BREXIT – Day Three, What is Trading?

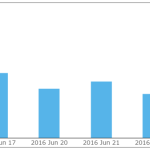

This blog will be updated throughout the day, so please remember to refresh the page (just hit F5). Following on from our BREXIT -What is Trading after the Result? Day One, and Day Two blogs, we will again be keeping a close eye on trade prices and volumes reported to US SDRs. 18:17 LON – […]

BREXIT – Day Two, What is Trading?

This blog will be updated throughout the day, so please remember to refresh the page (just hit F5). Following on from our BREXIT -What is Trading after the Result? Day One, which was last updated on Friday 24 June at 21:15pm after NY close, we will again be keeping a close eye on trade prices […]

BREXIT – What is Trading after the result? Day One

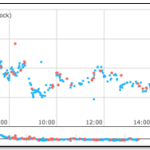

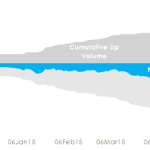

This blog was updated frequently throughout the day. Now that the UK trading day is done and dusted (21:06), we’ll call it a day. The final GBP swap volumes should include all of the DMO-close related trades that have gone through the SDRs, and we’ve finished with a USD update just after 4pm New York time. Thanks for following today. See […]

CPMI-IOSCO Public Disclosure by European CCPs

European CCPs have recently started to publish lots of quantitative data covering their Default Fund, Initial Margin, Collateral, Credit Risk, Liquidity Risk and other Financial Disclosures. This has been done in compliance with the guidance provided by CPMI-IOSCO with the public disclosure aiming to further increase the transparency of financial markets and CCPs in particular. The data […]

SEF Trading on US Holidays

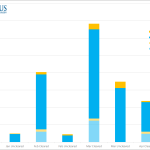

EUR swaps trading is intriguing on US holidays We don’t have many data points to play with… ….but the data shows continued EUR Swap activity on-SEF on US Holidays. Of this activity, much of it is client trading, which I find surprising. These volumes naturally filter into the data for Client Clearing at LCH on US Holidays.. […]

ECB QE and Eonia Swaps

We take a look at Eonia invoice swaps, which match the dates for German bond futures traded at Eurex: From volume data, we see an increase in Eonia swap activity post-QE. The price action in Schatz appears closely related to short-end Eonia swaps, whilst in Bobls and Bunds it is harder to pin-down. The appearance of trades with […]

Volatility and Volumes in Europe

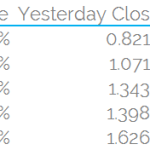

Since European Rates made all-time lows on 17th April, we have seen an unprecedented sell-off in European fixed income. SDRFix shows the moves from 17th April to the close on 5th June 2015: Showing: A huge steepening on the yield curve, with 30y rates 90bp higher (!), versus 2y higher by only 7.2bp. 5y are […]

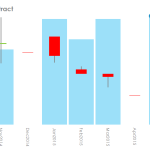

Data Visualisation for Swaps – a Tufte Approach

Data visualisation is meant to take something complex and make it simple and easy to understand. When I saw this in a blog recently, I immediately thought “Hey, that’s what Clarus do!” Interest piqued, I’ve begun delving into the fast-evolving field. As a Swaps-trader for over ten years, this aspect of the industry pretty much […]

What percentage of the market is in the US SDR data?

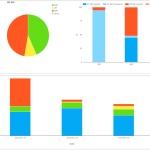

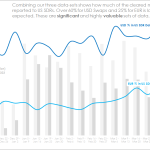

We analyse the SDR data in light of the whole market in the cleared Rates space. SDR data is shown to represent over 60% of total-market volumes at a trade-by-trade level. That’s huge! It’s funny how times change. Next month, the BIS will update their semi-annual review of OTC Derivatives. As recently as 2013 I would have to (manually) […]

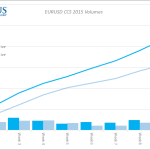

Cross Currency Swaps: SEFs enjoy QE-fueled volume boost

SEFs in 2015 have seen huge increases in Cross Currency volumes, seemingly as a result of ECB QE. European credit markets are a hotbed for foreign issuers right now, and this is driving a significant shift to On-SEF trading for this asset class. The FX Effect It’s certainly not new news that EUR/USD FX is plummeting, and has been on a […]