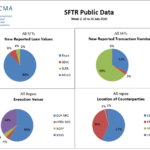

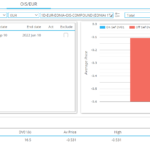

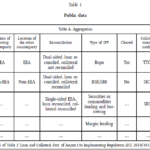

SFTR Public Data

In April I covered Securities Finance Transaction Reporting (SFTR) and ended that article by stating that I would check back end July for the first set of public reports from Trade Repositories. As there are four authorized Trade Repositories (DTCC, Regis-TR, UnaVista and KDPW), I had expected to look for the weekly data files published […]

€STR Discounting Switch

I’m sure that I am not the only one sat here wondering how the switch from EONIA to €STR discounting went at the CCPs over the weekend? As far as I understand it, the change in valuation (cash compensation) amounts should have settled on Monday (July 27th) morning. Will this switch lead to activity in […]

SFTR Reporting – Public Data

For some time now I have been noting, but not reading, articles about the Securities Financing Transactions Regulation (SFTR) being implemented in Europe, so today I wanted to take my first look into this regulation. Background The ESMA website has a good section on SFTR Reporting, so I will copy & paste liberally from that, […]

Is the Leverage Ratio impacting Swaps Trading?

Is the Leverage Ratio impacting Swaps Trading in Europe? This is a question posted by the authors of a recent ECB Working Paper, “The anatomy of the euro area interest rate swap market“. We provide an overview of the paper and look through the window that it provides into post-trade data in Europe. Executive Summary […]

Eurex Swap Volumes On the Up

Given the continuing uncertainty around Brexit as the UK government struggles with a parliamentary vote, I thought it was time to re-visit EUR Swap volumes, which I last looked at in early October 2018. I noted then that Eurex market share in the third quarter was 0.96% and little changed from the corresponding quarter a year earlier. […]

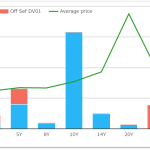

GBP Swaps for Dummies

GBP IRS markets are the third largest Interest Rate Derivatives market. Almost 100% of volumes are cleared at a CCP. Most trades are standardised contracts versus 6 month Libor (IRS) or SONIA (OIS). SONIA swaps are frequently forward-starting out of MPC dates and IMM dates. 42% of GBP Libor swaps are forward-starting; spot-starting swaps account […]

Clarus Research cited at UK Parliament Treasury Committee

LSE’s Xavier Rolet cited our research in today’s UK parliament treasury committee meeting. During the session on ‘The UK’s future economic relationship with the European Union’ it was this research on EUR clearing that he referred to; ‘Moving Euro Clearing out of the UK: the $77bn problem?’, in answer to questions from Jacob Rees-Mogg. The […]

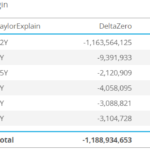

Moving Euro Clearing out of the UK: the $77bn problem?

We estimate the Initial Margin impact from moving EUR Clearing out of the UK This could happen as a result of Brexit We can make an estimate as to the maximum margin impact possible using publicly available data In terms of Initial Margin, we only see a small impact on the LCH SwapClear portfolio in London But […]

BREXIT – What is Trading?

We may have skipped a day yesterday (prior commitments, sorry all!) but we can’t really ignore the price action this morning in GBP swaps. The BoE comments yesterday bringing rates lower this morning. Bye bye that 1.00% handle in ten years…. End of Day GBP Wrap-Up 187 trades were reported to the SDRs. Over £8bn in […]

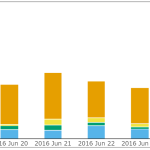

BREXIT – Day Four, What is Trading?

All seems calm in the markets overnight. We’ll continue to update this blog throughout the day with observations on volumes and prices as activity picks up. Just hit F5 to refresh. End of Day GBP Wrap-Up Better late than never….we’ll close this blog with a review of what traded in GBP on the 29th June. […]