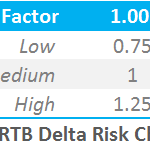

FRTB SA – Residual Risk AddOn

Following on from my article FRTB – The Default Risk Charge, I wanted to look at another specific component of the Standard Approach, namely the Residual Risk Add-On for instruments with non-linear payoffs. Background In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum Capital Requirements for Market Risk; also known as the […]

FRTB – Excel Calculator for the Standardised Approach

What is the market risk capital charge for a bank trading an interest rate position? We calculate some examples using the Sensitivities-based Method under FRTB standards We find that a standalone 10y USD IRS results in a market risk capital charge of nearly 10% of the swap notional Fundamental Review of the Trading Book Following […]

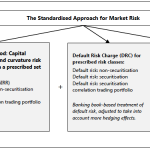

FRTB – The Default Risk Charge

Following on from my articles, Fundamental Review of the Trading Book and Internal Models or Standardised Approach, I wanted to take a look at a specific component of the Market Risk Capital, namely the Default Risk Charge as required under the Standardised Approach. Background In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum […]

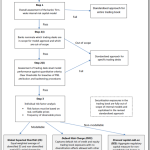

FRTB – Internal Models or Standardised Approach?

Following on from my article on Fundamental Review of the Trading Book – What You Need to Know, I wanted to look at the pros and cons of the Internal Models Approach over the Standardised Approach. Background In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum Capital Requirements for Market Risk; also known […]

Fundamental Review of the Trading Book – What You Need to Know

In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum Capital Requirements for Market Risk; also known as the Fundamental Review of the Trading Book (FRTB). These new standards replace parts of the Basel 2.5 reforms, which were introduced in 2009 to address the material undercapitalisation of trading book exposures during the […]