Current Exposure Methodology – What You Need To Know

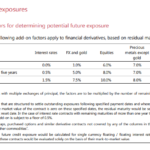

The Current Exposure Methodology is a key part of Leverage Ratio calculations. It dates back to the late 1980s and the first Basel accords on banking capital. CEM calculates the Potential Future Exposure of a derivative trade using a look-up table based on Asset Class and Maturity. CEM is a very simple, notional-based measure of […]

SA-CCR Calculator

SA-CCR for Excel calculates the Standardised Approach for Credit Risk Use it to reconcile your calculations Or assess the impact of moving to SA-CCR And perform pre-trade what-if analysis Free 14-day trials are available for all financial firms. Background In March 2014, the Basel Committee on Banking Supervision published bcbs279, the Standardised Approach for measuring Counterparty […]

SA-CCR – Explaining the Calculations

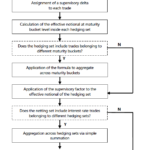

Background In March 2014, the Basel Committee on Banking Supervision published bcbs279, the Standardised Approach for measuring Counterparty Credit Risk exposures. SA-CCR replaces the current non-internal model approaches, the Current Exposure Method (CEM) of 1995 and the Standardised Method (SM) of 2005. The majority of banks currently use CEM as relatively few firms have Internal Model Method (This blog […]

Capital requirements for exposures to CCPs

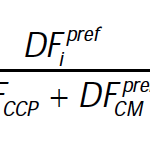

Following on from my article SA-CCR: Standardised Approach Counterparty Credit Risk, I wanted to look at the related topic of Capital requirements for Cleared Swaps and get a sense of the size of these requirements. Background In March 2014, the Basel Committee on Banking Supervision (BCBS) published it’s Standardised Approach (SA-CCR) for measuring exposure at default […]

SA-CCR: Standardised Approach Counterparty Credit Risk

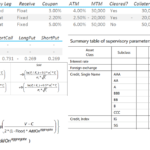

On 1 January 2017, the Standardised approach for measuring counterparty credit risk exposures (SA-CCR) will take effect. SA-CCR is required for Credit Risk Capital, as well as Exposures to CCPs and the Leverage Ratio. It is particularly important for Derivatives as it provides for improved netting benefit and recognition of margin for both cleared and bi-lateral […]