truest liquidity in the old-school sense of the word!

And Finally…

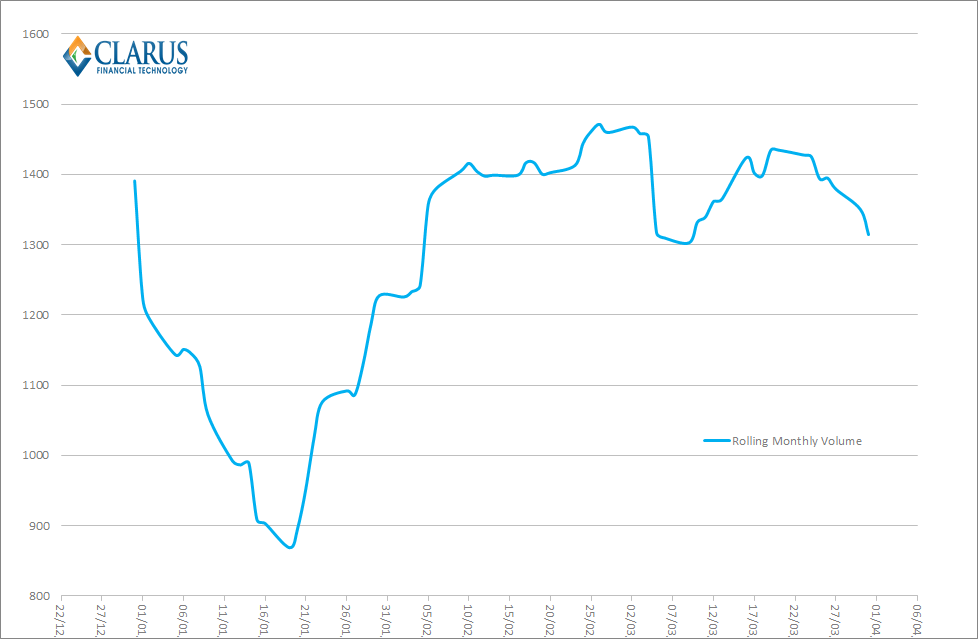

Whilst it’s nice to fit into everyone’s reporting cycles with a monthly review, it’s worth noting that all of this data is available on-demand and as near-as-damn-it in real-time. So sometimes it’s worth bearing in mind that just because two trades happened within the same month doesn’t necessarily mean they have any relation to each other. I’m therefore quite intrigued by the rolling time-series of volumes that we can create from the data instead. These can make it easier to gauge trends and hence spot any changes as they emerge.

For volumes, a rolling 20-day total shows a fairly constant picture throughout the month, that was towards the top-end of the run rate for the first quarter of 2015:

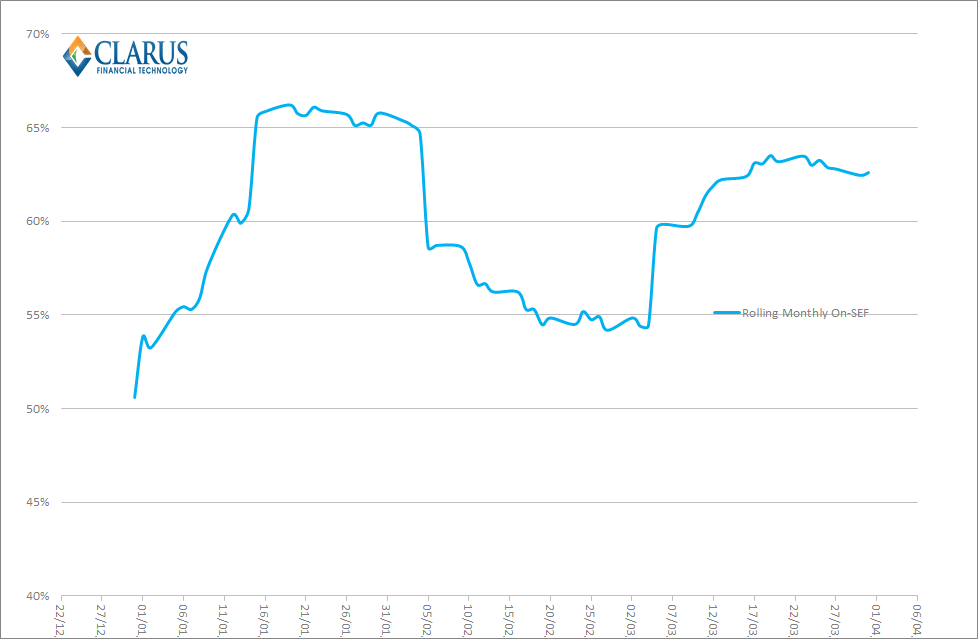

And going hand-in-hand with this we see a constant proportion of USD trades conducted on-SEF:

In Summary

Tradeweb take the plaudits for the highest overall volumes during Q1 2015, with Bloomberg taking the number one spot if we exclude Compression List Trading volumes. As Amir highlighted in his January blog, innovation seems to be the way to win volumes for SEF venues in 2015.

Volumes continue to push higher, whilst volatility in underlying markets has subsided a touch. Compression continues to be a focus which can distort the liquidity picture on a SEF, but results in more efficient central clearing houses. Fortunately, Clarus data allows us to paint a true picture of liquidity and having more efficient CCPs is certainly a positive evolution for market structure.

For the industry as a whole, the proportion of trades conducted on-SEF was running above 60% for the whole month. March was therefore a very positive month. It’s fair to say that greater volumes and a greater proportion of trades are going across SEFs than ever before – and may it long continue!